Office Insight - Jones Lang LaSalle

Office Insight - Jones Lang LaSalle

Office Insight - Jones Lang LaSalle

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Office</strong> <strong>Insight</strong><br />

Boston . Q2 2012<br />

Tight pockets in the market, but business<br />

owners are cautious<br />

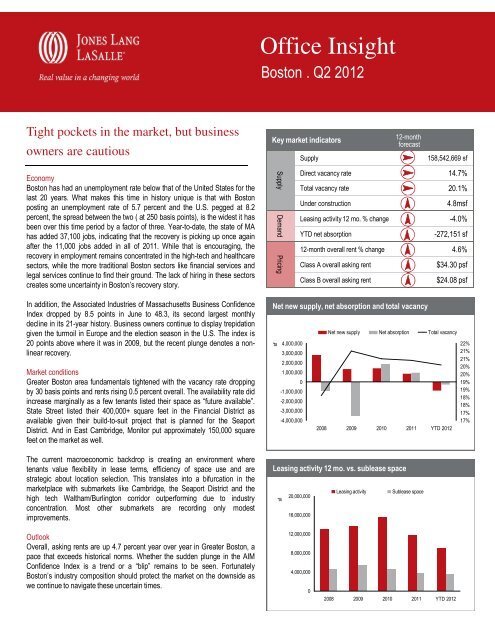

Key market indicators<br />

Supply<br />

12-month<br />

forecast<br />

158,542,669 sf<br />

Economy<br />

Boston has had an unemployment rate below that of the United States for the<br />

last 20 years. What makes this time in history unique is that with Boston<br />

posting an unemployment rate of 5.7 percent and the U.S. pegged at 8.2<br />

percent, the spread between the two ( at 250 basis points), is the widest it has<br />

been over this time period by a factor of three. Year-to-date, the state of MA<br />

has added 37,100 jobs, indicating that the recovery is picking up once again<br />

after the 11,000 jobs added in all of 2011. While that is encouraging, the<br />

recovery in employment remains concentrated in the high-tech and healthcare<br />

sectors, while the more traditional Boston sectors like financial services and<br />

legal services continue to find their ground. The lack of hiring in these sectors<br />

creates some uncertainty in Boston’s recovery story.<br />

Supply<br />

Demand<br />

Pricing<br />

Direct vacancy rate 14.7%<br />

Total vacancy rate 20.1%<br />

Under construction<br />

4.8msf<br />

Leasing activity 12 mo. % change -4.0%<br />

YTD net absorption<br />

-272,151 sf<br />

12-month overall rent % change 4.6%<br />

Class A overall asking rent<br />

$34.30 psf<br />

Class B overall asking rent<br />

$24.08 psf<br />

In addition, the Associated Industries of Massachusetts Business Confidence<br />

Index dropped by 8.5 points in June to 48.3, its second largest monthly<br />

decline in its 21-year history. Business owners continue to display trepidation<br />

given the turmoil in Europe and the election season in the U.S. The index is<br />

20 points above where it was in 2009, but the recent plunge denotes a nonlinear<br />

recovery.<br />

Market conditions<br />

Greater Boston area fundamentals tightened with the vacancy rate dropping<br />

by 30 basis points and rents rising 0.5 percent overall. The availability rate did<br />

increase marginally as a few tenants listed their space as “future available”.<br />

State Street listed their 400,000+ square feet in the Financial District as<br />

available given their build-to-suit project that is planned for the Seaport<br />

District. And in East Cambridge, Monitor put approximately 150,000 square<br />

feet on the market as well.<br />

The current macroeconomic backdrop is creating an environment where<br />

tenants value flexibility in lease terms, efficiency of space use and are<br />

strategic about location selection. This translates into a bifurcation in the<br />

marketplace with submarkets like Cambridge, the Seaport District and the<br />

high tech Waltham/Burlington corridor outperforming due to industry<br />

concentration. Most other submarkets are recording only modest<br />

improvements.<br />

Net new supply, net absorption and total vacancy<br />

sf<br />

Leasing Historical activity asking 12 mo. vs. vs. effective sublease rents space<br />

sf<br />

4,000,000<br />

3,000,000<br />

2,000,000<br />

1,000,000<br />

0<br />

-1,000,000<br />

-2,000,000<br />

-3,000,000<br />

-4,000,000<br />

20,000,000<br />

16,000,000<br />

Net new supply Net absorption Total vacancy<br />

2008 2009 2010 2011 YTD 2012<br />

Leasing activity<br />

Sublease space<br />

22%<br />

21%<br />

21%<br />

20%<br />

20%<br />

19%<br />

19%<br />

18%<br />

18%<br />

17%<br />

17%<br />

Outlook<br />

Overall, asking rents are up 4.7 percent year over year in Greater Boston, a<br />

pace that exceeds historical norms. Whether the sudden plunge in the AIM<br />

Confidence Index is a trend or a “blip” remains to be seen. Fortunately<br />

Boston’s industry composition should protect the market on the downside as<br />

we continue to navigate these uncertain times.<br />

12,000,000<br />

8,000,000<br />

4,000,000<br />

0<br />

2008 2009 2010 2011 YTD 2012

<strong>Jones</strong> <strong>Lang</strong> <strong>LaSalle</strong> Americas Research • Boston <strong>Office</strong> <strong>Insight</strong> • Q2 2012 2<br />

Tenant perspective<br />

Rent growth continues to be relegated to key, hot submarkets like<br />

Cambridge and the Seaport District. Areas north of the city like Burlington<br />

that are in the high tech corridor are exhibiting rising rents and high levels<br />

of net absorption as well. The South continues to lag as it contends with<br />

large blocks of space once used as back office Financial Services space.<br />

Tenants are truly selecting space and submarkets that meet their<br />

objectives from a branding and talent attraction standpoint if they can<br />

afford the space. As vacancy drops in key submarkets, demand is spilling<br />

into neighboring areas but some tenants like State Street Bank, Liberty<br />

Mutual, Ironwood, Vertex and Biogen are all choosing to build their own<br />

space in tight submarkets versus occupying existing buildings in looser<br />

areas. We are also starting to see spec office space in the construction<br />

pipeline (fully financed by developer) but a testament to the belief that<br />

tenants will pay a premium for new space.<br />

Landlord perspective<br />

Asking rents rose only 0.5 percent in the second quarter but landlords in<br />

the various submarkets are exposed to very different set of dynamics.<br />

Landlords continue to play offensively in the healthiest submarkets like<br />

Cambridge and the Seaport District. In the suburbs, 128/Mass Pike and<br />

the high tech corridor in the north continues to exhibit landlord favorable<br />

conditions. The first speculative office space is being built in Burlington<br />

speaking to the bullish sentiment that tenants will chose location and<br />

newer space over older space in secondary or tertiary submarkets.<br />

Landlords in these outer suburbs are struggling to attract tenants and look<br />

to create an urban feel in a suburban environment wherever and<br />

whenever they can. Troubled assets are also an issue in the outer<br />

suburbs with almost 10 percent of the space in 495/Mass Pike for<br />

example (equaling over 1.3 million square feet) in some form of trouble.<br />

Class A overall asking rents<br />

Class A tenant improvement allowance<br />

$ psf<br />

$70<br />

CBD<br />

Suburbs<br />

$ psf<br />

$70<br />

CBD<br />

Suburbs<br />

$60<br />

$60<br />

$50<br />

$50<br />

$40<br />

$40<br />

$30<br />

$30<br />

$20<br />

$20<br />

$10<br />

$10<br />

$0<br />

2008 2009 2010 2011 Q2 2012<br />

$0<br />

2008 2009 2010 2011 Q2 2012<br />

Class A free rent<br />

Class A blocks of contiguous space<br />

months<br />

9<br />

8<br />

7<br />

6<br />

5<br />

4<br />

3<br />

2<br />

1<br />

0<br />

CBD<br />

Suburbs<br />

2008 2009 2010 2011 Q2 2012<br />

# of blocks<br />

90<br />

80<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

60<br />

20<br />

50,000 -<br />

100,000 sf<br />

CBD<br />

25<br />

10<br />

100,000 -<br />

200,000 sf<br />

Includes vacant existing blocks and available blocks<br />

Suburbs<br />

5<br />

4<br />

> 200,000<br />

sf

<strong>Jones</strong> <strong>Lang</strong> <strong>LaSalle</strong> Americas Research • Boston <strong>Office</strong> <strong>Insight</strong> • Q2 2012 3<br />

Property clock – current market conditions<br />

Submarket leverage – market history and forecast<br />

Submarket 2010 2011 2012 2013 2014<br />

Landlord leverage<br />

Tenant leverage<br />

Back Bay<br />

Financial District<br />

Seaport District<br />

Cambridge<br />

128 Mass Pike<br />

495 Mass Pike<br />

495 North<br />

North<br />

Northwest<br />

South<br />

Landlord-favorable<br />

conditions<br />

Balanced<br />

conditions<br />

Tenant-favorable<br />

conditions<br />

Completed lease transactions<br />

Tenant Address Submarket Sf Type<br />

RSA, security division of EMC 174 Middlesex Turnpike, Bedford Northwest 328,232 Renewal<br />

Blue Cross Blue Shield 101 Huntington Avenue Back Bay 330,000 Relocation<br />

Red Hat, Inc. 314 Littleton Road, Westford 495/North 175,000 Renewal w/ Build-to-Suit<br />

Aveo Pharmaceutical (Lab) 650 East Kendall Street East Cambridge 126,065 Relocation<br />

Children’s Hospital Boston Landmark Center Back Bay 111,000 Sublease<br />

LogMeIn 320 Summer Street Seaport District 101,821 Relocation<br />

EnerNOC One Marina Park Drive Seaport District 100,000 Relocation<br />

Conformis 28 Crosby Drive, Bedford Northwest 90,000 Relocation<br />

Sybase, Inc. 15 Wayside Road, Burlington Northwest 62,805 Relocation w/ Contraction<br />

Top completed sale transactions<br />

Address Submarket Buyer / Seller Sf Sale Price $ psf<br />

451 D Street Seaport District Shorenstein Partners/Rockpoint 496,000 $115,000,000 $232<br />

13 Building portfolio Healthcare Trust of<br />

America/Stewart Healthcare<br />

Bedford Business Park Northwest The Davis Companies/Boston<br />

Properties<br />

371,000 $100,000,000 $400<br />

470,000 $62,800,000 $133<br />

Greater Boston methodology: Inventory includes all Class A, B, & C office properties, excluding all condo, medical and owner occupied buildings

About <strong>Jones</strong> <strong>Lang</strong> <strong>LaSalle</strong><br />

<strong>Jones</strong> <strong>Lang</strong> <strong>LaSalle</strong> (NYSE:JLL) is a financial and professional services firm specializing in real estate. The firm offers integrated services delivered<br />

by expert teams worldwide to clients seeking increased value by owning, occupying or investing in real estate. With 2011 global revenue of $3.6<br />

billion, <strong>Jones</strong> <strong>Lang</strong> <strong>LaSalle</strong> serves clients in 70 countries from more than 1,000 locations worldwide, including 200 corporate offices. The firm is an<br />

industry leader in property and corporate facility management services, with a portfolio of approximately 2.1 billion square feet worldwide. <strong>LaSalle</strong><br />

Investment Management, the company’s investment management business, is one of the world’s largest and most diverse in real estate with $47.7<br />

billion of assets under management. For further information, please visit our website, www.joneslanglasalle.com.<br />

About <strong>Jones</strong> <strong>Lang</strong> <strong>LaSalle</strong> Research<br />

<strong>Jones</strong> <strong>Lang</strong> <strong>LaSalle</strong>’s research team delivers intelligence, analysis, and insight through market-leading reports and services that illuminate today’s<br />

commercial real estate dynamics and identify tomorrow’s challenges and opportunities. Our 300 professional researchers track and analyze<br />

economic and property trends and forecast future conditions in over 60 countries, producing unrivalled local and global perspectives. Our research<br />

and expertise, fueled by real-time information and innovative thinking around the world, creates a competitive advantage for our clients and drives<br />

successful strategies and optimal real estate decisions.<br />

Boston <strong>Office</strong><br />

One Post <strong>Office</strong> Square<br />

Suite 2600<br />

Boston, MA 02109<br />

+1 617 523 8000<br />

www.us.joneslanglasalle.com/boston<br />

©2012 <strong>Jones</strong> <strong>Lang</strong> <strong>LaSalle</strong> IP, Inc. All rights reserved. No part of this publication may be reproduced by any means, whether graphically, electronically, mechanically or otherwise<br />

howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission<br />

of <strong>Jones</strong> <strong>Lang</strong> <strong>LaSalle</strong>. The information contained in this document has been compiled from sources believed to be reliable. <strong>Jones</strong> <strong>Lang</strong> <strong>LaSalle</strong> or any of their affiliates accept no<br />

liability or responsibility for the accuracy or completeness of the information contained herein and no reliance should be placed on the information contained in this document.