You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Highlights of <strong>the</strong> First Quarter<br />

Economic Environment<br />

AIRBAKE ALL-CLAD ARNO CALOR CLOCK KRUPS LAGOSTINA MIRRO MOULINEX PANEX<br />

PENEDO REGAL ROCHEDO ROWENTA SAMURAI <strong>SEB</strong> SUPOR TEFAL T-FAL WEAREVER<br />

Business Review<br />

for <strong>the</strong> three months ended 31 March 2008<br />

QUARTELY FINANCIAL INFORMATION<br />

24 April 2008<br />

During <strong>the</strong> first quarter of 2008, <strong>the</strong> general economic environment remained highly<br />

favourable in January and February, in line with 2007 trends, but began to tighten in a few<br />

countries in March. Compared with <strong>the</strong> vigorous 9.2% increase in first-quarter 2007, organic<br />

growth in consolidated revenue was very satisfactory, at 8.5%. This performance was led by<br />

sustained strong consumer spending in almost every market, which drove increased sales<br />

volumes and a high-quality revenue stream. It also reflected <strong>the</strong> continued strong appeal of<br />

brands, <strong>the</strong> popularity of product innovations and successful partnership programmes, which<br />

have now become a prominent feature of <strong>the</strong> small household equipment landscape.<br />

Never<strong>the</strong>less, <strong>the</strong> two major challenges that have shaped <strong>the</strong> business environment for <strong>the</strong><br />

past two years remained in effect during <strong>the</strong> quarter:<br />

� On <strong>the</strong> currency front, several of <strong>the</strong> Group’s leading functional currencies continued<br />

to depreciate against <strong>the</strong> euro, sometimes at even a faster pace than in 2007. Based<br />

on average rates for first-quarter 2008 and 2007, <strong>the</strong> US dollar lost 12% year-on-year<br />

against <strong>the</strong> euro, <strong>the</strong> rouble 5%, <strong>the</strong> Korean won 15%, <strong>the</strong> Mexican peso 11% and <strong>the</strong><br />

British pound 11%. On <strong>the</strong> o<strong>the</strong>r hand, <strong>the</strong> Turkish lira and <strong>the</strong> yen remained more or<br />

less stable and <strong>the</strong> Brazilian real gained ano<strong>the</strong>r 4% during <strong>the</strong> period. In all, <strong>the</strong>se<br />

fluctuations reduced reported revenue by €18 million during <strong>the</strong> quarter, compared<br />

with €19 million a year earlier. In addition to <strong>the</strong> negative impact when sales in several<br />

of our major international markets are translated into euros, <strong>the</strong> currency situation is<br />

also presenting a challenge for our competitiveness. For while <strong>the</strong> strong euro is<br />

lowering <strong>the</strong> cost of purchasing raw materials and components, it is also having an<br />

adverse effect on our export business, most of which is still based in Western Europe.<br />

The currency environment <strong>the</strong>refore remains an area of concern in early 2008, as it<br />

was in 2007.<br />

� Prices of raw materials, especially metals, remain high, although <strong>the</strong> sustained upward<br />

trend of recent years seems to be levelling off. Aluminium prices, for example, were<br />

close to <strong>the</strong>ir historic highs, at an average $2,730 a tonne, but were relatively stable<br />

compared with <strong>the</strong> average $2,800 a tonne paid in first-quarter 2007. Similarly, after<br />

soaring to record highs in 2007, <strong>the</strong> price of nickel (used to make stainless steel)<br />

stood at an average $28,860 a tonne in <strong>the</strong> first quarter, versus an average $41,450 a<br />

GROUPE <strong>SEB</strong> �<br />

DIRECTION DE LA COMMUNICATION FINANCIERE<br />

Chemin du Petit Bois I BP 172 - 69134 ECULLY Cedex France I T.+33 (0)4 72 18 16 40 • Fax +33 (0)4 72 18 15 99<br />

Société par Actions Simplifiée au capital de 806 400 € I 016 950 842 R.C.S Lyon I T.V.A FR 94016950842

year earlier. The sharp drop reflects a certain build-up in global nickel inventories as<br />

<strong>the</strong> wider use of alternative steels with lower nickel content pushes down demand.<br />

Prices never<strong>the</strong>less remain very high. On <strong>the</strong> o<strong>the</strong>r hand, prices of copper (used in<br />

cookware and motors) are continuing to trend steeply upwards, to an average $7,760<br />

a tonne in first-quarter 2008 versus $5,940 a year earlier. The rise, which is ongoing,<br />

is being driven by low global inventories, strong demand and speculative trading. At<br />

<strong>the</strong> same time, plastics and packaging prices are beginning to feel <strong>the</strong> impact of<br />

higher oil prices. Because purchases of metals inputs are hedged 12 months in<br />

advance, price fluctuations do not immediately feed through to purchasing costs; <strong>the</strong>ir<br />

impact is spread over time. The impact is more immediate in <strong>the</strong> case of sourced<br />

products, since suppliers quickly and directly pass on any increase in <strong>the</strong>ir raw<br />

materials costs.<br />

Consolidation of Supor<br />

The successful completion of a partial public tender offer on 21 December 2007 enabled<br />

<strong>Groupe</strong> <strong>SEB</strong> to raise its interest in Chinese company Supor to a controlling 52.74% from <strong>the</strong><br />

30% it had held since 31 August. Previously 30% accounted for by <strong>the</strong> equity method over<br />

four months in 2007, Supor has been fully consolidated since 1 January 2008. The process<br />

of integrating <strong>the</strong> company into our global operations is now well underway, led by two<br />

operating committees:<br />

� The Strategy Committee, comprising members of <strong>the</strong> <strong>Groupe</strong> <strong>SEB</strong> Executive<br />

Committee and <strong>the</strong> leading members of Supor’s senior management team, is defining<br />

and leading Supor’s strategic vision, while also identifying <strong>the</strong> priority objectives of <strong>the</strong><br />

integration process.<br />

� The Integration Committee, comprising members of Supor’s senior management<br />

team, is implementing <strong>the</strong> Strategy Committee’s decisions and carrying out <strong>the</strong><br />

integration process.<br />

As part of this process, ten strategic projects have been defined. Of <strong>the</strong>se, six have been<br />

given priority and are being implemented in <strong>the</strong> short term:<br />

� Develop Supor’s export sales.<br />

� Drive its expansion in South East Asia.<br />

� Mutually transfer products and technologies between Supor and <strong>Groupe</strong> <strong>SEB</strong> in two<br />

areas, cookware and small electrical appliances (covered by two different projects).<br />

� Adjust Supor’s outsourcing strategy.<br />

� Implement <strong>the</strong> chosen production strategy.<br />

At <strong>the</strong> same time, <strong>the</strong> process includes six integration projects, of which five have been<br />

given priority:<br />

� Improve plant productivity.<br />

� Optimise purchasing.<br />

� Integrate and align Finance, Human Resources and Information Systems processes<br />

(covered by three separate projects).<br />

Process alignment is already underway, while <strong>the</strong> exchange of best practices between <strong>the</strong><br />

Group and Supor teams has got off to a promising start.<br />

Three-for-one stock split<br />

On 12 February, <strong>the</strong> Board of Directors decided to ask shareholders at <strong>the</strong> Annual Meeting<br />

on 13 May to approve a 3-for-1 stock split, which would reduce <strong>the</strong> share’s par value to €1.00<br />

from €3.00. If approved at <strong>the</strong> Meeting, <strong>the</strong> split will be carried out next 16 June, at which<br />

time <strong>the</strong> <strong>SEB</strong> share price will be divided by three.<br />

GROUPE <strong>SEB</strong> �<br />

DIRECTION DE LA COMMUNICATION FINANCIERE<br />

Chemin du Petit Bois I BP 172 - 69134 ECULLY Cedex France I T.+33 (0)4 72 18 16 40 • Fax +33 (0)4 72 18 15 99<br />

Société par Actions Simplifiée au capital de 806 400 € I 016 950 842 R.C.S Lyon I T.V.A FR 94016950842

For more than a year, <strong>the</strong> <strong>SEB</strong> share has been trading at more than €100, making it one of<br />

<strong>the</strong> most expensive stocks in <strong>the</strong> SBF 120 index. The 3-for-1 split would enable <strong>the</strong> share to<br />

trade in a price band that would be more attractive and affordable for retail investors, while<br />

improving <strong>the</strong> liquidity of its market. The new shares will carry <strong>the</strong> same voting rights and<br />

rights to <strong>the</strong> supplementary dividend as <strong>the</strong> old shares. The split will not have any impact for<br />

shareholders, who will not have to do anything or pay any fees, nor will <strong>the</strong> value of <strong>the</strong>ir<br />

holdings change.<br />

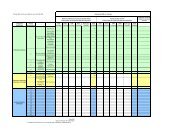

Business Review<br />

(in € millions) Q1 2007 Q1 2008<br />

% change<br />

Reported At constant<br />

exchange<br />

rates<br />

France 124 141 + 13.0 + 13.0<br />

O<strong>the</strong>r EU countries 151 159 + 5.4 + 7.2<br />

North America 89 89 + 0.6 + 12.1<br />

South America 60 61 + 1.3 - 0.5<br />

Central Europe, CIS<br />

and o<strong>the</strong>r countries<br />

138 153 + 11.6 + 13.5<br />

Asia-Pacific 51 122 +137.0 +144.4<br />

TOTAL 613 725 + 18.2 + 21.2<br />

Rounded figures Percentages based on exact figures, before rounding<br />

Revenue for <strong>the</strong> first three months of 2008 totalled €725 million, up 18.2% on a reported<br />

basis and 21.2% at constant exchange rates. The very strong growth reflected a combination<br />

of several factors:<br />

� The €78 million three-month contribution from Supor, acquired in late 2007 and fully<br />

consolidated since 1 January 2008.<br />

� A negative €18 million currency effect, compared with a negative €19 million in firstquarter<br />

2007. Although <strong>the</strong> Brazilian real fur<strong>the</strong>r appreciated against <strong>the</strong> euro during<br />

<strong>the</strong> period, <strong>the</strong> gain failed to offset <strong>the</strong> declines in several of <strong>the</strong> Group’s functional<br />

currencies, including <strong>the</strong> US dollar (which continued to weaken), <strong>the</strong> rouble, <strong>the</strong><br />

Korean won and <strong>the</strong> British pound.<br />

� Organic growth, excluding Supor, of 8.5%, reflecting sustained solid business levels<br />

despite <strong>the</strong> high prior-year comparatives (9.2% in first-quarter 2007 and 8.6% over <strong>the</strong><br />

full year).<br />

On a pro forma basis (including Supor in first-quarter 2007), growth would have stood at<br />

7.7% as reported and 10.4% at constant exchange rates.<br />

The robust like-for-like revenue growth was led by higher sales volumes and a fur<strong>the</strong>r<br />

improvement in <strong>the</strong> product mix, with <strong>the</strong> price effect having only a slightly positive impact. At<br />

constant scope of consolidation, unit sales, while stable in cookware, rose sharply in small<br />

electrical appliances, lifted by <strong>the</strong> sustained strong sales of <strong>the</strong> new products launched in<br />

GROUPE <strong>SEB</strong> �<br />

DIRECTION DE LA COMMUNICATION FINANCIERE<br />

Chemin du Petit Bois I BP 172 - 69134 ECULLY Cedex France I T.+33 (0)4 72 18 16 40 • Fax +33 (0)4 72 18 15 99<br />

Société par Actions Simplifiée au capital de 806 400 € I 016 950 842 R.C.S Lyon I T.V.A FR 94016950842

2007 (such as <strong>the</strong> Silence Force vacuum cleaner, Dolce Gusto and <strong>the</strong> Actifry fryer) and <strong>the</strong>ir<br />

introduction in new geographic markets. This offset <strong>the</strong> wea<strong>the</strong>r-related underperformance of<br />

fan sales in South America. At <strong>the</strong> same time, <strong>the</strong> product mix continued to move upmarket<br />

as demand shifted to higher value-added items, such as steam generators ra<strong>the</strong>r than steam<br />

irons, expresso machines ra<strong>the</strong>r than filter coffeemakers and <strong>the</strong> Actify oil-free fryer ra<strong>the</strong>r<br />

than conventional deep-fryers.<br />

In addition, almost all of <strong>the</strong> business lines reported higher sales for <strong>the</strong> period, with only food<br />

preparation appliances showing a slight decline. While <strong>the</strong> home comfort business contracted<br />

sharper over <strong>the</strong> period, dragged down by poor fan sales. All of <strong>the</strong> o<strong>the</strong>r businesses<br />

reported growth varying from satisfactory to very strong. Geographically, sales trended<br />

upwards in <strong>the</strong> majority of countries in <strong>the</strong> first quarter, except in South America, where <strong>the</strong><br />

year got off to a slow start, and <strong>the</strong> Middle East, where <strong>the</strong>re were problems with distribution.<br />

In particular, European markets continued to expand, with demand remaining firm except for<br />

some isolated weakness in March.<br />

The detailed breakdown of revenue by region has been updated somewhat since <strong>the</strong><br />

beginning of <strong>the</strong> year to highlight <strong>the</strong> Asia-Pacific region, where China is now making a larger<br />

contribution to consolidated business. Revenue by region may <strong>the</strong>refore be analysed as<br />

follows.<br />

In France, <strong>the</strong> small electrical appliance market remained buoyant during <strong>the</strong> first quarter,<br />

with substantial growth in volumes, a very slight consolidation in prices and an improvement<br />

in <strong>the</strong> product mix as demand continued to move upmarket. This was favourable for<br />

established brands, which fur<strong>the</strong>r streng<strong>the</strong>ned <strong>the</strong>ir positions, as well as for <strong>Groupe</strong> <strong>SEB</strong>,<br />

which saw revenue gain 13% over <strong>the</strong> period. Although some of <strong>the</strong> growth came from<br />

purchases postponed from December 2007, <strong>the</strong> Group also continued to gain market share<br />

by leveraging its flagship products, such as 1) <strong>the</strong> Actifry oil-free fryer, which remains as<br />

popular as ever; 2) <strong>the</strong> Silence Force vacuum cleaner, which is going from strength to<br />

strength thanks to its exceptionally quiet operation; 3) <strong>the</strong> breadmakers, with a very strong<br />

performance by <strong>the</strong> Baguette model; and 4) Dolce Gusto, which is making fur<strong>the</strong>r headway.<br />

At <strong>the</strong> same time, <strong>the</strong> quarter saw a sharp upturn in demand for more traditional products,<br />

revitalised by innovative features and designs, as well as by marketing campaigns. Steam<br />

cookers, irons and steam generators, for example, enjoyed a marked, and sometimes strong,<br />

increase in sales. On <strong>the</strong> o<strong>the</strong>r hand, business was more mixed in cookware, with growth in<br />

non-stick products offset by a decline in pressure cookers and bakeware. It was also more<br />

challenging in informal meal appliances and personal care products, where <strong>the</strong> offering<br />

needs to be revamped in response to intense competition.<br />

In <strong>the</strong> rest of <strong>the</strong> 15-country European Union, revenue was up 7.2% at constant exchange<br />

rates for <strong>the</strong> quarter, or by an organic 4.8% excluding Supor. Growth reflected a slightly more<br />

contrasted situation than in 2007, both by country and by month, with business slowing<br />

noticeably and sometimes declining in several markets in March. While firm overall,<br />

performance varied by country. Momentum remained strong in Spain, where a number of lost<br />

retail slots were regained and business was brisk in new products and partnerships (mainly<br />

Nespresso and Dolce Gusto). Fast growth continued apace across all our local product<br />

ranges in Greece and Switzerland, while growth remained satisfactory in Austria. In Italy, a<br />

weaker economy and <strong>the</strong> non-recurrence of a first-quarter 2007 promotional campaign led to<br />

a slight decline in revenue at constant scope of consolidation. After holding firm early in <strong>the</strong><br />

year, sales in Germany were hard hit when market conditions suddenly worsened in March,<br />

with a steep drop in demand and more aggressive competition that dampened growth.<br />

Revenue in Belgium, <strong>the</strong> Ne<strong>the</strong>rlands and Portugal was almost unchanged, as <strong>the</strong> tougher<br />

market environment was offset by successful sales of such flagship products as Actifry,<br />

Dolce Gusto and Silence Force, as well as <strong>the</strong> breadmakers, which made remarkable<br />

GROUPE <strong>SEB</strong> �<br />

DIRECTION DE LA COMMUNICATION FINANCIERE<br />

Chemin du Petit Bois I BP 172 - 69134 ECULLY Cedex France I T.+33 (0)4 72 18 16 40 • Fax +33 (0)4 72 18 15 99<br />

Société par Actions Simplifiée au capital de 806 400 € I 016 950 842 R.C.S Lyon I T.V.A FR 94016950842

progress. After a very difficult 2007, business in <strong>the</strong> United Kingdom rebounded significantly<br />

(at constant exchange rates) in <strong>the</strong> first quarter. The upturn cannot be extrapolated over <strong>the</strong><br />

full-year, however, because it was due more to <strong>the</strong> impact of special cookware promotions<br />

and <strong>the</strong> success of a few specific products (like Actify, Dolce Gusto and Quick Cup) than to<br />

an improvement in <strong>the</strong> market, which remains highly competitive and price driven.<br />

Sales in North America were up 12.1% at constant exchange rates, versus just 0.6% as<br />

reported. The currency effect primarily reflected <strong>the</strong> weaker dollar, with <strong>the</strong> decline in <strong>the</strong><br />

peso against <strong>the</strong> euro having a much less material impact. Organic growth stood at 7.3% for<br />

<strong>the</strong> period. As in 2007, <strong>the</strong> situation varied by country and brand. In <strong>the</strong> United States, where<br />

operations were reorganised and segmented in January, consumer spending is lacklustre<br />

and property market woes are weighing on purchases of kitchen equipment. Never<strong>the</strong>less,<br />

sales enjoyed satisfactory growth at constant scope of consolidation and exchange rates,<br />

supported by three core mid-range products: 1) T-fal cookware, whose sales recovered<br />

sharply on <strong>the</strong> positive retailer response to <strong>the</strong> brand’s repositioning upmarket; 2) Rowenta<br />

steam generators, which gave <strong>the</strong> brand a new growth momentum; and 3) Emeril’s small<br />

electrical appliance range designed by T-fal steam cookers, fryers and o<strong>the</strong>r items which had<br />

a good start to <strong>the</strong> year. Mirro WearEver sales contracted during <strong>the</strong> period. While WearEver<br />

is gradually replacing T-Fal in <strong>the</strong> lower mid-range, Mirro has yet to rebuild its entry-level<br />

positioning in an especially aggressive marketplace. In <strong>the</strong> premium segment, Krups’<br />

revenue continued to contract over <strong>the</strong> period, but <strong>the</strong> US market introduction of <strong>the</strong><br />

BeerTender in March drove an upsurge in sales at quarter-end, which augurs well for <strong>the</strong><br />

months ahead. All-Clad got off to a slow start to <strong>the</strong> year compared with a fairly strong firstquarter<br />

2007, despite a satisfactory March after <strong>the</strong> successful launch of new product lines.<br />

Performance was also mixed in <strong>the</strong> rest of <strong>the</strong> region. Sales were down in Canada in a<br />

challenging environment, even though <strong>the</strong> excellent results of our premium brands<br />

(especially All-Clad and Krups) demonstrate that <strong>the</strong> market is open to <strong>the</strong> emergence of<br />

upscale niches. Rowenta also saw an increase in local sales. In Mexico, market dynamics<br />

are shifting towards a strong preference for coffeemakers, but we continued to enjoy strong<br />

revenue growth, amplified in <strong>the</strong> first quarter by a special promotional campaign as part of a<br />

loyalty programme.<br />

In South America, revenue ended <strong>the</strong> first-quarter down 0.5% at constant exchange rates,<br />

breaking with several years of solid, uninterrupted expansion. In fact, <strong>the</strong> nearly flat growth<br />

was almost entirely attributable to operations in Brazil, where revenue declined 2.5% at<br />

constant exchange rates (but was up 1.2% as reported) after unfavourable wea<strong>the</strong>r during<br />

<strong>the</strong> quarter severely weighed on demand for fans. Excluding fan sales, Arno maintained<br />

market share in all of its flagship products, such as coffeemakers, blenders, sandwich<br />

makers and semi-automatic washing machines. Panex reported satisfactory growth despite<br />

<strong>the</strong> more intense competitive environment, which is being reshaped by 1) <strong>the</strong> stronger real,<br />

which makes it easier to import low-cost Asian products; 2) <strong>the</strong> growing influence of modern<br />

mass retailers and <strong>the</strong> increased consolidation of traditional channels; 3) <strong>the</strong> arrival of new<br />

market entrants; and 4) more aggressive marketing by competitors. At <strong>the</strong> same time, <strong>the</strong><br />

Group is continuing to expand in Venezuela, where consumer spending remains firm but<br />

where <strong>the</strong> political and economic situation is becoming more tense, particularly with<br />

Colombia. In <strong>the</strong> latter country, a sharp slowdown in demand, combined with <strong>the</strong> impact of<br />

wea<strong>the</strong>r on fan sales, caused local revenue to decline during <strong>the</strong> quarter. In Argentina and<br />

Chile, on <strong>the</strong> o<strong>the</strong>r hand, <strong>the</strong> broadening of our product offering in a more promising<br />

environment helped to drive an increase in revenue for <strong>the</strong> period.<br />

Central Europe, CIS and o<strong>the</strong>r countries (Turkey and o<strong>the</strong>r countries in <strong>the</strong> Middle East<br />

and Africa) account for 21% of consolidated sales. In recent years, business has been<br />

GROUPE <strong>SEB</strong> �<br />

DIRECTION DE LA COMMUNICATION FINANCIERE<br />

Chemin du Petit Bois I BP 172 - 69134 ECULLY Cedex France I T.+33 (0)4 72 18 16 40 • Fax +33 (0)4 72 18 15 99<br />

Société par Actions Simplifiée au capital de 806 400 € I 016 950 842 R.C.S Lyon I T.V.A FR 94016950842

expanding very quickly in <strong>the</strong>se regions, with revenue rising 20.5% at constant exchange<br />

rates in 2007. This trend continued in first-quarter 2008, as follows:<br />

� Consumer spending on household equipment remained as brisk as ever in Poland,<br />

Slovakia, Czech Republic, Bulgaria and o<strong>the</strong>r Central European countries, where we<br />

are streng<strong>the</strong>ning our positions by fur<strong>the</strong>r broadening <strong>the</strong> product range and<br />

successfully introducing our flagship products. Dolce Gusto, for example, has been<br />

launched in <strong>the</strong> Czech Republic and Slovakia, where its fast sales growth is very<br />

encouraging for <strong>the</strong> product’s scheduled September launch in Poland. The sustained<br />

development of large Western retail chains is providing an additional source of growth<br />

in <strong>the</strong>se booming markets.<br />

� Although <strong>the</strong> weaker rouble has made imports more expensive, <strong>the</strong> Group enjoyed<br />

robust growth in <strong>the</strong> CIS during <strong>the</strong> quarter, led by very strong demand across <strong>the</strong><br />

product line-up and <strong>the</strong> successful development of Actify, <strong>the</strong> breadmakers and<br />

microwave ovens. In this very promising environment, we never<strong>the</strong>less limited our<br />

sales to certain Russian customers whose tax situation was uncertain. At <strong>the</strong> same<br />

time, we recorded unprecedented growth in Ukraine, where demand has reached<br />

record highs.<br />

� The first-quarter also saw a very strong performance in Turkey, in a fairly stable<br />

currency environment and a market shaped by rising demand, aggressive competition<br />

and a fast changing retail industry. Led by <strong>the</strong> success of <strong>the</strong> country’s 156 Tefal<br />

shops, <strong>the</strong> growth concerned a large proportion of <strong>the</strong> product offering and confirmed<br />

<strong>the</strong> recovery initiated in second-half 2007.<br />

� In <strong>the</strong> Middle East, on <strong>the</strong> o<strong>the</strong>r hand, revenue was down sharply for <strong>the</strong> quarter<br />

despite growing demand, due to temporary difficulties at our primary distributor in<br />

Saudi Arabia and <strong>the</strong> impact of <strong>the</strong> Iran embargo.<br />

The Asia-Pacific region (China, South East Asia, Japan, South Korea, Australia, etc.)<br />

accounted for nearly 17% of consolidated revenue in first-quarter 2008, versus just 7% in<br />

2007. Revenue in <strong>the</strong> region has now been broken out separately to highlight <strong>the</strong> growing<br />

importance of our business in China following <strong>the</strong> acquisition of Supor. Based on <strong>the</strong> new<br />

breakdown, revenue in <strong>the</strong> Asia-Pacific region had risen by around 7% in 2007. In firstquarter<br />

2008, revenue surged more than 144% at constant exchange rates due to <strong>the</strong> firsttime<br />

consolidation of Supor. Growth at constant scope of consolidation and exchange rates<br />

was 10.7%, shaped by <strong>the</strong> following:<br />

� Faster momentum in South Korea, as <strong>the</strong> effective revitalisation of <strong>the</strong> cookware<br />

range offset <strong>the</strong> impact of a weaker won.<br />

� Fur<strong>the</strong>r advances in Australia and New Zealand, where we outperformed <strong>the</strong> markets<br />

and streng<strong>the</strong>ned our positions in cookware, steam generators and steam cookers.<br />

� Firm sales in Japan, especially of pressure cookers, whose use was encouraged by a<br />

major government energy savings campaign in <strong>the</strong> first quarter. The currency<br />

environment remained unfavourable, however.<br />

� Strong growth in Malaysia, where <strong>the</strong> Group is well positioned to respond to fast rising<br />

demand.<br />

In China, Supor, whose revenue was not consolidated in first-quarter 2007, reported a more<br />

than 30% increase in consolidated revenue in first-quarter 2008, in line with <strong>the</strong> company’s<br />

2007 performance. Growth was led by <strong>the</strong> development of <strong>the</strong> booming small appliance<br />

business.<br />

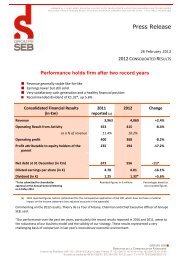

Financial Indicators<br />

Operating margin<br />

GROUPE <strong>SEB</strong> �<br />

DIRECTION DE LA COMMUNICATION FINANCIERE<br />

Chemin du Petit Bois I BP 172 - 69134 ECULLY Cedex France I T.+33 (0)4 72 18 16 40 • Fax +33 (0)4 72 18 15 99<br />

Société par Actions Simplifiée au capital de 806 400 € I 016 950 842 R.C.S Lyon I T.V.A FR 94016950842

Traditionally, sales are relatively slow in <strong>the</strong> first quarter, which accounts for an average 21-<br />

22% of <strong>the</strong> annual total. Because certain expenses (notably corporate overheads) are<br />

incurred year-round, this seasonal factor has a direct impact on quarterly operating margin.<br />

As a result, <strong>the</strong> first three months are not representative of annual revenue and performance.<br />

Operating margin amounted to €73.5 million in first-quarter 2008, a 73% increase from <strong>the</strong><br />

€42.6 million reported a year earlier. It included a €7.3 million contribution from Supor for <strong>the</strong><br />

period.<br />

High raw materials prices continued to push up purchasing costs, adding €1 million to direct<br />

raw materials procurement despite <strong>the</strong> attenuating impact of our hedging strategy. The<br />

improvement in operating margin primarily came from <strong>the</strong> organic growth in sales and<br />

particularly from <strong>the</strong> effective management of <strong>the</strong> product mix. The price effect was still<br />

positive, but to a much lesser extent than in previous quarters due to increased competition<br />

in certain European countries. O<strong>the</strong>r factors were <strong>the</strong> positive €7 million currency effect,<br />

which was almost entirely due to <strong>the</strong> weaker dollar, and our disciplined cost management.<br />

Variable costs are under control and fixed costs have stabilised, helping to drive a clear<br />

improvement in margins during <strong>the</strong> quarter. This performance has given <strong>the</strong> Group <strong>the</strong><br />

resources it needs to continue supporting its future growth, in particular by fur<strong>the</strong>r increasing<br />

its advertising expenditure in <strong>the</strong> second quarter, ahead of Mo<strong>the</strong>r’s Day.<br />

Financial position<br />

Debt stood at €489 million at 31 March 2008, a €138 million increase from a year earlier. The<br />

increase was due to <strong>the</strong> debt taken on to finance <strong>the</strong> Supor acquisition, all of which was<br />

incurred in second-half 2007. It was attenuated, however, by <strong>the</strong> continued paydown of debt,<br />

by €97 million in <strong>the</strong> first quarter, in line with <strong>the</strong> positive trend recorded at year-end 2007.<br />

The paydown reflected <strong>the</strong> sustained improvement in working capital management,<br />

especially in <strong>the</strong> area of inventories.<br />

Based on equity of €960 million at 31 March, gearing stood at 51% for <strong>the</strong> period. This was<br />

representative of <strong>the</strong> fact that debt for <strong>the</strong> year is generally lowest at <strong>the</strong> end of March. The<br />

Group’s financial situation <strong>the</strong>refore remains very healthy.<br />

Events since 31 March 2007<br />

On 28 April 2008, <strong>the</strong> new Supor plant was inaugurated in Vietnam.<br />

Outlook<br />

In an environment that showed some signs of worsening at quarter’s end, <strong>Groupe</strong> <strong>SEB</strong><br />

remains confident in its ability to capitalise on its strategic advantages to drive organic growth<br />

in 2008 and to fur<strong>the</strong>r improve margins. In this way, and by continuing to invest in research<br />

and development, as well as in marketing and advertising to promote our innovations, we will<br />

securely build our future, now and in <strong>the</strong> years to come.<br />

GROUPE <strong>SEB</strong> �<br />

DIRECTION DE LA COMMUNICATION FINANCIERE<br />

Chemin du Petit Bois I BP 172 - 69134 ECULLY Cedex France I T.+33 (0)4 72 18 16 40 • Fax +33 (0)4 72 18 15 99<br />

Société par Actions Simplifiée au capital de 806 400 € I 016 950 842 R.C.S Lyon I T.V.A FR 94016950842