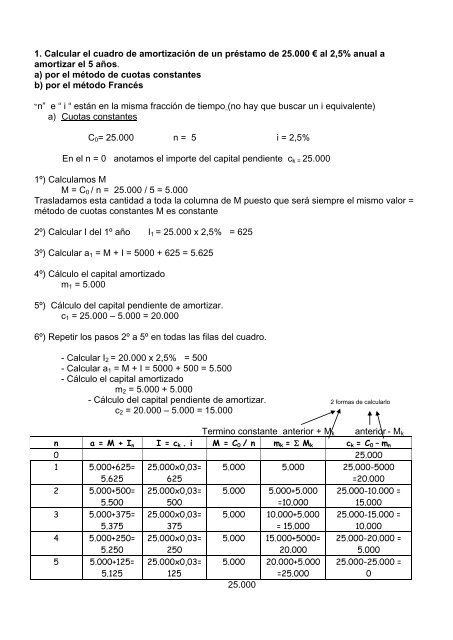

1. Calcular el cuadro de amortización de un préstamo de 25.000 ...

1. Calcular el cuadro de amortización de un préstamo de 25.000 ...

1. Calcular el cuadro de amortización de un préstamo de 25.000 ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>1.</strong> <strong>Calcular</strong> <strong>el</strong> <strong>cuadro</strong> <strong>de</strong> <strong>amortización</strong> <strong>de</strong> <strong>un</strong> <strong>préstamo</strong> <strong>de</strong> <strong>25.000</strong> € al 2,5% anual a<br />

amortizar <strong>el</strong> 5 años.<br />

a) por <strong>el</strong> método <strong>de</strong> cuotas constantes<br />

b) por <strong>el</strong> método Francés<br />

“n” e “ i “ están en la misma fracción <strong>de</strong> tiempo (no hay que buscar <strong>un</strong> i equivalente)<br />

a) Cuotas constantes<br />

C0= <strong>25.000</strong> n = 5 i = 2,5%<br />

En <strong>el</strong> n = 0 anotamos <strong>el</strong> importe d<strong>el</strong> capital pendiente ck = <strong>25.000</strong><br />

1º) Calculamos M<br />

M = C0 / n = <strong>25.000</strong> / 5 = 5.000<br />

Trasladamos esta cantidad a toda la columna <strong>de</strong> M puesto que será siempre <strong>el</strong> mismo valor =<br />

método <strong>de</strong> cuotas constantes M es constante<br />

2º) <strong>Calcular</strong> I d<strong>el</strong> 1º año I1 = <strong>25.000</strong> x 2,5% = 625<br />

3º) <strong>Calcular</strong> a1 = M + I = 5000 + 625 = 5.625<br />

4º) Cálculo <strong>el</strong> capital amortizado<br />

m1 = 5.000<br />

5º) Cálculo d<strong>el</strong> capital pendiente <strong>de</strong> amortizar.<br />

c1 = <strong>25.000</strong> – 5.000 = 20.000<br />

6º) Repetir los pasos 2º a 5º en todas las filas d<strong>el</strong> <strong>cuadro</strong>.<br />

- <strong>Calcular</strong> I2 = 20.000 x 2,5% = 500<br />

- <strong>Calcular</strong> a1 = M + I = 5000 + 500 = 5.500<br />

- Cálculo <strong>el</strong> capital amortizado<br />

m2 = 5.000 + 5.000<br />

- Cálculo d<strong>el</strong> capital pendiente <strong>de</strong> amortizar. 2 formas <strong>de</strong> calcularlo<br />

c2 = 20.000 – 5.000 = 15.000<br />

Termino constante anterior + Mk anterior - Mk<br />

n a = M + In I = ck . i M = C0 / n mk = Mk ck = C0 – mn<br />

0 <strong>25.000</strong><br />

1 5.000+625=<br />

5.625<br />

2 5.000+500=<br />

5.500<br />

3 5.000+375=<br />

5.375<br />

4 5.000+250=<br />

5.250<br />

5 5.000+125=<br />

5.125<br />

<strong>25.000</strong>x0,03=<br />

625<br />

<strong>25.000</strong>x0,03=<br />

500<br />

<strong>25.000</strong>x0,03=<br />

375<br />

<strong>25.000</strong>x0,03=<br />

250<br />

<strong>25.000</strong>x0,03=<br />

125<br />

5.000 5.000 <strong>25.000</strong>-5000<br />

=20.000<br />

5.000 5.000+5.000<br />

=10.000<br />

5.000 10.000+5.000<br />

= 15.000<br />

5.000 15.000+5000=<br />

20.000<br />

5.000 20.000+5.000<br />

=<strong>25.000</strong><br />

<strong>25.000</strong><br />

<strong>25.000</strong>-10.000 =<br />

15.000<br />

<strong>25.000</strong>-15.000 =<br />

10.000<br />

<strong>25.000</strong>-20.000 =<br />

5.000<br />

<strong>25.000</strong>-<strong>25.000</strong> =<br />

0

) Método Frances<br />

C0= <strong>25.000</strong> n = 5 i = 2,5%<br />

1ª fila d<strong>el</strong> <strong>cuadro</strong> = Periodo 0 = solo anotamos la cantidad prestada C0 = capital pendiente <strong>de</strong><br />

amortizar<br />

2ª fila d<strong>el</strong> <strong>cuadro</strong> = Periodo 1<br />

1º) Calculamos la parte constante = cuota <strong>de</strong> <strong>amortización</strong> M<br />

a = C0 / an┐i an┐i = 1 - (1 + i ) - n = 1- (1 + 0,025) -5 = 4,6458<br />

i 0,025<br />

a = <strong>25.000</strong> /4,6458 = 5.381,20<br />

Trasladamos esta cantidad a toda la columna <strong>de</strong> a (anualidad) puesto que será siempre <strong>el</strong><br />

mismo valor = método Francés a es constante<br />

2º) Calculamos la cuota <strong>de</strong> interés I d<strong>el</strong> 1º año<br />

I1 = <strong>25.000</strong> x 0,025 = 625<br />

3º) Calculamos la cuota <strong>de</strong> <strong>amortización</strong> M1<br />

M1 = 5.381,20 - 625 = 4.756,2<br />

4º) Cálculo <strong>el</strong> capital amortizado<br />

m1 = 4.756,2<br />

5º) Cálculo d<strong>el</strong> capital pendiente <strong>de</strong> amortizar.<br />

c1 = <strong>25.000</strong> – 4.756,2 = 20.243,8 2 formas <strong>de</strong> calcularlo<br />

Termino constante anterior + Mk anterior -Mk<br />

n a =C0/an┐i I = ck . i Mk = a - Ik mk = Mk ck = C0 – mn<br />

0 - - - - <strong>25.000</strong><br />

1<br />

5.381,20<br />

<strong>25.000</strong> . 2,5% =<br />

625<br />

2<br />

5.381,20<br />

20.243,8. 2,5% =<br />

506,1<br />

3<br />

5.381,20<br />

15.368,7. 2,5% =<br />

384,22<br />

4<br />

5.381,20<br />

10.371,72. 2,5%<br />

= 259,29<br />

5<br />

5.381,20<br />

5.249,81 . 2,5% =<br />

131,25<br />

5.381,20 – 625 =<br />

4.756,2<br />

5.381,20 – 506,1 =<br />

4.875,1<br />

5.381,20 – 384,22<br />

= 4.996,98<br />

5.381,20 – 259,29<br />

= 5.121,91<br />

5.381,20 –131,25<br />

=5.249,95<br />

4.756,2<br />

4.756,2+4.875,1 =<br />

9.631,3<br />

9.631,3+4.996,98=<br />

14.628,28<br />

14.628,28+5121,91<br />

= 19.750,19<br />

19750,19+5249,95<br />

~ <strong>25.000</strong><br />

<strong>25.000</strong>- 4.756,2 =<br />

20.243,8<br />

<strong>25.000</strong> – 9.631,3 =<br />

15.368,7<br />

<strong>25.000</strong>–14.628,28<br />

= 10.371,72<br />

<strong>25.000</strong> –19.750,19<br />

= 5.249,81<br />

25.0 -<strong>25.000</strong> =<br />

0

2.<strong>Calcular</strong> <strong>el</strong> <strong>cuadro</strong> <strong>de</strong> <strong>amortización</strong> <strong>de</strong> <strong>un</strong> <strong>préstamo</strong> <strong>de</strong> 6.000 € al 3% semestral a<br />

amortizar en 4 anualida<strong>de</strong>s ( en 4 pagos anuales)..<br />

a) por <strong>el</strong> método <strong>de</strong> cuotas constantes<br />

b) por <strong>el</strong> método Francés<br />

i y n no están expresados en no están en la misma fracción <strong>de</strong> tiempo<br />

(1 + i) = (1 + ik) k<br />

Conocemos ik <strong>de</strong>bemos calcular i, <strong>de</strong>spejando<br />

i = (1 + ik) k – 1<br />

i = (1 + 0,03) 2 – 1 = 0,0609<br />

a) Cuotas constantes<br />

C0= 6.000 n = 4 i = 0,0609<br />

En <strong>el</strong> n = 0 anotamos <strong>el</strong> importe d<strong>el</strong> capital pendiente ck = 6.000<br />

1º) Calculamos M<br />

M = C0 / n = 6.000 / 4 = <strong>1.</strong>500<br />

Trasladamos esta cantidad a toda la columna <strong>de</strong> M puesto que será siempre <strong>el</strong> mismo valor =<br />

método <strong>de</strong> cuotas constantes M es constante<br />

2º) <strong>Calcular</strong> I d<strong>el</strong> 1º año I1 = 6.000 x 0,0609 = 365,4<br />

3º) <strong>Calcular</strong> a1 = M + I = <strong>1.</strong>500 + 365,4= <strong>1.</strong>865,4<br />

4º) Cálculo <strong>el</strong> capital amortizado<br />

m1 = <strong>1.</strong>500<br />

5º) Cálculo d<strong>el</strong> capital pendiente <strong>de</strong> amortizar.<br />

c1 = 6.000 – <strong>1.</strong>500 = 4.500<br />

6º) Repetir los pasos 2º a 5º en todas las filas d<strong>el</strong> <strong>cuadro</strong>.<br />

- <strong>Calcular</strong> I2 = 4.500 x 0,0609 = 274,05<br />

- <strong>Calcular</strong> a1 = M + I = <strong>1.</strong>500 + 274,05 = <strong>1.</strong>774,05<br />

- Cálculo <strong>el</strong> capital amortizado<br />

m2 = <strong>1.</strong>500 + <strong>1.</strong>500<br />

- Cálculo d<strong>el</strong> capital pendiente <strong>de</strong> amortizar. 2 formas <strong>de</strong> calcularlo<br />

c2 = 6.000 – 3.000 = 3.000<br />

Termino constante anterior + Mk anterior - Mk<br />

n a = M + In I = ck . i M = C0 / n mk = Mk ck = C0 – mn<br />

0 6.000<br />

1<br />

2<br />

3<br />

4<br />

<strong>1.</strong>500 + 365,4 =<br />

<strong>1.</strong>865,4<br />

<strong>1.</strong>500 + 274,05 =<br />

<strong>1.</strong>774,05<br />

<strong>1.</strong>500 + 182,7 =<br />

<strong>1.</strong>682,7<br />

<strong>1.</strong>500 + 91,35 =<br />

<strong>1.</strong>591,35<br />

6.000x0,0609=<br />

365,4<br />

4.500x0,0609=<br />

274,05<br />

3.000x0,0609=<br />

182,7<br />

<strong>1.</strong>500x0,0609=<br />

91,35<br />

<strong>1.</strong>500 <strong>1.</strong>500<br />

<strong>1.</strong>500<br />

<strong>1.</strong>500<br />

<strong>1.</strong>500<br />

6.000<br />

<strong>1.</strong>500 + <strong>1.</strong>500=<br />

3.000<br />

3.000 + <strong>1.</strong>500=<br />

4.500<br />

4.500 + <strong>1.</strong>500=<br />

6.000<br />

6.000-<strong>1.</strong>500=<br />

4.500<br />

6.000-3.000=<br />

3.000<br />

6.000-4.500<br />

= <strong>1.</strong>500<br />

0

) Método Frances<br />

C0= 6.000 n = 4 i = 0,0609 (calculado anteriormente)<br />

1ª fila d<strong>el</strong> <strong>cuadro</strong> = Periodo 0 = solo anotamos la cantidad prestada C0 = capital pendiente <strong>de</strong><br />

amortizar<br />

2ª fila d<strong>el</strong> <strong>cuadro</strong> = Periodo 1<br />

1º) Calculamos la parte constante = cuota <strong>de</strong> <strong>amortización</strong> M<br />

a = C0 / an┐i an┐i = 1 - (1 + i ) - n = 1- (1 + 0,0609) -4 = 3,4580<br />

i 0,0609<br />

a = 6.000 /3,4580= <strong>1.</strong>735,11<br />

Trasladamos esta cantidad a toda la columna <strong>de</strong> a (anualidad) puesto que será siempre <strong>el</strong><br />

mismo valor = método Francés a es constante<br />

2º) Calculamos la cuota <strong>de</strong> interés I d<strong>el</strong> 1º año<br />

I1 = 6.000 x 0,0609 = 365,4<br />

3º) Calculamos la cuota <strong>de</strong> <strong>amortización</strong> M1<br />

M1 = <strong>1.</strong>735,11 - 365,4 = <strong>1.</strong>369,71<br />

4º) Cálculo <strong>el</strong> capital amortizado<br />

m1 = <strong>1.</strong>369,71<br />

5º) Cálculo d<strong>el</strong> capital pendiente <strong>de</strong> amortizar.<br />

c1 = 6.000 – <strong>1.</strong>369,71= 4.630,29 2 formas <strong>de</strong> calcularlo<br />

Termino constante anterior + Mk anterior -Mk<br />

n a =C0/an┐i I = ck . i Mk = a - Ik mk = Mk ck = C0 – mn<br />

0 - - - - 6.000<br />

1<br />

<strong>1.</strong>735,11<br />

6.000 . 0,0609 =<br />

365,4<br />

2 <strong>1.</strong>735,11 4.630,29. 0,0609<br />

= 281,98<br />

3 <strong>1.</strong>735,11 3.177,16 . 0,0609<br />

= 193,49<br />

4 <strong>1.</strong>735,11 <strong>1.</strong>635,54. 0,0609<br />

= 99,60<br />

<strong>1.</strong>735,11– 365,4<br />

=<strong>1.</strong>369,71<br />

<strong>1.</strong>735,11– 281,98<br />

= <strong>1.</strong>453,13<br />

<strong>1.</strong>735,11– 193,49<br />

= <strong>1.</strong>541,62<br />

<strong>1.</strong>735,11– 99,60=<br />

<strong>1.</strong>635,51<br />

6.000<br />

<strong>1.</strong>369,71<br />

<strong>1.</strong>369,71+<strong>1.</strong>453,13<br />

= 2.822,84<br />

2.822,84+<strong>1.</strong>541,62<br />

=4.364,46<br />

4.364,46+<strong>1.</strong>635,51<br />

~ 6.000<br />

6.000- <strong>1.</strong>369,71=<br />

4.630,29<br />

6.000 – 2.822,84<br />

= 3.177,16<br />

6.000–4.364,46=<br />

<strong>1.</strong>635,54<br />

6.000 –6.000 =<br />

0

Resumen d<strong>el</strong> cálculo <strong>de</strong> <strong>un</strong> <strong>cuadro</strong> <strong>de</strong> <strong>amortización</strong>:<br />

1º) Al igual que en las rentas tenemos que Comprobar que “n” e “ i “ están en la misma<br />

fracción <strong>de</strong> tiempo<br />

En <strong>el</strong> caso <strong>de</strong> que no ocurra esto <strong>de</strong>bemos <strong>de</strong>bemos buscar <strong>un</strong> i equivalente <strong>de</strong>spejando<br />

<strong>de</strong> la formula. formula<br />

(1 + i) = (1 + ik) k<br />

2º) Dependiendo d<strong>el</strong> tipo <strong>de</strong> <strong>préstamo</strong> calculamos <strong>el</strong> término constante<br />

a) Si es <strong>de</strong> Cuotas Constantes, <strong>el</strong> termino constante es M (cuota amortiz). Calculamos M.<br />

M = C0 / n<br />

b) Si es Francés, <strong>el</strong> término constante es a (anualidad). Calculamos a<br />

a =C0/an┐i<br />

3º) Dibujamos <strong>el</strong> <strong>cuadro</strong> <strong>de</strong> <strong>amortización</strong> poniendo siempre los siguientes encabezados<br />

n a I Mk mk = Mk ck = C0 – mn<br />

4º) Anotamos en <strong>el</strong> <strong>cuadro</strong>:<br />

- la 1ªcolumna “n” <strong>de</strong>s<strong>de</strong> 0 a n<br />

- la cantidad prestada C0, (en la 1ª fila , última columna)<br />

- <strong>el</strong> término constante en todas las c<strong>el</strong>das.<br />

Si es por Cutoas Constantes (M es constante) r<strong>el</strong>lenar todas las casillas <strong>de</strong> la columna<br />

con M<br />

Si es Francés (a es constante) r<strong>el</strong>lenar todas las casillas <strong>de</strong> la columna con a<br />

5º) <strong>Calcular</strong> <strong>el</strong> resto <strong>de</strong> casillas