An Introduction to Error Correction Models An Introduction to ECMs ...

An Introduction to Error Correction Models An Introduction to ECMs ...

An Introduction to Error Correction Models An Introduction to ECMs ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

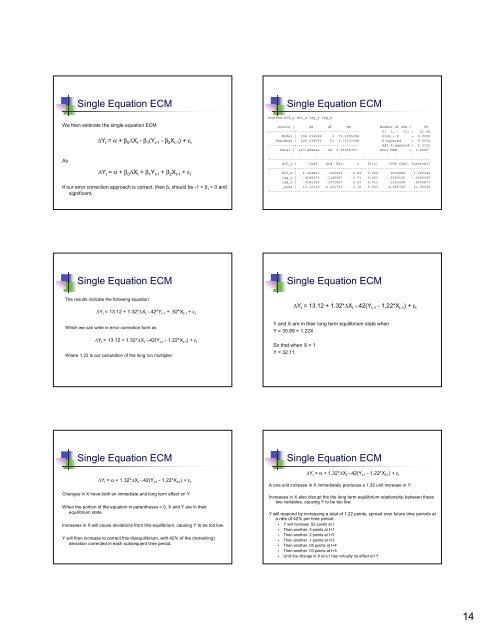

Single Equation ECM<br />

We then estimate the single equation ECM<br />

As<br />

∆Y t = α + β 0∆X t - β 1(Y t-1 - β 2X t-1) + ε t<br />

∆Y t = α + β 0∆X t + β 1Y t-1 + β 2X t-1 + ε t<br />

If our error correction approach is correct, then β 1 should be -1 < β 1 < 0 and<br />

significant.<br />

Single Equation ECM<br />

The results indicate the following equation<br />

∆Y t = 13.12 + 1.32*∆X t -.42*Y t-1 + .52*X t-1 + ε t<br />

Which we can write in error correction form as<br />

∆Y t = 13.12 + 1.32*∆X t -.42(Y t-1 - 1.22*X t-1 ) + ε t<br />

Where 1.22 is our calculation of the long run multiplier<br />

Single Equation ECM<br />

∆Y t = α + 1.32*∆X t -.42(Y t-1 - 1.22*X t-1 ) + ε t<br />

Changes in X have both an immediate and long term effect on Y<br />

When the portion of the equation in parentheses = 0, X and Y are in their<br />

equilibrium state.<br />

Increases in X will cause deviations from this equilibrium, causing Y <strong>to</strong> be <strong>to</strong>o low.<br />

Y will then increase <strong>to</strong> correct this disequilibrium, with 42% of the (remaining)<br />

deviation corrected in each subsequent time period.<br />

Single Equation ECM<br />

regress dif_y dif_x lag_y lag_x<br />

Source | SS df MS Number of obs = 55<br />

-------------+------------------------------ F( 3, 51) = 21.40<br />

Model | 238.216589 3 79.4055296 Prob > F = 0.0000<br />

Residual | 189.278033 51 3.71133398 R-squared = 0.5572<br />

-------------+------------------------------ Adj R-squared = 0.5312<br />

Total | 427.494622 54 7.91656707 Root MSE = 1.9265<br />

-----------------------------------------------------------------------------dif_y<br />

| Coef. Std. Err. t P>|t| [95% Conf. Interval]<br />

-------------+---------------------------------------------------------------dif_x<br />

| 1.324821 .200003 6.62 0.000 .9232986 1.726344<br />

lag_y | -.4248235 .1146587 -3.71 0.001 -.6550105 -.1946365<br />

lag_x | .5182186 .1971867 2.63 0.011 .1223498 .9140873<br />

_cons | 13.12112 4.201755 3.12 0.003 4.685745 21.55649<br />

------------------------------------------------------------------------------<br />

Single Equation ECM<br />

∆Y t = 13.12 + 1.32*∆X t -.42(Y t-1 - 1.22*X t-1) + ε t<br />

Y and X are in their long term equilibrium state when<br />

Y = 30.89 + 1.22X<br />

So that when X = 1<br />

Y = 32.11<br />

Single Equation ECM<br />

∆Y t = α + 1.32*∆X t -.42(Y t-1 - 1.22*X t-1 ) + ε t<br />

A one unit increase in X immediately produces a 1.32 unit increase in Y.<br />

Increases in X also disrupt the the long term equilibrium relationship between these<br />

two variables, causing Y <strong>to</strong> be <strong>to</strong>o low.<br />

Y will respond by increasing a <strong>to</strong>tal of 1.22 points, spread over future time periods at<br />

a rate of 42% per time period.<br />

� Y will increase .52 points at t<br />

� Then another .3 points at t+1<br />

� Then another .2 points at t+2<br />

� Then another .1 points at t+3<br />

� Then another .05 points at t+4<br />

� Then another .03 points at t+5<br />

� Until the change in X at t-1 has virtually no effect on Y<br />

14