Climate Action 2010-2011

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Energy and Mitigation<br />

The electricity market challenge for<br />

low-carbon technologies<br />

In OECD countries, nuclear plants provide large amounts<br />

of carbon-free electricity at low and predictable costs for up<br />

to 60 years under stringent regulatory oversight that ensures<br />

high standards of safety and security. Decision-makers in<br />

a majority of our member countries agree with us that the<br />

challenges of safety, waste disposal and proliferation can be<br />

suitably addressed. What then is holding back a ‘nuclear<br />

renaissance’ to slash GHG emissions?<br />

A major issue is certainly economics. While nuclear<br />

plants have attractive average costs calculated over<br />

their complete lifetime, they are expensive to build and<br />

therefore have high upfront investment costs. According<br />

to the new IEA/NEA study Projected Costs of Generating<br />

Electricity: <strong>2010</strong> Edition, the capital costs of an individual<br />

1,000 Megawatt (MW) usually varies between US$3<br />

and US$6 billion at a five per cent real discount rate and<br />

between US$4 and UD$7 billion at a 10 per cent real<br />

discount rate. Of course, the precise costs vary significantly,<br />

even between OECD countries, due to different reactor<br />

designs and different regulatory frameworks as well as due<br />

to differences in labour costs and exchange rates.<br />

The combination of high fixed costs during<br />

construction and low variable costs during operations is<br />

a characteristic that nuclear energy shares with all other<br />

low-carbon or carbon-free energies, be they renewable<br />

energies for generating electricity, carbon capture and<br />

storage or even investments in demand-side management<br />

and energy efficiency. Fossil-fuel based power plants,<br />

which emit significant amounts of CO 2<br />

, instead have<br />

comparatively low fixed costs and comparatively high<br />

variable costs. This conjunction is not the fruit of chance.<br />

High carbon intensity and high variable costs (and<br />

comparatively low fixed costs) always come together as<br />

they are both due to the same underlying reason: the use<br />

of expensive, carbon-intensive and frequently imported<br />

fossil fuels such as gas and oil.<br />

In the marketplace for electricity, low-carbon<br />

technologies with high fixed costs and low variable costs<br />

thus compete with fossil-fuel based technologies with<br />

low fixed costs and high variable costs. Concerns about<br />

climate change have heightened the overall attractiveness<br />

of low-carbon technologies, nuclear among them, from<br />

a social point of view. This is increasingly seen in public<br />

opinion polls.<br />

However, the economic incentives for private<br />

investors have actually shifted to the other direction.<br />

The deregulation of electricity markets and the<br />

liberalisation of electricity prices have enormously<br />

increased the volatility of prices and the uncertainty<br />

of investors. Confronted with such unprecedented<br />

risks, investors will try to limit their exposure in the<br />

case that prices fall and thus opt for technologies with<br />

comparatively lower fixed costs. This, however, means<br />

more greenhouse gas-emitting, fossil-fuel technologies.<br />

The impact of carbon pricing<br />

Uncertainty in electricity markets tilts the balance against<br />

low-carbon technologies such as nuclear and renewables.<br />

While renewables have to some extent been shielded from<br />

this effect through direct subsidies or through subsidised<br />

feed-in tariffs, the magnitude of the challenge in terms of<br />

GHG emission reductions over the next decades is far too<br />

large to be solved by selective subsidisation.<br />

What has supported the drive towards low-carbon<br />

technologies in the electricity market is the widely-shared<br />

concern about climate change-inducing GHG emissions.<br />

Implicitly or explicitly, such concerns translated into an<br />

increase of the current or perceived future costs of GHG<br />

emissions or, in its simplest form, a price to pay for each<br />

tonne of CO 2<br />

. The most concrete expression of this trend is<br />

so far is the European Emission Trading System (EU ETS),<br />

where the price for a tonne of carbon is currently<br />

hovering around €15 (slightly less than US$20).<br />

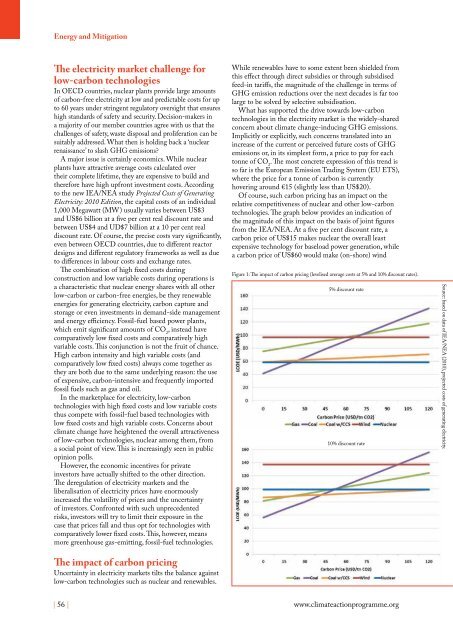

Of course, such carbon pricing has an impact on the<br />

relative competitiveness of nuclear and other low-carbon<br />

technologies. The graph below provides an indication of<br />

the magnitude of this impact on the basis of joint figures<br />

from the IEA/NEA. At a five per cent discount rate, a<br />

carbon price of US$15 makes nuclear the overall least<br />

expensive technology for baseload power generation, while<br />

a carbon price of US$60 would make (on-shore) wind<br />

Figure 1: The impact of carbon pricing (levelised average costs at 5% and 10% discount rates).<br />

5% discount rate<br />

10% discount rate<br />

Source: based on data of IEA/NEA (<strong>2010</strong>), projected costs of generating electricity.<br />

| 56 |<br />

www.climateactionprogramme.org