Rohstoffwirtschaftliche Länderstudie - BGR

Rohstoffwirtschaftliche Länderstudie - BGR

Rohstoffwirtschaftliche Länderstudie - BGR

Sie wollen auch ein ePaper? Erhöhen Sie die Reichweite Ihrer Titel.

YUMPU macht aus Druck-PDFs automatisch weboptimierte ePaper, die Google liebt.

Rohstoffsituation Deutschland 2009<br />

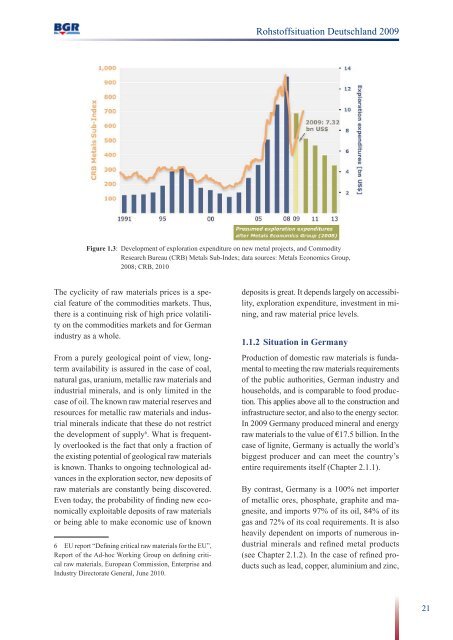

Figure 1.3: Development of exploration expenditure on new metal projects, and Commodity<br />

Research Bureau (CRB) Metals Sub-Index; data sources: Metals Economics Group,<br />

2008; CRB, 2010<br />

The cyclicity of raw materials prices is a special<br />

feature of the commodities markets. Thus,<br />

there is a continuing risk of high price volatility<br />

on the commodities markets and for German<br />

industry as a whole.<br />

From a purely geological point of view, longterm<br />

availability is assured in the case of coal,<br />

natural gas, uranium, metallic raw materials and<br />

industrial minerals, and is only limited in the<br />

case of oil. The known raw material reserves and<br />

resources for metallic raw materials and industrial<br />

minerals indicate that these do not restrict<br />

the development of supply 6 . What is frequently<br />

overlooked is the fact that only a fraction of<br />

the existing potential of geological raw materials<br />

is known. Thanks to ongoing technological advances<br />

in the exploration sector, new deposits of<br />

raw materials are constantly being discovered.<br />

Even today, the probability of finding new economically<br />

exploitable deposits of raw materials<br />

or being able to make economic use of known<br />

6 EU report “Defining critical raw materials for the EU”,<br />

Report of the Ad-hoc Working Group on defining critical<br />

raw materials, European Commission, Enterprise and<br />

Industry Directorate General, June 2010.<br />

deposits is great. It depends largely on accessibility,<br />

exploration expenditure, investment in mining,<br />

and raw material price levels.<br />

1.1.2 Situation in Germany<br />

Production of domestic raw materials is fundamental<br />

to meeting the raw materials requirements<br />

of the public authorities, German industry and<br />

households, and is comparable to food produc-<br />

tion. This applies above all to the construction and<br />

infrastructure sector, and also to the energy sector.<br />

In 2009 Germany produced mineral and energy<br />

raw materials to the value of €17.5 billion. In the<br />

case of lignite, Germany is actually the world’s<br />

biggest producer and can meet the country’s<br />

entire requirements itself (Chapter 2.1.1).<br />

By contrast, Germany is a 100% net importer<br />

of metallic ores, phosphate, graphite and magnesite,<br />

and imports 97% of its oil, 84% of its<br />

gas and 72% of its coal requirements. It is also<br />

heavily dependent on imports of numerous industrial<br />

minerals and refined metal products<br />

(see Chapter 2.1.2). In the case of refined products<br />

such as lead, copper, aluminium and zinc,<br />

21