Guideline on WCT - IRCON's INTRANET SYSTEM!!!

Guideline on WCT - IRCON's INTRANET SYSTEM!!!

Guideline on WCT - IRCON's INTRANET SYSTEM!!!

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

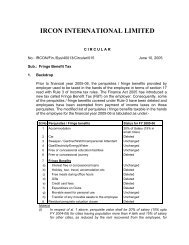

IRCON INTERNATIONAL LIMITED<br />

(A GOVERNMENT OF INDIA UNDERTAKING)<br />

CIRCULAR<br />

IRCON/FIN/TAX/<strong>WCT</strong> CIRCULAR/2003-04 Dt. 10 th March 2003<br />

The Project Head(s)<br />

(All Indian Projects)<br />

SUB.: <str<strong>on</strong>g>Guideline</str<strong>on</strong>g> <strong>on</strong> Works C<strong>on</strong>tract Tax<br />

The <str<strong>on</strong>g>Guideline</str<strong>on</strong>g>s <strong>on</strong> Works C<strong>on</strong>tract Tax (<strong>WCT</strong>) has been finalised and<br />

placed <strong>on</strong> ‘IRCON Intranet’. A hard copy of the <str<strong>on</strong>g>Guideline</str<strong>on</strong>g>s al<strong>on</strong>gwith<br />

annexure is enclosed for ready reference.<br />

The Projects are expected to comply with the <str<strong>on</strong>g>Guideline</str<strong>on</strong>g>s with<br />

immediate effect.<br />

This has approval of Competent Authority.<br />

Copy for informati<strong>on</strong>:<br />

1. PA to MD, DF, DW & CVO<br />

2. All GM/AGM in Corporate Office<br />

3. Advisor - Internal Audit<br />

Sd/-<br />

(S.K.PAL)<br />

(ADDL.GENERAL MANAGER TAX)<br />

1

INTRODUCTION<br />

IRCON INTERNATIONAL LIMITED<br />

Corporate taxati<strong>on</strong> cell<br />

<str<strong>on</strong>g>Guideline</str<strong>on</strong>g> <strong>on</strong> Works C<strong>on</strong>tract Tax<br />

February 2003<br />

Works C<strong>on</strong>tract Tax (here in after referred as <strong>WCT</strong>) is leviable <strong>on</strong> the works<br />

c<strong>on</strong>tractor <strong>on</strong> transfer of title in goods (either as goods or in some other form)<br />

involved in executi<strong>on</strong> of works c<strong>on</strong>tract. The tax is levied by the State in which the<br />

works c<strong>on</strong>tract is executed; and is governed by Sales Tax / <strong>WCT</strong> Act and Rules of<br />

the State. Every State has separate set of Act and Rules. It is therefore necessary<br />

that the <strong>WCT</strong> matters are tackled by the projects locally under guidance of<br />

Corporate Taxati<strong>on</strong> Cell (here-in-after referred as CTC). The services of a local<br />

c<strong>on</strong>sultant/ tax practiti<strong>on</strong>er/ advocate may also be availed for compliance with the<br />

statutory requirements and liais<strong>on</strong> with the sales tax department.<br />

The objectives of this guideline are:<br />

• To ensure effective <strong>WCT</strong> management at different phases of life cycle of a<br />

project (from incepti<strong>on</strong> to the closing of the project).<br />

• To prevent profit leakage.<br />

• To ensure statutory compliance under <strong>WCT</strong> Rules.<br />

• To bring uniformity across the projects.<br />

• To ensure periodical reporting to the CTC.<br />

BIDDING STAGE<br />

The c<strong>on</strong>tracts may be classified in two broad categories from the viewpoint of<br />

<strong>WCT</strong>:<br />

2

1. Prices exclusive of <strong>WCT</strong>- In this case <strong>WCT</strong> does not form part of the price/cost.<br />

The client agrees to reimburse <strong>WCT</strong> separately over and above the agreed price.<br />

Therefore vetting of <strong>WCT</strong> liability by CTC in this type of bids is opti<strong>on</strong>al<br />

2. Prices inclusive of <strong>WCT</strong>- In this case <strong>WCT</strong> forms part of the price/cost.<br />

Profitability is affected by correctness of <strong>WCT</strong> liability included in cost.<br />

Therefore vetting of <strong>WCT</strong> liability by CTC in this type of bid is mandatory<br />

before the same is placed before DF/MD for their c<strong>on</strong>siderati<strong>on</strong>/ approval.<br />

LOI/LOA STAGE<br />

1. The project should refer to the Intranet (www.irc<strong>on</strong>net.com) for general<br />

guidance <strong>on</strong> various provisi<strong>on</strong>s of <strong>WCT</strong> of the State. In case the same is not<br />

available the project should c<strong>on</strong>tact CTC for general guidance.<br />

2. The project should check with the CTC regarding availability of any local<br />

c<strong>on</strong>sultant/tax practiti<strong>on</strong>er/advocate already rendering services to IRCON and<br />

the track record of such local c<strong>on</strong>sultant/tax practiti<strong>on</strong>er/advocate.<br />

3. In case a new local c<strong>on</strong>sultant/tax practiti<strong>on</strong>er/advocate is to be engaged, the<br />

same may be d<strong>on</strong>e by the project in c<strong>on</strong>sultati<strong>on</strong> with the CTC.<br />

4. The law regarding registrati<strong>on</strong> varies from State to State. Some of the States<br />

allow multiple projects to be covered under <strong>on</strong>e registrati<strong>on</strong>. The project should<br />

check with the CTC whether IRCON has any existing sales tax/<strong>WCT</strong><br />

registrati<strong>on</strong> number, which could be used for the new project in the State.<br />

5. In case a fresh registrati<strong>on</strong> number is to be taken, applicati<strong>on</strong> seeking fresh<br />

registrati<strong>on</strong> should be moved by the project immediately and in no case bey<strong>on</strong>d<br />

the permissible time limit under the sales tax/<strong>WCT</strong> law of the State. The<br />

services of the local c<strong>on</strong>sultant/tax practiti<strong>on</strong>er/advocate may be utilised for the<br />

purpose.<br />

6. In some States, the works c<strong>on</strong>tractors are given an opti<strong>on</strong> to pay <strong>WCT</strong> under a<br />

scheme of compositi<strong>on</strong> , which provides for payment of <strong>WCT</strong> at a flat rate,<br />

lower than the normal rate of tax. The method is hassle free and works out to be<br />

cheaper in some cases. The project should check from CTC whether<br />

3

compositi<strong>on</strong> scheme is available in the state and also work out the <strong>WCT</strong> liability<br />

under compositi<strong>on</strong> route vis-a-vi normal route to find out most profitable<br />

opti<strong>on</strong>, specially in case of c<strong>on</strong>tracts with prices inclusive of <strong>WCT</strong>.<br />

7. If compositi<strong>on</strong> opti<strong>on</strong> is intended to be exercised, an applicati<strong>on</strong> should be<br />

moved by the project within the permissible time limit of the sales tax/<strong>WCT</strong> law<br />

of the State. The services of the local c<strong>on</strong>sultant/tax practiti<strong>on</strong>er/advocate may<br />

be utilised for the purpose.<br />

8. If <strong>WCT</strong> is reimbursable by the client over and above the c<strong>on</strong>tract price (price<br />

exclusive of <strong>WCT</strong>) and compositi<strong>on</strong> opti<strong>on</strong> is intended to be exercised by the<br />

project, it should obtain prior c<strong>on</strong>firmati<strong>on</strong> from the client to avoid any future<br />

dispute <strong>on</strong> the subject.<br />

9. Project should check with the CTC whether the tax authorities of the State<br />

entertain requests for exempti<strong>on</strong> from TDS/Deducti<strong>on</strong> of tax at a rate lower than<br />

the normal rate of TDS, prescribed by the sales tax/<strong>WCT</strong> laws of the State.<br />

10. If permitted a certificate should be obtained by the project for exempti<strong>on</strong> from<br />

TDS/Deducti<strong>on</strong> of tax at lower rate. Project should ensure submissi<strong>on</strong> of<br />

applicati<strong>on</strong> in prescribed form within the prescribed time limit. The services of<br />

the local c<strong>on</strong>sultant/tax practiti<strong>on</strong>er/advocate may be utilised for the purpose.<br />

EXECUTION STAGE<br />

1. Project should take initiative either in pers<strong>on</strong> or through the local c<strong>on</strong>sultant/tax<br />

practiti<strong>on</strong>er/advocate to collect Registrati<strong>on</strong> Certificate from Sales Tax/<strong>WCT</strong><br />

Authorities.<br />

2. Project should take initiative either in pers<strong>on</strong> or through the local c<strong>on</strong>sultant/tax<br />

practiti<strong>on</strong>er/advocate to collect permissi<strong>on</strong> for compositi<strong>on</strong> tax from Sales<br />

Tax/<strong>WCT</strong> Authorities.<br />

3. Project should take initiative either in pers<strong>on</strong> or through the local c<strong>on</strong>sultant/tax<br />

practiti<strong>on</strong>er/advocate to collect certificate for exempti<strong>on</strong> from TDS/Deducti<strong>on</strong><br />

of tax at source at lower rate from Sales Tax/<strong>WCT</strong> Authorities.<br />

4. The project should, either in pers<strong>on</strong> or through the local c<strong>on</strong>sultant/tax<br />

practiti<strong>on</strong>er/advocate, take initiative to submit, such informati<strong>on</strong> to the tax<br />

4

authorities of the State, in time, as may be required by the sales tax /<strong>WCT</strong> laws<br />

of the State.<br />

5. The project should ensure that no TDS is effected by the client from the<br />

mobilisati<strong>on</strong> advance. Mobilizati<strong>on</strong> advance is not subject to TDS as no transfer<br />

of property takes place at that stage.<br />

6. The project should ensure that all the sub-c<strong>on</strong>tractors are registered with sales/<br />

works c<strong>on</strong>tract tax authorities and also ensure deducti<strong>on</strong> of TDS from sub-<br />

c<strong>on</strong>tractors' bills at prescribed rate, subject to exempti<strong>on</strong> certificates as may be<br />

produced by the sub-c<strong>on</strong>tractors.<br />

7. The project should also ensure that the TDS effected from the sub-c<strong>on</strong>tractors is<br />

deposited to the Govt. exchequer within the prescribed time limit and the<br />

evidence of such payments are preserved <strong>on</strong> record.<br />

8. The project should ensure issuance of TDS Certificate to the sub-c<strong>on</strong>tractors in<br />

prescribed form, within the prescribed time limit.<br />

9. The project should take initiative to collect TDS certificates from the client and<br />

keep a record of the same.<br />

10. The project should, with the help of the local c<strong>on</strong>sultant/tax<br />

practiti<strong>on</strong>er/advocate, assess the m<strong>on</strong>thly/quarterly/annual <strong>WCT</strong> liability and<br />

arrange to deposit the same to the Govt. exchequer, after adjusting the amount<br />

of TDS deposited by the client. The project should also ensure that the payment<br />

is made before the due date.<br />

11. The project should, with the help of the c<strong>on</strong>sultant/tax practiti<strong>on</strong>er/advocate<br />

prepare sales tax/<strong>WCT</strong> Returns at prescribed interval and submit the same to the<br />

tax authorities <strong>on</strong> or before the due dates.<br />

12. The project should send periodical reports to the CTC in prescribed format for<br />

informati<strong>on</strong> of corporate management.<br />

ASSESSMENT STAGE<br />

1. Project to liais<strong>on</strong> with tax authorities and c<strong>on</strong>sultant/tax practiti<strong>on</strong>er/advocate<br />

5

2. Project to ensure presence before the tax authorities either in pers<strong>on</strong> or through<br />

the c<strong>on</strong>sultant/tax practiti<strong>on</strong>er/advocate for verificati<strong>on</strong> of records/hearing to<br />

complete the assessment expeditiously.<br />

3. On receipt of assessment order the project should examine the same thoroughly<br />

with the help of the local c<strong>on</strong>sultant/tax practiti<strong>on</strong>er/advocate and send a copy<br />

of the same assessment order al<strong>on</strong>g with observati<strong>on</strong> for attenti<strong>on</strong> of the CTC. If<br />

the project proposes to make appeal against the assessment order the same<br />

should be clearly menti<strong>on</strong>ed in the observati<strong>on</strong>.<br />

APPEAL STAGE<br />

1. A competent Council to be engaged by the project in c<strong>on</strong>sultati<strong>on</strong> with CTC.<br />

2. Project should provide complete details and documents to the Council to<br />

prepare appeal papers, grounds of appeal, stay applicati<strong>on</strong> etc and send the draft<br />

copy to CTC for examinati<strong>on</strong> before submissi<strong>on</strong> to the tax authorities. Normally<br />

appeal papers are to be submitted within the specified time limit. Utmost care<br />

has to be taken by the project to ensure that the appeal papers are filed within<br />

the stipulated time limit. Project should inform CTC of submissi<strong>on</strong> of appeal in<br />

time.<br />

3. Project should ensure attendance before the tax authorities either in pers<strong>on</strong> or<br />

through the Council to complete the appellate proceedings expeditiously.<br />

4. On receipt of appellate order the project should examine the same thoroughly<br />

with the help of the Council and send a copy of the same al<strong>on</strong>g with observati<strong>on</strong><br />

for attenti<strong>on</strong> of the CTC. If the project proposes to appeal to next higher<br />

appellant authority the same should be clearly menti<strong>on</strong>ed in the observati<strong>on</strong>.<br />

FINAL CLOSING STAGE<br />

1. Project to intimate Sales Tax/<strong>WCT</strong> authorities regarding financial closure of the<br />

project.<br />

2. The project should take initiative to cancel the Sales Tax/<strong>WCT</strong> Registrati<strong>on</strong>, if it<br />

is exclusively for the project. The project should also inform CTC of such<br />

cancellati<strong>on</strong> of Registrati<strong>on</strong>.<br />

6

*****<br />

7