COMMERCIAL REAL ESTATE MARKET - Knight Frank

COMMERCIAL REAL ESTATE MARKET - Knight Frank

COMMERCIAL REAL ESTATE MARKET - Knight Frank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

2009<br />

Commercial<br />

real estate market<br />

Moscow<br />

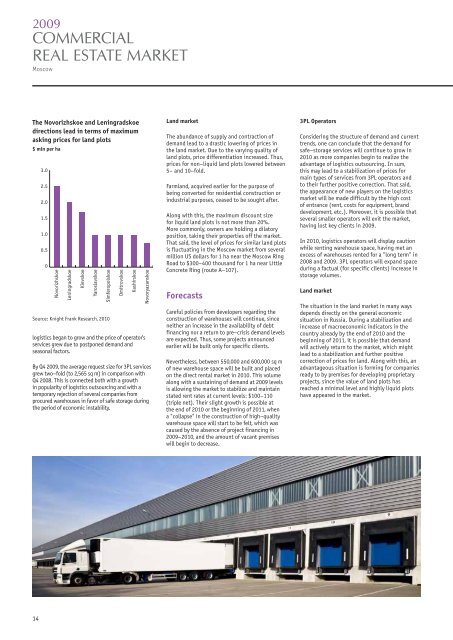

The Novorizhskoe and Leningradskoe<br />

directions lead in terms of maximum<br />

asking prices for land plots<br />

$ mln per ha<br />

3.0<br />

2.5<br />

2.0<br />

1.5<br />

1.0<br />

0.5<br />

0<br />

Novorizhskoe<br />

Leningradskoe<br />

Kievskoe<br />

Yaroslavskoe<br />

Simferopolskoe<br />

Source: <strong>Knight</strong> <strong>Frank</strong> Research, 2010<br />

Dmitrovskoe<br />

Kashirskoe<br />

logistics began to grow and the price of operator's<br />

services grew due to postponed demand and<br />

seasonal factors.<br />

Novoryazanskoe<br />

By Q4 2009, the average request size for 3PL services<br />

grew two–fold (to 2,565 sq m) in comparison with<br />

Q4 2008. This is connected both with a growth<br />

in popularity of logistics outsourcing and with a<br />

temporary rejection of several companies from<br />

procured warehouses in favor of safe storage during<br />

the period of economic instability.<br />

Land market<br />

The abundance of supply and contraction of<br />

demand lead to a drastic lowering of prices in<br />

the land market. Due to the varying quality of<br />

land plots, price differentiation increased. Thus,<br />

prices for non–liquid land plots lowered between<br />

5– and 10–fold.<br />

Farmland, acquired earlier for the purpose of<br />

being converted for residential construction or<br />

industrial purposes, ceased to be sought after.<br />

Along with this, the maximum discount size<br />

for liquid land plots is not more than 20%.<br />

More commonly, owners are holding a dilatory<br />

position, taking their properties off the market.<br />

That said, the level of prices for similar land plots<br />

is fluctuating in the Moscow market from several<br />

million US dollars for 1 ha near the Moscow Ring<br />

Road to $300–400 thousand for 1 ha near Little<br />

Concrete Ring (route A–107).<br />

Forecasts<br />

Careful policies from developers regarding the<br />

construction of warehouses will continue, since<br />

neither an increase in the availability of debt<br />

financing nor a return to pre–crisis demand levels<br />

are expected. Thus, some projects announced<br />

earlier will be built only for specific clients.<br />

Nevertheless, between 550,000 and 600,000 sq m<br />

of new warehouse space will be built and placed<br />

on the direct rental market in 2010. This volume<br />

along with a sustaining of demand at 2009 levels<br />

is allowing the market to stabilize and maintain<br />

stated rent rates at current levels: $100–110<br />

(triple net). Their slight growth is possible at<br />

the end of 2010 or the beginning of 2011, when<br />

a "collapse" in the construction of high–quality<br />

warehouse space will start to be felt, which was<br />

caused by the absence of project financing in<br />

2009–2010, and the amount of vacant premises<br />

will begin to decrease.<br />

3PL Operators<br />

Considering the structure of demand and current<br />

trends, one can conclude that the demand for<br />

safe–storage services will continue to grow in<br />

2010 as more companies begin to realize the<br />

advantage of logistics outsourcing. In sum,<br />

this may lead to a stabilization of prices for<br />

main types of services from 3PL operators and<br />

to their further positive correction. That said,<br />

the appearance of new players on the logistics<br />

market will be made difficult by the high cost<br />

of entrance (rent, costs for equipment, brand<br />

development, etc.). Moreover, it is possible that<br />

several smaller operators will exit the market,<br />

having lost key clients in 2009.<br />

In 2010, logistics operators will display caution<br />

while renting warehouse space, having met an<br />

excess of warehouses rented for a "long term" in<br />

2008 and 2009. 3PL operators will expand space<br />

during a factual (for specific clients) increase in<br />

storage volumes.<br />

Land market<br />

The situation in the land market in many ways<br />

depends directly on the general economic<br />

situation in Russia. During a stabilization and<br />

increase of macroeconomic indicators in the<br />

country already by the end of 2010 and the<br />

beginning of 2011, it is possible that demand<br />

will actively return to the market, which might<br />

lead to a stabilization and further positive<br />

correction of prices for land. Along with this, an<br />

advantageous situation is forming for companies<br />

ready to by premises for developing proprietary<br />

projects, since the value of land plots has<br />

reached a minimal level and highly liquid plots<br />

have appeared in the market.<br />

14

![[PDF] ÐÑогÑамма меÑоÐÑиÑÑÐ¸Ñ - Knight Frank](https://img.yumpu.com/43099779/1/184x260/pdf-n-3-4-n-1-4-1-4-1-4-un-3-4-nnnn-knight-frank.jpg?quality=85)

![[PDF] Ð Ñнок коммеÑÑеÑкой недвижимоÑÑи - Knight Frank](https://img.yumpu.com/36235407/1/184x260/pdf-n-1-2-3-4-3-4-1-4-1-4-unnun-3-4-1-2-u-1-4-3-4-nn-knight-frank.jpg?quality=85)

![[PDF] ÐлиÑÐ½Ð°Ñ Ð¶Ð¸Ð»Ð°Ñ Ð½ÐµÐ´Ð²Ð¸Ð¶Ð¸Ð¼Ð¾ÑÑÑ - Knight Frank](https://img.yumpu.com/35569291/1/184x260/pdf-n-1-2-n-n-1-2-u-1-4-3-4-nnn-knight-frank.jpg?quality=85)

![[pdf] ÑÑнок оÑиÑной недвижимоÑÑи - Knight Frank](https://img.yumpu.com/34340947/1/184x260/pdf-nn-1-2-3-4-3-4-nn-1-2-3-4-1-2-u-1-4-3-4-nn-knight-frank.jpg?quality=85)

![[PDF] СкладÑкой ÑÐµÐ³Ð¼ÐµÐ½Ñ - Knight Frank](https://img.yumpu.com/31048046/1/184x260/pdf-n-3-4-nu-1-4-u-1-2-n-knight-frank.jpg?quality=85)