US GAAP vs. IFRS The basics - Financial Executives International

US GAAP vs. IFRS The basics - Financial Executives International

US GAAP vs. IFRS The basics - Financial Executives International

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

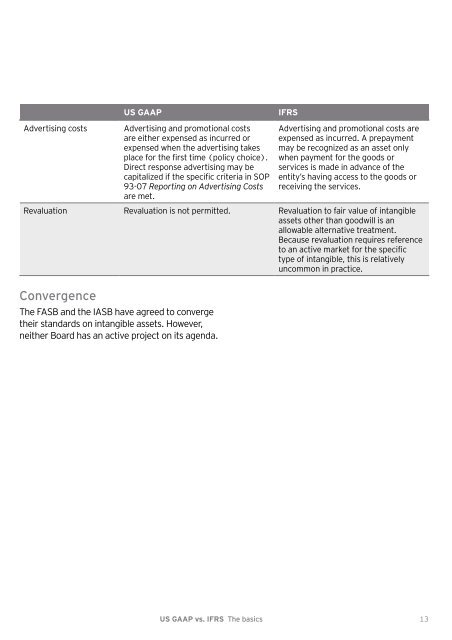

<strong>US</strong> <strong>GAAP</strong> <strong>IFRS</strong><br />

Advertising costs Advertising and promotional costs<br />

are either expensed as incurred or<br />

expensed when the advertising takes<br />

place for the first time (policy choice).<br />

Direct response advertising may be<br />

capitalized if the specific criteria in SOP<br />

93-07 Reporting on Advertising Costs<br />

are met.<br />

<strong>US</strong> <strong>GAAP</strong> <strong>vs</strong>. <strong>IFRS</strong> <strong>The</strong> <strong>basics</strong><br />

Advertising and promotional costs are<br />

expensed as incurred. A prepayment<br />

may be recognized as an asset only<br />

when payment for the goods or<br />

services is made in advance of the<br />

entity’s having access to the goods or<br />

receiving the services.<br />

Revaluation Revaluation is not permitted. Revaluation to fair value of intangible<br />

assets other than goodwill is an<br />

allowable alternative treatment.<br />

Because revaluation requires reference<br />

to an active market for the specific<br />

type of intangible, this is relatively<br />

uncommon in practice.<br />

Convergence<br />

<strong>The</strong> FASB and the IASB have agreed to converge<br />

their standards on intangible assets. However,<br />

neither Board has an active project on its agenda.<br />

13