pago de impuesto al activo. - Interejecutivos

pago de impuesto al activo. - Interejecutivos

pago de impuesto al activo. - Interejecutivos

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

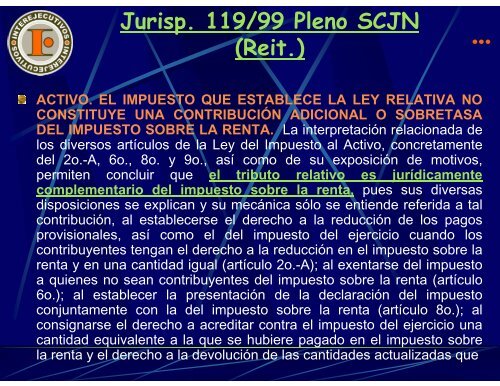

Jurisp. 119/99 Pleno SCJN<br />

(Reit.)<br />

ACTIVO. EL IMPUESTO QUE ESTABLECE LA LEY RELATIVA NO<br />

CONSTITUYE UNA CONTRIBUCIÓN ADICIONAL O SOBRETASA<br />

DEL IMPUESTO SOBRE LA RENTA. La interpretación relacionada <strong>de</strong><br />

los diversos artículos <strong>de</strong> la Ley <strong>de</strong>l Impuesto <strong>al</strong> Activo, concretamente<br />

<strong>de</strong>l 2o.-A, 6o., 8o. y 9o., así como <strong>de</strong> su exposición <strong>de</strong> motivos,<br />

permiten concluir que el tributo relativo es jurídicamente<br />

complementario <strong>de</strong>l <strong>impuesto</strong> sobre la renta, pues sus diversas<br />

disposiciones se explican y su mecánica sólo se entien<strong>de</strong> referida a t<strong>al</strong><br />

contribución, <strong>al</strong> establecerse el <strong>de</strong>recho a la reducción <strong>de</strong> los <strong>pago</strong>s<br />

provision<strong>al</strong>es, así como el <strong>de</strong>l <strong>impuesto</strong> <strong>de</strong>l ejercicio cuando los<br />

contribuyentes tengan el <strong>de</strong>recho a la reducción en el <strong>impuesto</strong> sobre la<br />

renta y en una cantidad igu<strong>al</strong> (artículo 2o.-A); <strong>al</strong> exentarse <strong>de</strong>l <strong>impuesto</strong><br />

a quienes no sean contribuyentes <strong>de</strong>l <strong>impuesto</strong> sobre la renta (artículo<br />

6o.); <strong>al</strong> establecer la presentación <strong>de</strong> la <strong>de</strong>claración <strong>de</strong>l <strong>impuesto</strong><br />

conjuntamente con la <strong>de</strong>l <strong>impuesto</strong> sobre la renta (artículo 8o.); <strong>al</strong><br />

consignarse el <strong>de</strong>recho a acreditar contra el <strong>impuesto</strong> <strong>de</strong>l ejercicio una<br />

cantidad equiv<strong>al</strong>ente a la que se hubiere pagado en el <strong>impuesto</strong> sobre<br />

la renta y el <strong>de</strong>recho a la <strong>de</strong>volución <strong>de</strong> las cantida<strong>de</strong>s actu<strong>al</strong>izadas que

![[Modo de compatibilidad].pdf - Interejecutivos](https://img.yumpu.com/38534396/1/190x245/modo-de-compatibilidadpdf-interejecutivos.jpg?quality=85)