CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

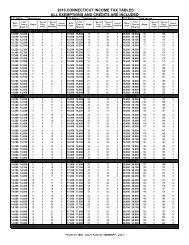

Table B - <strong>Tax</strong> Calculation for <strong>2011</strong> <strong>Tax</strong>able Year<br />

Use the fi ling status shown on the front of your return. This is the initial tax calculation of your tax liability. It does not<br />

include personal tax credits, the 3% phase-out or tax recapture.<br />

Single or Filing Separately<br />

If the amount on line 3 of the <strong>Tax</strong> Calculation Schedule is:<br />

Less than or equal to: ..................................................... $ 10,000 ...............3.00%<br />

More than $10,000, but less than or equal to ................. $ 50,000 ...............$300 plus 5.0% of the excess over $10,000<br />

More than $50,000, but less than or equal to ................. $100,000 ..............$2,300 plus 5.5% of the excess over $50,000<br />

More than $100,000, but less than or equal to ............... $200,000 ..............$5,050 plus 6.0% of the excess over $100,000<br />

More than $200,000, but less than or equal to ............... $250,000 ..............$11,050 plus 6.5% of the excess over $200,000<br />

More than $250,000 .....................................................................................$14,300 plus 6.7% of the excess over $250,000<br />

Line 3 is $13,000, Line 4 is $450<br />

$13,000 - $10,000 = $3,000<br />

$3,000 X .05 = $150<br />

$300 + $150 = $450<br />

Single or Filing Separately Examples:<br />

Line 3 is $525,000, Line 4 is $32,725<br />

$525,000 - $250,000 = $275,000<br />

$275,000 x .067 = $18,425<br />

$14,300 + $18,425 = $32,725<br />

Filing Jointly/Qualifying Widow(er)<br />

If the amount on line 3 of the <strong>Tax</strong> Calculation Schedule is:<br />

Less than or equal to: ..................................................... $ 20,000 ...............3.00%<br />

More than $20,000, but less than or equal to ................. $100,000 ..............$600 plus 5.0% of the excess over $20,000<br />

More than $100,000, but less than or equal to ............... $200,000 ..............$4,600 plus 5.5% of the excess over $100,000<br />

More than $200,000, but less than or equal to ............... $400,000 ..............$10,100 plus 6.0% of the excess over $200,000<br />

More than $400,000, but less than or equal to ............... $500,000 ..............$22,100 plus 6.5% of the excess over $400,000<br />

More than $500,000 .....................................................................................$28,600 plus 6.7% of the excess over $500,000<br />

Filing Jointly/Qualifying Widow(er) Examples:<br />

Line 3 is $22,500, Line 4 is $725<br />

Line 3 is $1,100,000, Line 4 is $68,800<br />

$22,500 - $20,000 = $2,500<br />

$1,100,000 - $500,000 = $600,000<br />

$2,500 x .05 = $125<br />

$600,000 x .067 = $40,200<br />

$600 + $125 = $725<br />

$28,600 + $40,200 = $68,800<br />

Head of Household<br />

If the amount on line 3 of the <strong>Tax</strong> Calculation Schedule is:<br />

Less than or equal to: ..................................................... $ 16,000 ...............3.00%<br />

More than $16,000, but less than or equal to ................. $ 80,000 ...............$480 plus 5.0% of the excess over $16,000<br />

More than $80,000, but less than or equal to ................. $160,000 ..............$3,680 plus 5.5% of the excess over $80,000<br />

More than $160,000, but less than or equal to ............... $320,000 ..............$8,080 plus 6.0% of the excess over $160,000<br />

More than $320,000, but less than or equal to ............... $400,000 ..............$17,680 plus 6.5% of the excess over $320,000<br />

More than $400,000 .....................................................................................$22,880 plus 6.7% of the excess over $400,000<br />

Line 3 is $20,000, Line 4 is $680<br />

$20,000 - $16,000 = $4,000<br />

$4,000 x .05 = $200<br />

$480 + $200 = $680<br />

Head of Household Examples:<br />

Line 3 is $825,000, Line 4 is $51,355<br />

$825,000 - $400,000 = $425,000<br />

$425,000 x .067 = $28,475<br />

$22,880 + $28,475 = $51,355<br />

Form <strong>CT</strong>-<strong>1040</strong>TCS Back (Rev. 12/11)<br />

Page 47