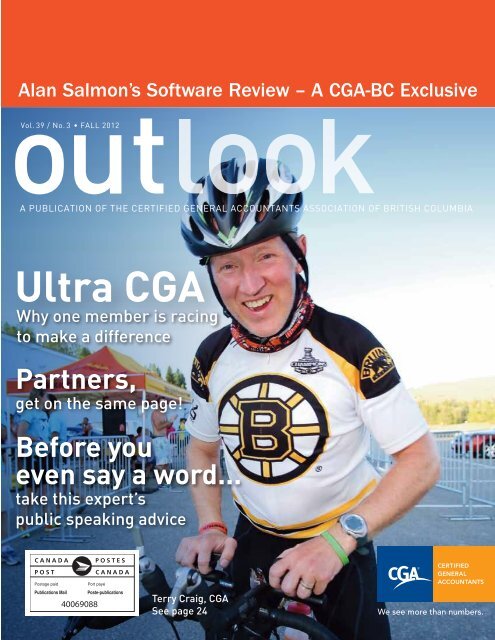

Ultra CGA

CGA Outlook Magazine Autumn 2012 - The Kemp Harvey Group

CGA Outlook Magazine Autumn 2012 - The Kemp Harvey Group

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Alan Salmon’s Software Review – A <strong>CGA</strong>-BC Exclusive<br />

Vol. 39 / No. 3 • FALL 2012<br />

A PUBLICATION OF THE CERTIFIED GENERAL ACCOUNTANTS ASSOCIATION OF BRITISH COLUMBIA<br />

<strong>Ultra</strong> <strong>CGA</strong><br />

Why one member is racing<br />

to make a difference<br />

Partners,<br />

get on the same page!<br />

Before you<br />

even say a word...<br />

take this expert’s<br />

public speaking advice<br />

40069088<br />

Terry Craig, <strong>CGA</strong><br />

See page 24

30 28 40<br />

Vol. 39 / No. 3 • FALL 2012<br />

features views spotlight<br />

24<br />

A true <strong>Ultra</strong>man<br />

<strong>CGA</strong> Terry Craig participates in a gruelling<br />

endurance event – and proves that organ<br />

donors can go the distance<br />

contents<br />

16<br />

28<br />

30<br />

Trends in accounting<br />

software<br />

Alan Salmon reviews the most popular<br />

accounting software options for you and your<br />

clients<br />

Investment options in a time<br />

of low interest rates<br />

Steve Zadra highlights income investment<br />

options that offer decent returns<br />

Life-cycle assessment<br />

LCA lets you understand the true, long-term<br />

costs of an investment decision<br />

06<br />

09<br />

12<br />

14<br />

34<br />

taxmatters<br />

Ed Kroft looks back on the<br />

major developments in<br />

Canadian tax this summer<br />

techview<br />

Your notebook is valuable –<br />

learn how to keep it (and its<br />

data) safe<br />

periscope<br />

Career coach Joanne Loberg<br />

outlines fail-safe tips for<br />

building a successful career<br />

ethics in focus<br />

Evaluating an ethical<br />

dilemma<br />

publicpractice<br />

Edifier<br />

Steve Erickson says partnerships<br />

with a high degree<br />

of trust are more profitable<br />

23<br />

36<br />

38<br />

40<br />

42<br />

keepingTabs<br />

<strong>CGA</strong>s in the news and<br />

members on the move<br />

currentAssets<br />

A roundup of all the latest<br />

gadgets, tech gear and apps<br />

snapShots<br />

Photos from <strong>CGA</strong>-BC events<br />

partingShot<br />

Meet Angela Trif, <strong>CGA</strong>, a<br />

business consultant with the<br />

Interior Health Authority and<br />

dedicated <strong>CGA</strong>-BC volunteer<br />

morethanNumbers<br />

Letting the data tell the<br />

story<br />

32<br />

Before you even say a word<br />

Planning and preparing for your public speech<br />

is just as important as the speech itself<br />

You can follow <strong>CGA</strong>-BC<br />

on Facebook and on Twitter at<br />

www.twitter.com/cgabc<br />

Cover photo (and related story photos)<br />

by Rick Kent.<br />

outlook 03

editor’smessage<br />

outlook<br />

><br />

are so afraid of public speaking<br />

that they’d rather be in the casket<br />

than giving the eulogy. Maybe<br />

that’s a bit of an exaggeration<br />

on his part, but when you finish<br />

What Did You Do This Summer?<br />

executive committee<br />

Chair: Cindy Choi, F<strong>CGA</strong><br />

Past-Chair/Treasurer: Bruce Hurst, F<strong>CGA</strong><br />

First Vice-Chair: Candace Nancke, F<strong>CGA</strong><br />

Second Vice-Chair: David Sale, F<strong>CGA</strong><br />

Chief Executive Officer and Secretary: Gordon Ruth, F<strong>CGA</strong><br />

executive staff<br />

Chief Executive Officer: Gordon Ruth, F<strong>CGA</strong><br />

Director, Administration, HR & IT: Dan Cheetham, <strong>CGA</strong><br />

Director of Marketing & Communications:<br />

Edward Downing, MA (Journalism)<br />

Director of Education & Student Services:<br />

W. D. (Bill) Johnson, FCIS, PAdm, F<strong>CGA</strong><br />

Director, Executive and Corporate Affairs: Juliana Laing, BA<br />

Director of Member Services: Pamela Skinner, BSc, CFP, <strong>CGA</strong><br />

We hear clichés like “hit the<br />

ground running” or “head of the<br />

pack” all the time. But <strong>CGA</strong> Terry<br />

Craig really lives and breathes<br />

those sayings as his performance<br />

in the <strong>Ultra</strong>man Canada<br />

competition headlined in this<br />

issue shows. He battled the heat<br />

of an Okanagan summer to run,<br />

bike and swim distances that<br />

some of us wouldn’t even drive.<br />

He did it to highlight the need<br />

for living organ donation and<br />

to show that even when you<br />

have donated a vital organ like<br />

a kidney you can be an ultracompetitive<br />

athlete.<br />

Speaking of the heat of summer,<br />

the ever perceptive and<br />

insightful Ed Kroft shows that<br />

while we were enjoying the<br />

beach or travelling this summer,<br />

a lot was happening in the<br />

world of taxation. He reports, for<br />

example, that the CRA has been<br />

conducting various income tax<br />

audits in the area of tax-free<br />

savings accounts and retirement<br />

compensation arrangements.<br />

Many of us have heard the<br />

Seinfeld line about people who<br />

reading Chris Molineux’s article<br />

(and possibly taken his course),<br />

you are going to be ready to<br />

conquer all your public speaking<br />

fears. Like everything you do as<br />

a <strong>CGA</strong>, it’s really about planning<br />

and being prepared. The rest is<br />

just technique.<br />

If you are in public practice,<br />

then Steve Erickson’s piece on<br />

getting partners on the same<br />

page has some solid tips. And<br />

ethicist Michael McDonald, <strong>CGA</strong><br />

(Hon.), tackles some of the everyday<br />

ethical issues that many<br />

of us confront.<br />

As always, we love to hear<br />

from our readers. We did get<br />

more mail than usual about last<br />

issue’s article on Gerry McKinnon,<br />

<strong>CGA</strong> (Hon.), and he even<br />

penned a letter himself. Remember,<br />

if there’s something you’d<br />

like to say or a story idea that<br />

you would like covered, don’t<br />

hesitate to contact us.<br />

outlook staff<br />

Managing Editor: Edward Downing (604) 730-6208<br />

Communications Manager: Patrick Schryburt (604) 730-6238<br />

Communications Officer: David Ferman (604) 730-6206<br />

Production Co-ordinator: Trevor Hargreaves (604) 730-6226<br />

Advertising Co-ordinator: Pardeep Clair (604) 730-6228<br />

Graphic Design:<br />

Core Associates Communication Design Inc.<br />

Regular Contributors:<br />

Ed Kroft, QC, LLB, LLM, <strong>CGA</strong> (Hon.); Dr. Michael McDonald,<br />

<strong>CGA</strong> (Hon.); Alan Salmon<br />

advertising<br />

For advertising rates, contact Pardeep Clair at<br />

(604) 730-6228 or visit our website at www.cga-bc.org.<br />

Outlook is the premier way to contact B.C.’s <strong>CGA</strong>s.<br />

Advertising in Outlook magazine does not indicate an<br />

endorsement of any business, organization, service or<br />

product by <strong>CGA</strong>-BC.<br />

Outlook is published four times a year by the Certified<br />

General Accountants Association of British Columbia and<br />

is sent to nearly 15,000 <strong>CGA</strong> members and <strong>CGA</strong> students.<br />

Opinions expressed are not necessarily endorsed by <strong>CGA</strong>-BC.<br />

Copyright <strong>CGA</strong>-BC 2012.<br />

articles, enquiries and letters<br />

Articles, enquiries and letters should be sent to Outlook:<br />

<strong>CGA</strong>-BC, 300-1867 West Broadway, Vancouver, BC, V6J 5L4<br />

(604) 732-1211 or (800) 565-1211<br />

ISSN 1488-2337 Outlook - Certified General Accountants<br />

Association of British Columbia<br />

<strong>CGA</strong> on the web<br />

Members and students, you can find all of your most<br />

important <strong>CGA</strong>-BC services online at www.cga-bc.org.<br />

Edward Downing is <strong>CGA</strong>-BC’s Director of Communications<br />

edowning@cga-bc.org<br />

Agreement no. 40069088<br />

Return undeliverable Canadian addresses to:<br />

<strong>CGA</strong>-BC, 300-1867 West Broadway, Vancouver, BC, V6J 5L4<br />

Printed in Canada<br />

04 outlook

feature<br />

“BS baffles brains. If you don’t have chutzpah it’s like a piece of wet lettuce: it just lies there. and<br />

that was the problem I had with so many accountants. I had to enrol them in public-speaking<br />

courses because they couldn’t express themselves effectively.” Gerry McKinnon, <strong>CGA</strong> (Hon.)<br />

<strong>CGA</strong>-BC’s first Executive Director instilled pride in all members and students<br />

By Quintin Winks<br />

> All his life Gerry McKinnon, <strong>CGA</strong> (Hon.), did great things: he became a decorated war<br />

veteran, raised and supported a family, was successful in business and served countless<br />

volunteer hours. Throughout, McKinnon was influential in shaping the communities<br />

and societies where he lived.<br />

Among his most recognized achievements was propelling the Certified General<br />

Accountants of British Columbia forward, helping it establish a sense of identity in<br />

the 1960s that enabled the organization to become the industry leader that it is now.<br />

It is difficult to imagine today’s <strong>CGA</strong>-BC, with all its power and polish, operating<br />

with just McKinnon, Fran Maynard and two staff members. In 1967 they worked in a<br />

dreary little office on Hastings Street. The organization had 600 <strong>CGA</strong> students, with<br />

an additional membership of about 600. <strong>CGA</strong>-BC was the governing and regulatory<br />

body responsible for their training and certification.<br />

Today the organization boasts nearly 15,000 <strong>CGA</strong>s and <strong>CGA</strong> students. Which makes<br />

it all the more remarkable that McKinnon was able to achieve what he did for the<br />

organization without being an accountant.<br />

Yet for all his achievements as Executive Director, McKinnon says he is most proud<br />

of the letters BBE, which appeared after his name at his retirement from <strong>CGA</strong>-BC on<br />

December 1, 1981. The letters stand for Best Boss Ever and were bestowed on him by<br />

affectionate staff.<br />

“He was realistic in how he perceived staff and the organization,” says Vernon Dean,<br />

who met McKinnon through <strong>CGA</strong>-BC in the 1960s and remains a close friend today.<br />

“He was fair and appreciated the staff and the work they did, and because of his own<br />

attitude a lot of them became <strong>CGA</strong>s.”<br />

Born on October 3, 1920 in Peterborough, Ontario, McKinnon embarked on his first<br />

career as a military man in Brockville as World War II drew more and more countries<br />

into the fray.<br />

34 outlook<br />

In 1942, McKinnon was sent to a<br />

new school in Nanaimo on Vancouver<br />

Island. He crossed the country<br />

by train that February, eventually<br />

arriving in the Lower Mainland.<br />

“I looked out at one point and<br />

there were snow-capped peaks<br />

and Holsteins standing up to their<br />

udders in green grass,” he says.<br />

“I thought I had died. Here it was<br />

February and we could wear short<br />

sleeves.”<br />

If that optimism is to blame for<br />

an ensuing bout of pneumonia that<br />

landed him in a Nanaimo military<br />

hospital, it must also be credited<br />

with introducing McKinnon to his<br />

future wife.<br />

While convalescing, the new<br />

brigadier intelligence officer met<br />

the “cutest little nurse” named Mary<br />

Campbell. The couple began dating<br />

and became engaged.<br />

But as love played out on<br />

Vancouver Island, war played out<br />

in Europe. Before long Mary was<br />

shipped east, so McKinnon applied<br />

to go overseas. As he lined up to<br />

board the ship sailing for England<br />

he looked up, into the sea of faces,<br />

and saw Mary.<br />

“Everything was secret and classified<br />

and we had no idea the other<br />

would be aboard,” he says. “Yet we<br />

ended up going overseas together.”<br />

The reunion lasted as long as the<br />

voyage. McKinnon was transferred<br />

to the British army, Mary to a<br />

hospital elsewhere. They had a brief<br />

reunion over beer one evening<br />

before McKinnon was shipped to<br />

Normandy as part of the D-Day<br />

invasion.<br />

“We were totally surrounded by<br />

people, some of them in big black<br />

helmets,” he says of the experience.<br />

“It was an indescribable situation.”<br />

McKinnon was wounded during<br />

the invasion and flown back to England.<br />

Back on friendly soil, he was<br />

eventually transferred into Mary’s<br />

THE PRIDE OF ONE<br />

F<br />

N<br />

O<br />

E<br />

outlook 35<br />

letters<br />

Standing a<br />

quarter-inch taller<br />

Kudos for Article<br />

Thanks for the great article on<br />

Mr. McKinnon. His is an amazing<br />

story and very worthy of sharing<br />

with the membership. Thanks!<br />

Allen Szeliga, <strong>CGA</strong><br />

Chief Financial Officer<br />

Darford International Inc.<br />

Vernon, B.C.<br />

O1<br />

1<br />

OF ONE<br />

I enjoyed reading the article on<br />

Gerry McKinnon in the recent<br />

Outlook issue. We owe a lot to<br />

the ‘pioneers’ like Gerry and<br />

his comments are ‘right on the<br />

money.’<br />

Mary McKenna, <strong>CGA</strong><br />

Capital Budget Analyst<br />

Provincial Health Services<br />

Authority<br />

Vancouver, B.C.<br />

Today I received my copy of the<br />

summer edition of Outlook and<br />

as much as I am embarrassed, I<br />

do thank you for remembering<br />

me. I certainly cherish the time<br />

Mary and I spent with the Association<br />

and its wonderful and<br />

dedicated people all across this<br />

beautiful country – many are still<br />

our closest friends.<br />

I really must acknowledge<br />

that all our goals and objectives<br />

were set by resolutions of our<br />

Board of Governors that I had the<br />

pleasure of working for and with.<br />

I did “tease” them every so often,<br />

but after all these years, many of<br />

them are still my very best friends<br />

today.<br />

If I may, I would like to correct,<br />

for the record, that it was not our<br />

B.C. office staff that revamped<br />

the course of study – that was<br />

accomplished by the then<br />

National Coordinating Council on<br />

Education and the faculty at UBC.<br />

I was the Secretary-Treasurer of<br />

that group.<br />

Many thanks to you all and<br />

again congratulations to us all<br />

on this [sic] our 60th anniversary<br />

year. Perhaps it is now time, after<br />

all our historical success, to add<br />

another quarter-inch and from<br />

now on stand a half-inch taller<br />

with justifiable pride.<br />

G. F. McKinnon, <strong>CGA</strong> (Hon.)<br />

Comox, B.C.<br />

Have an opinion? Email your “letter” to edowning@cga-bc.org<br />

Blair Mackay Mynett<br />

Valuations Inc.<br />

is the leading independent business<br />

valuation and litigation support practice<br />

in British Columbia. Our practice focus<br />

is on business valuations, mergers<br />

and acquisitions, economic loss claims,<br />

forensic accounting and other litigation<br />

accounting matters. We can be part<br />

of your team, providing you with the<br />

experience your clients require.<br />

Suite 1100<br />

1177 West Hastings Street<br />

Vancouver, BC, V6E 4T5<br />

Telephone: 604.687.4544<br />

Facsimile: 604.687.4577<br />

www.bmmvaluations.com<br />

Left to Right:<br />

Vern Blair, Cheryl Shearer, Robert D. Mackay,<br />

Kiu Ghanavizchian, Chad Rutquist,<br />

Gary M. W. Mynett, Chris Halsey-Brandt,<br />

Andy Shaw, Jeff P. Matthews, Farida Sukhia<br />

outlook 05

Ed Kroft, QC, LLB, LLM, <strong>CGA</strong> (Hon.)<br />

and Soraya Jamal, LLB, LLM<br />

taxmatters<br />

Given that I’m writing<br />

this in September,<br />

it seems fitting to<br />

talk about what has<br />

transpired during the past<br />

three months in the Canadian<br />

income tax world, particularly<br />

if you have been busy with<br />

tax return compliance or otherwise<br />

occupied. The matters<br />

that follow will be discussed<br />

at upcoming tax update<br />

seminars to be held this fall.<br />

Income tax legislation<br />

in the 2012 Federal<br />

Budget<br />

The Federal Budget was tabled<br />

on March 29, 2012, and<br />

47 resolutions were in the<br />

Notice of Ways and Means<br />

Motion tabled on that day.<br />

On April 23, 2012, the<br />

Minister of Finance tabled a<br />

Notice of Ways and Means<br />

Motion to implement some<br />

of the proposals in the 2012<br />

Budget. These include the<br />

temporary measure to allow<br />

certain family members to be<br />

RDSP plan holders (portion<br />

of resolution 1); extension of<br />

the mineral exploration tax<br />

credit for flow-through investors<br />

(resolution 2); split and<br />

late eligible dividend elections<br />

(resolution 3); taxation<br />

of the Governor General’s<br />

salary (resolution 15); partnership<br />

waivers (resolution<br />

27); gifts to foreign charitable<br />

organizations (resolution 42);<br />

political activities of charities<br />

(resolution 43); changes relating<br />

to tax shelters, including<br />

tax shelter identification<br />

numbers and increased penalties<br />

for failure of promoters<br />

to file information returns<br />

(resolutions 44 to 47); and<br />

additions to the list of eligible<br />

expenses for the medical<br />

expense tax credit (Regulation<br />

5700).<br />

On April 26, 2012, the Minister<br />

of Finance introduced<br />

Bill C-38, which implements<br />

certain tax measures from<br />

the 2012 Budget and enacts<br />

and amends several other<br />

Acts. Bill C-38 also implements<br />

all of the GST/HST<br />

A review of noteworthy income tax developments during the<br />

past three months<br />

What Happened This Summer?<br />

06 outlook<br />

Budget proposals. These<br />

address health services (including<br />

medical and assistive<br />

devices, pharmacist services<br />

and providing corrective<br />

eyewear), the book rebate<br />

for literacy organizations, tax<br />

on imported rental vehicles<br />

and streamlined accounting<br />

thresholds. On June 29, 2012,<br />

Bill C-38, the Jobs, Growth<br />

and Long-term Prosperity<br />

Act, received Royal Assent<br />

as Chapter No. 19.<br />

On August 14, 2012, the<br />

Department of Finance<br />

released draft legislation<br />

and explanatory notes<br />

pertaining to other items<br />

announced on March 29.<br />

The draft legislative proposals<br />

include the following<br />

measures:<br />

Personal Income Tax<br />

• Improving Registered<br />

Disability Savings Plans<br />

(RDSPs) following the review<br />

of the RDSP program<br />

in 2011.<br />

• Including an employer’s<br />

contributions to a group<br />

sickness or accident insurance<br />

plan in an employee’s<br />

income to the extent that<br />

CRA has been conducting<br />

various<br />

income tax audit<br />

initiatives, including<br />

audits of tax-free<br />

savings accounts,<br />

domestic trusts and<br />

retirement compensation<br />

arrangements.<br />

Ed Kroft, QC, LLB, LLM,<br />

<strong>CGA</strong> (Hon.), is a partner<br />

with Blake, Cassels &<br />

Graydon LLP. He is a<br />

member of the firm’s Tax<br />

Group and leader of its<br />

Tax Controversy & Litigation<br />

Group.<br />

Soraya Jamal, LLB, LLM,<br />

is an associate with<br />

Blake, Cassels & Graydon<br />

LLP, where she provides<br />

tax advice on domestic<br />

and international corporate<br />

taxation matters.<br />

the contributions are not<br />

in respect of wage-loss<br />

replacement benefits payable<br />

on a periodic basis.<br />

• Amending the rules<br />

applicable to retirement<br />

compensation arrangements<br />

to prevent certain<br />

schemes designed to<br />

inappropriately reduce tax<br />

liabilities.<br />

• Amending the rules applicable<br />

to Employees Profit<br />

Sharing Plans to discourage<br />

excessive contributions<br />

for employees with a<br />

close tie to their employer.<br />

Corporate Income Tax<br />

• Expanding the eligibility<br />

for the accelerated capital<br />

cost allowance for clean<br />

energy generation equipment<br />

to include a broader<br />

range of bioenergy equipment.<br />

• Phasing out the Corporate<br />

Mineral Exploration and<br />

Development Tax Credit.<br />

• Phasing out the Atlantic<br />

Investment Tax Credit for<br />

activities related to the oil<br />

& gas and mining sectors.<br />

• Providing that qualified<br />

property for the purposes<br />

of the Atlantic Investment<br />

Tax Credit will include<br />

certain electricity generation<br />

equipment and clean<br />

energy generation equipment<br />

used primarily in an<br />

eligible activity.<br />

• Reducing the general<br />

Scientific Research and Experimental<br />

Development<br />

(SR&ED) investment tax<br />

credit rate to 15 per cent<br />

from 20 per cent.<br />

• Reducing the prescribed<br />

proxy amount, which taxpayers<br />

use to claim SR&ED<br />

overhead expenditures,<br />

from 65 per cent to 55 per<br />

cent of the salaries and<br />

wages of employees who<br />

are engaged in SR&ED<br />

activities.

• Removing the profit element<br />

from arm’s-length<br />

third-party contracts for<br />

the purpose of calculating<br />

SR&ED tax credits.<br />

• Removing capital from the<br />

base of eligible expenditures<br />

for the purpose<br />

of calculating SR&ED tax<br />

incentives.<br />

• Preventing the avoidance<br />

of corporate income<br />

tax through the use of<br />

partnerships to convert<br />

income gains into capital<br />

gains.<br />

International Taxation<br />

• Ensuring that transfer<br />

pricing secondary adjustments<br />

will be treated as<br />

dividends for Part XIII withholding<br />

tax purposes.<br />

• Improving the integrity<br />

and fairness of the thin<br />

capitalization rules by:<br />

- reducing the debtto-equity<br />

ratio from 2-to-1<br />

to 1.5-to-1;<br />

- extending the scope of<br />

the thin capitalization rules<br />

to debts of partnerships of<br />

which a Canadian-resident<br />

corporation is a member;<br />

- treating disallowed<br />

interest expense under the<br />

thin capitalization rules as<br />

dividends for Part XIII withholding<br />

tax purposes; and<br />

- preventing double<br />

taxation in certain circumstances<br />

where a Canadian<br />

resident corporation<br />

borrows money from its<br />

controlled foreign affiliate.<br />

• Restricting the ability of<br />

foreign-based multinational<br />

corporations to transfer,<br />

or “dump”, foreign affiliates<br />

into their Canadian subsidiaries,<br />

while preserving the<br />

ability of these subsidiaries<br />

to undertake legitimate<br />

expansions of their Canadian<br />

businesses.<br />

• Phasing out the Overseas<br />

Employment Tax Credit.<br />

Other draft income<br />

tax legislation<br />

On July 25, 2012, the Department<br />

of Finance released<br />

draft legislation to amend the<br />

Income Tax Act. The draft legislation<br />

would add new sections<br />

12.6 and 18.3 regarding<br />

stapled securities and would<br />

amend the definitions of<br />

“non-portfolio property” and<br />

“excluded subsidiary entity” in<br />

subsection 122.1(1) and the<br />

instalment rules for SIFT trusts<br />

and SIFT partnerships. As well,<br />

the draft legislation includes<br />

an amendment to subsection<br />

214(3) to address the issue of<br />

withholding tax on amounts<br />

that are payable from a<br />

Canadian resident trust to<br />

a non-resident beneficiary<br />

but which are actually paid<br />

after the trust ceases to be a<br />

Canadian resident.<br />

On June 8, 2012, the Department<br />

of Finance released<br />

draft legislation to amend<br />

the Tax Court of Canada Act<br />

and the Income Tax Act. These<br />

proposed amendments will<br />

implement the changes<br />

required to improve the<br />

caseload management of the<br />

Tax Court of Canada.<br />

We have had a tax legislative<br />

hangover for many years.<br />

Legislation announced in<br />

2000, 2002 and 2003 has<br />

sat unpassed yet has been<br />

administered at times by<br />

the CRA as if it were law. This<br />

has caused mass confusion.<br />

Proposed legislation dealing<br />

with issues such as restrictive<br />

covenants, attribution, foreign<br />

trusts and other technical<br />

matters was released in July<br />

2010 but has not yet been<br />

passed. On August 19, 2011,<br />

draft legislation and regulations<br />

emerged regarding<br />

rules relating to foreign affiliates.<br />

Some rules are new and<br />

others are revised from an<br />

earlier release on February 27,<br />

2004. On December 14, 2011,<br />

On June 8, 2012,<br />

the Department<br />

of Finance<br />

released draft<br />

legislation to<br />

amend the Tax<br />

Court of Canada<br />

Act and the<br />

Income Tax Act.<br />

the Department of Finance<br />

released for consultation draft<br />

income tax legislation, regulations<br />

and explanatory notes<br />

regarding pooled registered<br />

pension plans.<br />

On October 31, 2011, the<br />

Department of Finance<br />

released for comments draft<br />

legislation, regulations and<br />

explanatory notes regarding<br />

technical amendments to the<br />

Income Tax Act and the Excise<br />

Tax Act. This package includes<br />

technical changes relating to<br />

trusts, investment corporations,<br />

mortgage investment<br />

corporations, mutual fund<br />

corporations and agricultural<br />

cooperative corporations; the<br />

treatment of non-residents<br />

with Canadian service providers;<br />

corporations that carry on<br />

an insurance business; and<br />

the reporting of recaptured<br />

input tax credits.<br />

On March 16, 2011, the Department<br />

of Finance released<br />

draft income tax legislation in<br />

response to decisions in three<br />

recent court cases. They are<br />

Collins v. The Queen, 2010 DTC<br />

5028 (FCA), regarding contingent<br />

amounts; Lehigh Cement<br />

Limited v. The Queen, 2010<br />

DTC 5081 (FCA), regarding<br />

withholding tax on interest<br />

paid to a non-arm’s length<br />

non-resident; and The Queen<br />

v. National Life Assurance<br />

Company of Canada, 2008 DTC<br />

6141 (FCA), regarding a life<br />

insurance corporation’s segregated<br />

fund policy reserves.<br />

Income tax case law<br />

released during the<br />

summer<br />

The appellate courts and<br />

the Tax Court of Canada do<br />

not sit frequently in July and<br />

August and decisions are not<br />

issued very often. However,<br />

the Supreme Court of<br />

Canada released Craig, which<br />

involves a Toronto lawyer<br />

who claimed farming losses<br />

outlook 07

without the application of the<br />

restricted farm loss rules. In a<br />

landmark decision, the Court<br />

unanimously rejected the<br />

application of the Moldowan<br />

decision and has enunciated<br />

a new interpretation<br />

of the rules in section 31 of<br />

the Income Tax Act. This is<br />

welcome news for taxpayers.<br />

The Alberta Court of<br />

Appeal issued two decisions<br />

(Canada Safeway and Husky)<br />

that dealt with the Alberta<br />

General Anti-Avoidance Rule<br />

(“GAAR”). The taxpayers were<br />

both successful as they had<br />

been in the lower courts.<br />

Future case law<br />

The Tax Court of Canada and<br />

the Federal Court of Appeal<br />

are expected to release a<br />

number of decisions this fall<br />

that will deal with various<br />

aspects of the GAAR. These<br />

cases deal with claims for<br />

capital losses, claims for other<br />

types of deductions and<br />

losses, transfer pricing and<br />

the imposition of non-resident<br />

withholding taxes.<br />

Taxpayers are also<br />

anticipating the Supreme<br />

Court of Canada’s decision<br />

in Daishowa, which will<br />

be heard next March. The<br />

case will address whether<br />

a vendor of a business will<br />

be required to include, as<br />

proceeds of disposition, the<br />

amount of assumed contingent<br />

liabilities associated<br />

with the assets sold.<br />

Some current CRA<br />

audit initiatives<br />

CRA has been conducting<br />

various income tax audit<br />

initiatives. One involves “high<br />

net worth individuals” and<br />

information request letters<br />

have been issued to various<br />

taxpayers. CRA continues to<br />

audit and reassess taxpayers<br />

who have made “leveraged<br />

donations” or who bought<br />

and sold real estate within a<br />

relatively short time frame.<br />

CRA has also been conducting<br />

audits of tax-free<br />

savings accounts, domestic<br />

trusts and retirement compensation<br />

arrangements. CRA<br />

is initiating audits of trusts<br />

throughout Canada, alleging<br />

that the affected trusts are<br />

resident in the jurisdiction in<br />

which the beneficiary resides<br />

notwithstanding that the<br />

trustee is resident elsewhere.<br />

The CRA is relying on the<br />

unanimous decision of the<br />

Supreme Court in Fundy<br />

Settlement, which determined<br />

that residence is based on<br />

central management and<br />

control of the trust and not<br />

the residence of the trustees.<br />

Other projects include<br />

audits of non-profit organizations,<br />

the frequent imposition<br />

of penalties for failure<br />

to file forms and slips and,<br />

generally speaking, a move<br />

to risk-based assessments.<br />

CRA is still interested in<br />

scrutinizing employee and<br />

shareholder benefits, deductibility<br />

of expenses, claims<br />

for scientific research and<br />

experimental development<br />

ITCs, and various valuationbased<br />

claims involving fair<br />

market value.<br />

Other audit issues have<br />

surfaced in connection with<br />

professional corporations,<br />

transfer pricing, indirect tax,<br />

international tax matters<br />

(such as cross-border loans<br />

and the taxation of non-resident<br />

employees working in<br />

Canada), domestic non-arm’s<br />

length transactions, interprovincial<br />

allocations and “tech<br />

wreck “ loss/gains transfers.<br />

Conclusion<br />

Some of you may have reflected<br />

long and hard about<br />

the thrilling aspects of tax<br />

during the summer. Others<br />

may have shunned any<br />

mention of tax. The contents<br />

of my review here may have<br />

reaffirmed your actions. The<br />

remainder of 2012 should<br />

prove interesting, as it seems<br />

that income tax law and<br />

practice never stays static.<br />

May the rest of 2012 bring<br />

you health, happiness and<br />

prosperity.<br />

08 outlook

Alan Salmon and Randy Johnston<br />

techview<br />

We’re all busy<br />

these days, but<br />

that’s no excuse<br />

to get sloppy<br />

when it comes to securing<br />

the safety of your notebook<br />

and other portable devices.<br />

These handy tools are valuable<br />

– making them popular<br />

targets for thieves – and they<br />

also tend to contain valuable<br />

and sensitive personal and<br />

professional information. In<br />

this article, I outline some<br />

tips for protecting these<br />

devices at home and on the<br />

road, including advice for<br />

protecting your data as you<br />

travel internationally.<br />

Keep the following in<br />

mind:<br />

• A notebook is easy to carry<br />

to and from work, presentations<br />

and client meetings<br />

– but that means it is also<br />

very easy for a thief to walk<br />

off with it.<br />

• Because a notebook is<br />

small and portable, it is<br />

easy to accidentally leave<br />

it behind – as a friend of<br />

mine did when he left<br />

his notebook in the seat<br />

pocket on an Air Canada<br />

flight to Antigua.<br />

• Your notebook is valuable<br />

to you because it<br />

can speedily give you<br />

access to important data,<br />

information and software<br />

– which also makes it<br />

valuable to others and of<br />

interest to thieves.<br />

Statistics show that there<br />

is a 1 in 14 chance that your<br />

notebook will be stolen.<br />

Even the FBI loses, on average,<br />

10 notebooks a month.<br />

Here are 10 common sense<br />

tips to protect your valuable<br />

portable devices.<br />

Carry your notebook<br />

with you<br />

Always keep your notebook<br />

with you on a plane or train<br />

rather than checking it with<br />

your luggage. It is easy to<br />

lose luggage and it is just as<br />

easy to lose your notebook.<br />

If you are travelling by car,<br />

keep your notebook out<br />

of sight by locking it in the<br />

trunk when you are not<br />

using it.<br />

A little time and effort now can save you lots of grief and<br />

headaches later<br />

Secure Your Notebook!<br />

Don’t put your notebook<br />

on the floor<br />

Setting it on the floor is an<br />

easy way to forget about it as<br />

you talk at a ticket counter or<br />

order your cappuccino. If you<br />

do set it down, put it between<br />

your feet or lean it against<br />

your leg.<br />

Keep an eye on your<br />

notebook<br />

As you go through airport<br />

security, hold your bag until<br />

the person in front of you has<br />

gone through the screening<br />

process.<br />

Avoid using computer bags<br />

Computer bags make it obvious<br />

that you are carrying a<br />

notebook. Instead, carry it in a<br />

padded briefcase or carry-on<br />

case.<br />

Use a screen guard<br />

These guards prevent someone<br />

from seeing your screen,<br />

and are particularly useful if<br />

you are working on sensitive<br />

data in a public place.<br />

Statistics show<br />

that there is a 1<br />

in 14 chance that<br />

your notebook will<br />

be stolen.<br />

Alan Salmon is a leading<br />

authority on accounting<br />

technology. He is the CEO<br />

of K2 Enterprises Canada, a<br />

North American consulting<br />

firm providing technology<br />

training to accountants. In<br />

addition to his work with<br />

consultants, accountants<br />

and software companies in<br />

both Canada and the U.S.,<br />

he is the chairperson of<br />

the Accounting Technology<br />

seminar series. He can be<br />

reached by email at<br />

alan@k2e.ca or by visiting<br />

www.k2e.ca.<br />

Randy Johnston is a shareholder<br />

in K2 Enterprises<br />

(www.k2e.com). He has<br />

been a top-rated speaker<br />

in the technology industry<br />

for over 30 years. He was<br />

inducted into the Accounting<br />

Hall of Fame in 2011.<br />

He was selected as a Top 25<br />

Thought Leader in Accounting<br />

in 2011 and 2012 and has<br />

been selected eight times by<br />

Accounting Today as one of<br />

the Top 100 Most Influential<br />

People in Accounting.<br />

Don’t leave your notebook<br />

in your hotel room<br />

Many things get lost in<br />

hotel rooms, as they are not<br />

totally secure and there are<br />

too many key cards floating<br />

around. If you do leave your<br />

notebook in your room, put<br />

the “Do not disturb” sign on<br />

the door to keep hotel staff<br />

out.<br />

Buy a notebook security<br />

device or program<br />

If you do need to leave<br />

your notebook in your<br />

hotel room, use a notebook<br />

security cable to attach it to<br />

a heavy chair, table or desk.<br />

There are also programs and<br />

devices that will report the<br />

location of a stolen laptop.<br />

These work when the<br />

notebook connects to the<br />

Internet and can report the<br />

notebook’s exact physical<br />

location via GPS tracking.<br />

Absolute Software’s LoJack<br />

and its line of Computrace<br />

products, for example, offer<br />

physical location tracing<br />

as well as capabilities for<br />

remotely disabling a missing<br />

computer, retrieving or<br />

deleting data, and more.<br />

Affix your name and<br />

contact info to your<br />

notebook<br />

You should put your name<br />

and contact information,<br />

along with the promise<br />

of a “Reward if found – no<br />

questions asked,” on your<br />

notebook. This can substantially<br />

increase your odds of<br />

getting your notebook back<br />

in the event of theft or a<br />

simple mix-up.<br />

Use strong passwords,<br />

and do not keep them in<br />

your notebook bag<br />

Strong passwords stop unauthorized<br />

access to individual<br />

files and even to the entire<br />

operating system. Of course,<br />

outlook 09

the strongest password in<br />

the world is useless if you<br />

keep it in your notebook<br />

bag.<br />

Encrypt your data<br />

If someone does get your<br />

notebook and gains access<br />

to your files, encryption<br />

(scrambling your data) gives<br />

you another layer of protection.<br />

With the Windows<br />

operating system, you can<br />

encrypt both files and folders.<br />

If someone does gain<br />

access to an important file,<br />

they cannot decrypt it and<br />

see your information. With<br />

more advanced versions<br />

of Windows, BitLocker<br />

encryption is available, or<br />

third-party products like PGP<br />

or TrueCrypt can be used to<br />

encrypt the entire drive.<br />

Cross-Border<br />

Security for Your<br />

Portable Devices<br />

If you regularly travel to the<br />

U.S. on business, you face<br />

another potential security<br />

issue with your notebook<br />

and its data. U.S. laws allow<br />

Customs and Border Protection<br />

(CBP) officers to search<br />

and confiscate notebooks,<br />

phones, cameras and other<br />

data-storing devices. Agents<br />

have also been known to<br />

download the contents of an<br />

entire computer hard drive<br />

and other storage media<br />

for later review. (Note that<br />

similar situations occur at the<br />

borders of other countries<br />

as well.) So what are your<br />

options to protect your portable<br />

devices and data from<br />

such seizures?<br />

Travel with a “bare”<br />

computer<br />

CBP officers cannot read<br />

what a device does not<br />

contain. That is why certain<br />

companies give their employees<br />

“forensically clean”<br />

computers for travel. These<br />

computers contain the<br />

operating system, required<br />

applications, and little or<br />

no data. Once they arrive at<br />

their destinations, employees<br />

work with data stored on<br />

company servers via secure<br />

virtual private networks<br />

(VPN). They can download<br />

files to their computers,<br />

upload the results to company<br />

servers and “forensically<br />

clean” their notebooks<br />

before travelling again.<br />

Since broadband Internet<br />

access is widely available<br />

across the U.S., there are few<br />

problems travelling with a<br />

clean notebook, unless you<br />

are downloading large files<br />

or are in an area with poor<br />

Internet access.<br />

Use software with “SaaS”<br />

Cloud computing is another<br />

solution to avoid having sensitive<br />

data on your portable<br />

devices. Your programs and<br />

data can be in the cloud and<br />

all you need to work is an Internet<br />

connection. However,<br />

this approach is less secure<br />

than total forensic cleanliness.<br />

Your web browser<br />

tracks your Internet activity<br />

using cookies, history and<br />

other data. Make sure you<br />

delete this record before you<br />

board your next flight.<br />

But what if the border<br />

agents really want your data?<br />

If a server (your company’s<br />

or a SaaS provider’s) resides<br />

within the borders of the<br />

United States, the U.S. Patriot<br />

Act enables U.S. government<br />

agents to access your<br />

data (and compel the SaaS<br />

company to keep the breach<br />

quiet). If the data resides<br />

outside U.S. borders, but the<br />

company’s head office or<br />

chief executives reside in the<br />

U.S., the data must be turned<br />

over upon request or the<br />

U.S. laws allow<br />

Customs and<br />

Border Protection<br />

officers to<br />

search and confiscate<br />

notebooks,<br />

phones, cameras<br />

and other datastoring<br />

devices.<br />

company/executives may<br />

face charges.<br />

Back up your data<br />

If border agents confiscate<br />

your computer, they cannot<br />

stop you from working if you<br />

have a backup of your data<br />

in a safe place, such as on<br />

another hard drive or your<br />

company’s servers. You will<br />

then be able to load that<br />

data on another portable<br />

device.<br />

Use a different user<br />

account to hold sensitive<br />

information<br />

Today’s computers can be<br />

used by different people,<br />

each with their own login.<br />

Users can password-protect<br />

their accounts so other users<br />

with access to that computer<br />

cannot access programs and<br />

documents that do not belong<br />

to them. You can set up<br />

your notebook with a “clean”<br />

non-administrative account<br />

while you are travelling and<br />

put your sensitive documents<br />

in a “safe” account for<br />

which you do not know the<br />

password. When you confirm<br />

your arrival at your final destination,<br />

the colleague who<br />

created the “safe” account<br />

can send you the password<br />

via secure email.<br />

If you follow the above steps,<br />

you will find that securing<br />

your portable devices and<br />

your data is a fair bit of work.<br />

However, what happens<br />

if you do not apply these<br />

security policies? The bottom<br />

line is that your devices and<br />

information are at much<br />

greater risk. You and your<br />

business can be liable for<br />

data loss. Never mind how<br />

long it will take you to reconfigure<br />

a new portable device.<br />

This is the technological version<br />

of the old adage: penny<br />

wise and dollar foolish.<br />

10 outlook

outlook 11

Joanne Loberg, BA, CMP, CEC<br />

periscope<br />

12 outlook<br />

Ready for your next<br />

career move? Building<br />

a successful<br />

career in financial<br />

leadership involves more<br />

than great work experience;<br />

it involves a tailored career<br />

plan, marketing tools and<br />

strategically leveraging your<br />

career to enhance your profile<br />

within and beyond your<br />

organization.<br />

Create a career plan<br />

The old adage “Keep your<br />

head down and work hard”<br />

doesn’t necessarily help you<br />

build a career as a financial<br />

leader. Instead, Recruitment<br />

Team Lead Jim Huynh of Horizon<br />

Recruitment (formerly<br />

WPCG Finance & Professional<br />

Recruitment) advises you to<br />

“develop a plan and know<br />

where you want to get in 5 to<br />

15 years.”<br />

Be a rock star<br />

Do your job well and consistently<br />

outperform your<br />

performance objectives. Not<br />

sure if your performance is on<br />

track? Don’t wait for your annual<br />

performance review, ask<br />

your manager for feedback<br />

and suggestions now to help<br />

you develop your expertise.<br />

Show initiative<br />

Increase your profile by<br />

speaking up in team and<br />

organization-wide meetings.<br />

Suggest strategies to tackle<br />

old problems and improve<br />

processes. Volunteer to take<br />

on projects − the more<br />

complex and challenging, the<br />

better.<br />

Commit to professional<br />

development<br />

Read what your leaders are<br />

reading. Notice the reading<br />

material on your senior leaders’<br />

desks. Commit yourself<br />

to keeping abreast of the<br />

broader issues impacting<br />

organizations and fine-tune<br />

your technical expertise<br />

accordingly. Consider the<br />

<strong>CGA</strong>-BC Certificate in Executive<br />

Leadership to strengthen<br />

your strategic planning, communication,<br />

project and team<br />

management, and critical<br />

decision-making skills.<br />

Tips on building a robust and rewarding career<br />

Strategies for Career Success<br />

Build a sphere of<br />

influence<br />

Success rarely happens in isolation.<br />

Jim Huynh works with<br />

successful financial leaders<br />

and advises emerging leaders<br />

to leverage their careers<br />

by focusing on “building a<br />

sphere of influence while<br />

fostering connections and<br />

growing their reputation<br />

beyond their work groups.”<br />

Get a mentor<br />

The Corporate Leadership<br />

Council surveyed CEOs of<br />

Fortune 500 organizations<br />

and discovered that one of<br />

the top reasons CEOs believed<br />

they were successful<br />

was having a mentor. Mentors<br />

guide and direct you, and<br />

provide critical strategies to<br />

navigate and advance your<br />

career.<br />

Building a<br />

successful career<br />

in financial<br />

leadership<br />

involves more<br />

than great work<br />

experience; it<br />

involves a tailored<br />

career plan,<br />

marketing tools<br />

and strategically<br />

leveraging your<br />

career.<br />

Joanne Loberg, BA, CMP,<br />

CEC, provides career<br />

coaching services to<br />

professional and executive<br />

clients needing career<br />

testing; targeted, accomplishment-based<br />

resumés<br />

and cover letters; and interview<br />

practice to ensure<br />

they launch a successful<br />

job search.<br />

Raise your profile in<br />

your organization and<br />

beyond<br />

Individuals who rise to the<br />

top typically have rich networks.<br />

Network with other<br />

business units to find out<br />

about their financial reporting<br />

needs and how your<br />

division can better serve<br />

them. Outside your organization,<br />

use the professional<br />

networking site LinkedIn<br />

to build your network. As<br />

an extra bonus, LinkedIn is<br />

actively used by recruiters<br />

to source top talent. Lastly,<br />

join a Board (www.boardmatch.org)<br />

so that you can<br />

expand your network and<br />

build your leadership skills.<br />

Communicate your<br />

success<br />

In conversations within<br />

your business unit and<br />

with key decision makers,<br />

keep others apprised of key<br />

projects you have taken on,<br />

as well as your successes.<br />

Next time you’re in the<br />

elevator and a senior leader<br />

asks how you are doing,<br />

talk about key projects or<br />

initiatives you are involved<br />

with. For example, “Things<br />

are going well. I’ve just<br />

begun implementing new<br />

financial reporting software<br />

that will greatly improve<br />

our tracking of financial<br />

performance within our<br />

branch offices.”<br />

Be a great people<br />

manager<br />

Advance your people<br />

management skills: ask your<br />

manager for the opportunity<br />

to manage larger teams.<br />

Look for opportunities to<br />

turn around team performance,<br />

coach and develop<br />

employees, conduct performance<br />

conversations<br />

and terminations (when<br />

necessary), and drive teams<br />

to successfully tackle key<br />

projects. Develop a reputation<br />

for building high-performance<br />

work teams and<br />

engaged employees.

Learn the art of<br />

influencing<br />

Patricia Hazelwood, Division<br />

Director of Robert Half Finance<br />

& Accounting, specifically<br />

looks for candidates with<br />

well-honed listening skills,<br />

since “listening is important<br />

to management as you must<br />

listen to your team” in order<br />

to influence change. She is<br />

also looking for candidates<br />

who are decisive, articulate<br />

communicators without being<br />

arrogant or pushy. In her<br />

words, it’s all about “relationship<br />

management.” Top candidates<br />

have a track record of<br />

building strong relationships<br />

throughout the organization,<br />

which enable them to influence<br />

and drive change.<br />

Fine-tune your<br />

marketing tools<br />

Critical to career success in<br />

today’s highly competitive<br />

market is a well-crafted, accomplishment-based<br />

resumé.<br />

Set yourself apart by highlighting<br />

your results, such as<br />

managing large or complex<br />

projects, implementing IT<br />

systems and suggesting<br />

strategies to improve financial<br />

reporting and increase<br />

efficiency. Where possible,<br />

quantify your results.<br />

Polish your interview<br />

skills<br />

Diane Kerley, National Practice<br />

Leader of Accounting &<br />

Finance at Aplin Professional,<br />

states it is imperative that you<br />

Critical to career<br />

success in<br />

today’s highly<br />

competitive market<br />

is a well-crafted,<br />

accomplishmentbased<br />

resumé.<br />

consistently put your best<br />

foot forward. She looks for a<br />

“great attitude, enthusiasm<br />

and good communication<br />

skills.” If nerves get the best<br />

of you, engage in interview<br />

coaching with a career coach.<br />

If you lack confidence and<br />

clarity when communicating,<br />

she recommends attending a<br />

Toastmasters group.<br />

Kerley also advises you to<br />

know your resumé inside and<br />

out, as well as your key accomplishments.<br />

Successful interview<br />

candidates are able to<br />

readily discuss their successes<br />

and sprinkle these throughout<br />

their interviews. During<br />

interviews, present examples<br />

of your accomplishments<br />

related to process improvement,<br />

project management,<br />

team leadership and other<br />

contributions to the top- and<br />

bottom-line performance of<br />

the organization.<br />

All three recruiters advise<br />

that you be prepared for<br />

these commonly asked<br />

questions (which typically are<br />

poorly answered):<br />

• “Tell me about yourself.”<br />

(Ensure your answer is<br />

relevant to the role you are<br />

applying for.)<br />

• “Why do you want to work<br />

for us?”<br />

• “What do you know about<br />

us?”<br />

• “Walk us through your resumé.”<br />

(Talk about your key<br />

accomplishments within<br />

each role.)<br />

Create a well-defined career<br />

plan, establish a track record<br />

of solid performance, take<br />

on new projects, develop<br />

your sphere of influence and<br />

ensure your key accomplishments<br />

are captured in your<br />

resumé and presented during<br />

your interviews. Lastly, Jim<br />

Huynh says “don’t be afraid of<br />

change” in order to leverage<br />

your career and reach your<br />

goals.<br />

outlook 13

By Michael McDonald, PhD, <strong>CGA</strong> (Hon.)<br />

ethics in<br />

THE DILEMMA:<br />

Mark Chagall is a recently graduated <strong>CGA</strong> who has<br />

been acting as the junior on an audit of Picasso<br />

Industries with Hank Van Gogh as lead auditor. Mark<br />

and Hank have been friends for years and are employed<br />

by Turner and Matisse, <strong>CGA</strong>s. The audit has<br />

progressed very slowly and work is now three weeks<br />

behind schedule. One of the partners, Bill Turner,<br />

has asked Mark to explain the delays.<br />

Mark is worried about what to say to Bill. The<br />

problem, as Mark sees it, is that due to excessive<br />

drinking, Hank has been very unfocused during the<br />

audit. In fact, Mark covered for Hank at two client<br />

meetings when Hank was too hungover to participate.<br />

Mark is worried that reporting this to Bill might<br />

jeopardize Hank’s position and his own friendship<br />

with Hank. What should Mark do? Further, if Mark<br />

does report this to Bill, how should Bill respond?<br />

The Situation<br />

There are two decision-makers in this dilemma – the<br />

junior <strong>CGA</strong> on the audit, Mark, and the senior <strong>CGA</strong>, Bill.<br />

Mark feels loyal to Hank both as a professional colleague<br />

and a friend. However, as a professional, Mark also knows<br />

that the audit delays will likely negatively impact both the<br />

client and the accounting firm. Mark has to decide what to<br />

tell Bill about the lack of progress in the audit and Hank’s<br />

role in those delays. As partner, Bill will have to decide<br />

what to do with Mark’s information. Even if Mark is silent<br />

about Hank’s role in the audit of Picasso, Bill still has the<br />

problem of dealing with an audit that is progressing far<br />

too slowly.<br />

A Response<br />

<strong>CGA</strong> member Cheryl Turcotte responded<br />

to this dilemma. In response<br />

to whether Mark should report the<br />

problems due to Hank’s behaviour, she<br />

wrote:<br />

I believe that Mark should let Bill know<br />

that the audit has fallen behind due to<br />

Hank’s obsession with the bottle. Not<br />

doing so ‘enables’ Hank to continue<br />

drinking and, of course, doesn’t solve<br />

any of his problems. I believe that Mark<br />

would actually be helping Hank by<br />

bringing the problem to light and making<br />

Hank face it. Furthermore, neither<br />

the client nor the firm should suffer for<br />

Hank’s addiction.<br />

I think that this recommendation<br />

heads in the right direction. It responds<br />

to the needs of the client and the firm.<br />

Hank’s drinking is not a purely personal<br />

matter, and telling Bill about the problem<br />

could also help Hank address his<br />

problems with alcoholism.<br />

But before he does this, Mark should<br />

remember R105 “Criticism of a Professional<br />

Colleague” in the <strong>CGA</strong>-BC Code<br />

of Ethical Principles and Rules of Conduct<br />

(CEPROC), since the conversation with<br />

Bill would be considered a criticism of<br />

Hank. This rule requires Mark to first<br />

discuss his issues with Hank and give<br />

him an opportunity to respond. This is<br />

only fair to Hank. The conversation may<br />

also suggest other options to Mark,<br />

such as letting Hank continue on the<br />

audit with a warning to “immediately<br />

clean up his act,” provided this does not<br />

compromise the integrity of the audit.<br />

However, Mark may decide that the<br />

only acceptable option is the request<br />

that Hank explain his personal issues<br />

and their impact on the client’s audit<br />

directly to Bill. Should Hank refuse to<br />

own up to his problem, Mark would<br />

then be obligated to inform Hank<br />

that he is bringing the matter to Bill’s<br />

attention.<br />

In regard to what Bill, the partner<br />

and senior on the audit, should do, Ms.<br />

Turcotte said:<br />

If we are to assume that Hank has<br />

been a valuable employee in the past, I<br />

believe that Bill should pull him off the<br />

audit, insist that Hank seek professional<br />

assistance such as rehab and/<br />

or Alcoholics Anonymous and (finally)<br />

that he should let Hank know the company<br />

will provide him with a leave of<br />

absence and keep his job open for his<br />

return. Bill would be best served by letting<br />

Hank know that he must choose<br />

between his job and his drinking.<br />

Perhaps this will be Hank’s bottom and<br />

14 outlook

focus<br />

he will gladly take the chance afforded to<br />

him to get back on track.<br />

This is good counsel for Bill. By removing<br />

Hank from the audit, Bill is protecting<br />

the client and the accounting firm. Further,<br />

by ordering Hank to seek professional<br />

help, Bill is potentially saving a valuable<br />

employee. Finally, Bill is dealing with<br />

Hank in an intelligent and compassionate<br />

manner. Of course Hank may not take the<br />

opportunity and he may continue in his<br />

addiction. In that case, Turner and Matisse<br />

would have no option other than dismissing<br />

Hank.<br />

What’s an Ethics Issue?<br />

In her note, Ms. Turcotte went on to comment:<br />

I do not normally react to these questions<br />

but I honestly don’t think there are any<br />

Michael McDonald is Professor<br />

Emeritus of Applied Ethics at the W.<br />

Maurice Young Centre for Applied<br />

Ethics at the University of British Columbia.<br />

In 2006, McDonald received<br />

an Honorary <strong>CGA</strong> for his extensive<br />

work in accounting ethics education.<br />

McDonald welcomes suggestions<br />

for new cases and solutions for this<br />

column.<br />

other right answers. This seems to be more<br />

a question of addiction than of ethics.<br />

Furthermore, there are human rights<br />

issues at hand where one can argue that<br />

Hank is sick and should be given every<br />

opportunity to ‘cure’ himself. In short they<br />

should do all that they can to get Hank<br />

back on track, but Hank needs to know<br />

that it cannot be to the detriment of the<br />

firm and its clients.<br />

So what is an ethics issue? A useful way<br />

of thinking about this is suggested by<br />

my colleague, Professor Susan Cox, who<br />

distinguishes between big “E” and small “e”<br />

ethics issues. For <strong>CGA</strong>s, most big “E” Ethics<br />

issues are defined in CEPROC. Then there<br />

are the multiple small “e” ethics issues we<br />

face every day, ranging from matters of<br />

courtesy and politeness to issues of safety,<br />

human rights and acting with decency<br />

toward our fellow humans.<br />

In both Ethics and ethics, there are many<br />

black and white issues with clear right and<br />

wrong answers. However, there will also<br />

be grey areas where the decision-makers<br />

have to make judgement calls. Here, good<br />

people will sometimes disagree. Consider<br />

what a difference it would make if Hank<br />

was only a so-so employee or had been<br />

previously warned about his drinking<br />

problems. Those factors might shift the<br />

issue, leading to a different decision.<br />

The Next Dilemma<br />

Lydia Ko, <strong>CGA</strong>, is employed by Maxim Accounting<br />

Services. Lydia has just returned<br />

from an on-site meeting with a new client,<br />

Tom Rex, the CEO of Dinosaur Construction<br />

Ltd.<br />

She tells her best friend and colleague<br />

Francesca Paulo that it was a very disturbing<br />

and upsetting experience and that she<br />

doesn’t want to return to the site. Lydia spoke<br />

of sexist and racist remarks from the Dinosaur<br />

Construction workers, which Tom summarily<br />

dismissed with the comment “boys will be<br />

boys.”<br />

Francesca suggests that Lydia voice her<br />

concerns to their boss, Henry Morgan, who<br />

is also a <strong>CGA</strong>. Lydia is worried about Henry’s<br />

reaction. Henry asked her to work with Dinosaur<br />

because she has an ideal skill set for their<br />

business issues. He also mentioned that this<br />

account is so substantial for Maxim that “we<br />

can’t afford to lose it.”<br />

What should Lydia do? If Lydia does voice<br />

her concerns to her boss Henry, how should<br />

Henry respond?<br />

Please email us your thoughts on this ethical<br />

dilemma. We accept anonymous submissions<br />

provided we can verify that you are a <strong>CGA</strong> or<br />

student. Send your feedback to<br />

edowning@cga-bc.org.<br />

outlook 15

$<br />

$<br />

$<br />

$<br />

$<br />

16 outlook

$<br />

Trends in Accounting<br />

Software<br />

More features and a move to the cloud<br />

Accounting software continues to shift to “cloud computing,” which<br />

will ultimately move accounting software into a new dimension.<br />

Accounting in the cloud allows everyone in the organization to<br />

have the same information at the same time, with a common set of<br />

applications easily accessible over the Internet.<br />

This will involve a major shift in how organizations deal with data. When accounting moves online, it does<br />

not stay in its own cubicle and it naturally wants to link to everything else such as payroll, CRM, your website<br />

and your other business applications. When accounting is locked in a desktop application, only a few<br />

people use it in the back office. By contrast, online accounting is multi-user, allows front staff in, and links<br />

By Alan Salmon<br />

outlook 17

Trends in Accounting<br />

Software<br />

$<br />

$<br />

to all the other business systems. Online<br />

accounting will evolve into broader business<br />

management.<br />

Accounting in the new world will be<br />

a hybrid. Many enterprises are already<br />

looking beyond their private cloud and<br />

adopting hybrid cloud computing, which<br />

maintains the benefits of traditional servers<br />

and brings in the accessibility of the<br />

public cloud (a public cloud sells services<br />

to anyone on the Internet).<br />

As accounting software vendors move<br />

their products to the cloud, publishers are<br />

also recruiting commercial hosting companies<br />

to provide hosted versions of their<br />

client/server-based applications. With the<br />

escalating popularity of tablet computers,<br />

smartphones and other mobile devices,<br />

vendors are also making it easier to manage<br />

cloud-hosted solutions using these<br />

devices.<br />

Accounting remains the interpretation<br />

of the numbers, but the manual entry and<br />

coding of transactions will be reduced<br />

significantly over the next few years. A<br />

perfect example of this is the new Wave<br />

Accounting solution for small businesses.<br />

Wave Accounting imports bank data<br />

automatically from over 10,000 financial<br />

institutions, thereby eliminating manual<br />

data entry.<br />

Online systems also facilitate Electronic<br />

Data Interchange between banks, suppliers<br />

and customers. A centrally hosted<br />

application allows vendors to continuously<br />

link to more systems and reduce<br />

manual coding. Only brand new transactions<br />

should ever have to be coded. Even<br />

the smallest business will have a near<br />

real-time view of their financials.<br />

While the movement is definitely<br />

gaining momentum, there will be serious<br />

resistance to doing accounting in<br />

the cloud. Major concerns include data<br />

security, backups, legal issues as to<br />

who owns the data and concerns about<br />

Internet shutdowns. Those adopting<br />

cloud-based solutions should have a<br />

clearly documented strategy for getting<br />

their data out of the product should they<br />

decide to make a change. One example of<br />

a provider with excellent documentation<br />

is Google’s “Data Liberation Front” (www.<br />

dataliberation.org).<br />

So, does this mean the end of traditional<br />

server-based accounting programs?<br />

No! They will certainly be around<br />

for the foreseeable future. However, from<br />

my perspective, the move to the cloud<br />

will be a popular and practical choice for<br />

many organizations.<br />

Other trends in the accounting software<br />

world in 2012 include the following:<br />

• Businesses no longer want a standalone<br />

system. CFOs realize that integration<br />

provides transparency across<br />

multiple aspects of the enterprise, and<br />

that having one system cover multiple<br />

departments is a great way to achieve<br />

that visibility. It is also simpler and<br />

usually more cost-effective to maintain<br />

one system rather than several.<br />

• There is a desire to have standardized<br />

databases and tight integration with<br />

Microsoft Office for reporting in Excel<br />

and integrating with Exchange and<br />

Outlook calendars.<br />

• Buyers want to see systems designed<br />

specifically for their “unique” needs.<br />

Stand-alone accounting systems are<br />

inherently generic, and the specialtyspecific<br />

features of a system are typically<br />

found in the automation of other<br />

$<br />

processes (shop floor control, project<br />

management, inventory control, etc.)<br />

that are removed from accounting. As a<br />

result, buyers seeking specialty-specific<br />

solutions naturally shy away from<br />

“generic” accounting applications and<br />

implement complete packages.<br />

• The emergence of Software as a Service<br />

enables collaboration and communication<br />

that was either very difficult or<br />

not achievable with older client-server<br />

systems. This collaboration enables<br />

companies to implement expansive<br />

systems to tie the enterprise together<br />

more easily.<br />

• Decision-makers are opting for systems<br />

that support consumer technologies<br />

and trends (such as remote access<br />

with mobile devices, integration with<br />

social media, and open and standardbased<br />

systems). This will naturally<br />

squeeze out horizontal accounting<br />

systems because they can offer only<br />

one function or cannot support the<br />

“must-have” consumer needs.<br />

$<br />

Software vendors are reacting to these<br />

trends by offering additional modules<br />

and customizations built for specific<br />

needs and narrow vertical markets. Their<br />

customers then implement these packages,<br />

which enhance their generic, standalone<br />

accounting software, and usually<br />

integrate to other applications. This is evident<br />

in the software accounting solutions<br />

reviewed in this article.<br />

This trend seems to vary with company<br />

size. Most very small companies (with a<br />

handful of employees and less than $1<br />

million in annual revenue) looking for<br />

a $200-$500 accounting system will opt<br />

18 outlook

$<br />

for generic packages such as QuickBooks<br />

or Simply Accounting. However, once<br />

buyers get above the $1 million to $2<br />

million annual revenue range, they tend<br />

to seek out industry-specific or integrated<br />

solutions.<br />

So, in summary, many businesses will<br />

continue to use their existing serverbased<br />

systems. However, larger businesses<br />

are increasingly moving some of their<br />

accounting to the cloud and that trend<br />

will continue to grow.<br />

A SUMMARY OF ACCOUNTING<br />

SOFTWARE TODAY<br />

Here’s a short synopsis of the direction of<br />

the major accounting software solutions;<br />

a more detailed analysis can be found<br />

online at www.cga-bc.org.<br />

..............<br />

AccountEdge<br />

For 2012, the emphasis is on usability<br />

and mobility. A redesigned Command<br />

Centre, for example, improves the user<br />

experience. The new Side Bar and additional<br />

menus make it easier to navigate<br />

the company file, while retaining the<br />

familiar AccountEdge flow chart layout.<br />

Enhancements to AccountEdge Mobile<br />

(iOS) allow mobile users to record sales<br />

and activity slips, enter expenses and<br />

contacts, and sync to the desktop version.<br />

With the new mileage tracker (in both<br />

AccountEdge and AccountEdge Mobile),<br />

users can track the date, note the vehicle<br />

used, keep trip notes, apply mileage to a<br />

specific job and add mileage to customer<br />

invoices when billing with reimbursable<br />

expenses.<br />

Additionally, AccountEdge has responded<br />

to customer requests to support<br />

Many enterprises are<br />

already adopting hybrid<br />

cloud computing,<br />

which maintains the<br />

benefits of traditional<br />

servers and brings in<br />

the accessibility of the<br />

public cloud.<br />

$<br />