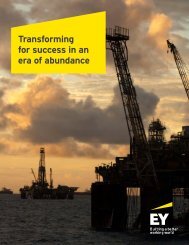

Transforming for success in an era of abundance

6017BWhxb

6017BWhxb

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

As shale producers<br />

<strong>in</strong> the US confront<br />

persistent low oil prices,<br />

the US Shale <strong>in</strong>dustry is<br />

tr<strong>an</strong>s<strong>for</strong>m<strong>in</strong>g, refocus<strong>in</strong>g<br />

on fundamentals <strong>an</strong>d<br />

enter<strong>in</strong>g a new <strong>era</strong><br />

that requires close <strong>an</strong>d<br />

discipl<strong>in</strong>ed attention to<br />

op<strong>era</strong>tional efficiency,<br />

capital structure <strong>an</strong>d<br />

portfolio m<strong>an</strong>agement.<br />

<strong>Tr<strong>an</strong>s<strong>for</strong>m<strong>in</strong>g</strong> <strong>for</strong> <strong>success</strong><br />

<strong>in</strong> <strong>an</strong> <strong>era</strong> <strong>of</strong> abund<strong>an</strong>ce<br />

Our <strong>in</strong>dustry is undergo<strong>in</strong>g a tectonic shift. Gone<br />

are the hopes <strong>for</strong> a V-shaped recovery from the<br />

downturn that started <strong>in</strong> late-2014. Launched<br />

by technology that unlocked shale oil, we have<br />

entered <strong>an</strong> “<strong>era</strong> <strong>of</strong> oil abund<strong>an</strong>ce”, <strong>an</strong>d we are<br />

scrambl<strong>in</strong>g to adapt. With lower th<strong>an</strong> expected<br />

global dem<strong>an</strong>d growth, this <strong>era</strong> <strong>of</strong> abund<strong>an</strong>t<br />

oil supply has s<strong>of</strong>tened market response to<br />

geopolitical triggers <strong>an</strong>d ch<strong>an</strong>ged the global pric<strong>in</strong>g<br />

dynamic. “Unconventional wisdom” now calls <strong>for</strong> a<br />

structurally lower price po<strong>in</strong>t def<strong>in</strong>ed by US Shale<br />

economics, along with expectations <strong>of</strong> compressed<br />

<strong>an</strong>d more frequent price cycles because shale<br />

production c<strong>an</strong> more quickly enter <strong>an</strong>d exit the<br />

market <strong>in</strong> response to price signals.<br />

In the wake <strong>of</strong> these ch<strong>an</strong>ges, the f<strong>in</strong><strong>an</strong>cial community is now view<strong>in</strong>g<br />

the oil <strong>an</strong>d gas sector differently. With breathtak<strong>in</strong>g crude price<br />

decl<strong>in</strong>es, the oil <strong>an</strong>d gas producer risk-return pr<strong>of</strong>ile has ch<strong>an</strong>ged<br />

dramatically, <strong>an</strong>d access to cheap capital — which was a key US<br />

unconventional production growth driver — is decl<strong>in</strong><strong>in</strong>g, especially<br />

from traditional sources such as b<strong>an</strong>ks. Tighter credit liquidity is<br />

also driven by regulatory pressures on traditional lenders that aim<br />

to prevent systemic b<strong>an</strong>k<strong>in</strong>g risks — the Dodd-Fr<strong>an</strong>k effect. Go<strong>in</strong>g<br />

<strong>for</strong>ward, a growth agenda is unlikely to comm<strong>an</strong>d higher multiples.<br />

Stung by recent equity value collapse <strong>an</strong>d <strong>in</strong>solvency fears, <strong>in</strong>vestors<br />

will be far more likely to reward oil <strong>an</strong>d gas comp<strong>an</strong>ies that are agile<br />

<strong>in</strong> capital allocation, adept at optimiz<strong>in</strong>g marg<strong>in</strong> <strong>an</strong>d focused on<br />

reduc<strong>in</strong>g variability <strong>in</strong> free cash flows.<br />

The implications <strong>for</strong> the US onshore exploration <strong>an</strong>d production (E&P)<br />

sector are far-reach<strong>in</strong>g. F<strong>in</strong><strong>an</strong>cial stress result<strong>in</strong>g from drastically<br />

low oil prices <strong>an</strong>d unw<strong>in</strong>d<strong>in</strong>g hedges is creat<strong>in</strong>g signific<strong>an</strong>t turmoil,<br />

especially among the <strong>in</strong>dependents. For example, EY recently<br />

conducted a review <strong>of</strong> the top 100 op<strong>era</strong>tors <strong>in</strong> US onshore, <strong>an</strong>d the<br />

results are sober<strong>in</strong>g. About a third <strong>of</strong> the comp<strong>an</strong>ies are <strong>in</strong> f<strong>in</strong><strong>an</strong>cial<br />

distress <strong>an</strong>d will require some level <strong>of</strong> restructur<strong>in</strong>g <strong>in</strong> the near future<br />

absent a signific<strong>an</strong>t oil price recovery. An estimated 40% to 50% <strong>of</strong><br />

the comp<strong>an</strong>ies are <strong>in</strong> survival mode, with just enough liquidity to<br />

weather the storm <strong>for</strong> the next one to two years. Long expected<br />

merger activity has not materialized among m<strong>an</strong>y <strong>of</strong> these comp<strong>an</strong>ies<br />

due to ch<strong>an</strong>ge <strong>in</strong> control provisions <strong>an</strong>d other negative debt coven<strong>an</strong>t<br />

restrictions. The rema<strong>in</strong><strong>in</strong>g 20% to 30% are <strong>in</strong> position to capitalize on<br />

the downturn with well-considered <strong>in</strong>org<strong>an</strong>ic growth strategies.<br />

An “abund<strong>an</strong>ce <strong>era</strong>” calls <strong>for</strong> tr<strong>an</strong>s<strong>for</strong>mational moves <strong>in</strong> (1) op<strong>era</strong>tional<br />

practices, (2) capital structure <strong>an</strong>d (3) portfolio strategy. M<strong>an</strong>agement<br />

focus will shift through these three components, depend<strong>in</strong>g on the<br />

current comp<strong>an</strong>y condition.<br />

February 2016