- Page 2 and 3:

Decision Analysis for Management Ju

- Page 5 and 6:

Decision Analysis for Management Ju

- Page 7:

To Mary and Josephine, Jamie, Jerom

- Page 10 and 11:

viii Contents Chapter 16 The analyt

- Page 12 and 13:

x Foreword real problems, and it is

- Page 14 and 15:

xii Preface accountancy, where rece

- Page 17 and 18:

1 Introduction Complex decisions Im

- Page 19 and 20:

The role of decision analysis 3 you

- Page 21 and 22:

Applications of decision analysis 5

- Page 23 and 24:

Applications of decision analysis 7

- Page 25 and 26:

Applications of decision analysis 9

- Page 27 and 28:

Overview of the book 11 and profit.

- Page 29:

References 13 8. Walls, M. R., Mora

- Page 32 and 33:

16 How people make decisions involv

- Page 34 and 35:

18 How people make decisions involv

- Page 36 and 37:

20 How people make decisions involv

- Page 38 and 39:

22 How people make decisions involv

- Page 40 and 41:

24 How people make decisions involv

- Page 42 and 43:

26 How people make decisions involv

- Page 44 and 45:

28 Decisions involving multiple obj

- Page 46 and 47:

30 Decisions involving multiple obj

- Page 48 and 49:

32 Decisions involving multiple obj

- Page 50 and 51:

34 Decisions involving multiple obj

- Page 52 and 53:

36 Decisions involving multiple obj

- Page 54 and 55:

38 Decisions involving multiple obj

- Page 56 and 57:

40 Decisions involving multiple obj

- Page 58 and 59:

42 Decisions involving multiple obj

- Page 60 and 61:

44 Decisions involving multiple obj

- Page 62 and 63:

46 Decisions involving multiple obj

- Page 64 and 65:

48 Decisions involving multiple obj

- Page 66 and 67:

50 Decisions involving multiple obj

- Page 68 and 69:

52 Decisions involving multiple obj

- Page 70 and 71:

54 Decisions involving multiple obj

- Page 72 and 73:

56 Decisions involving multiple obj

- Page 74 and 75: 58 Decisions involving multiple obj

- Page 76 and 77: 60 Decisions involving multiple obj

- Page 78 and 79: 62 Decisions involving multiple obj

- Page 80 and 81: 64 Decisions involving multiple obj

- Page 82 and 83: 66 Decisions involving multiple obj

- Page 84 and 85: 68 Decisions involving multiple obj

- Page 86 and 87: 70 Decisions involving multiple obj

- Page 88 and 89: 72 Introduction to probability Beca

- Page 90 and 91: 74 Introduction to probability prac

- Page 92 and 93: 76 Introduction to probability we w

- Page 94 and 95: 78 Introduction to probability whet

- Page 96 and 97: 80 Introduction to probability give

- Page 98 and 99: 82 Introduction to probability prob

- Page 100 and 101: 84 Introduction to probability deci

- Page 102 and 103: 86 Introduction to probability that

- Page 104 and 105: 88 Introduction to probability inte

- Page 106 and 107: 90 Introduction to probability subj

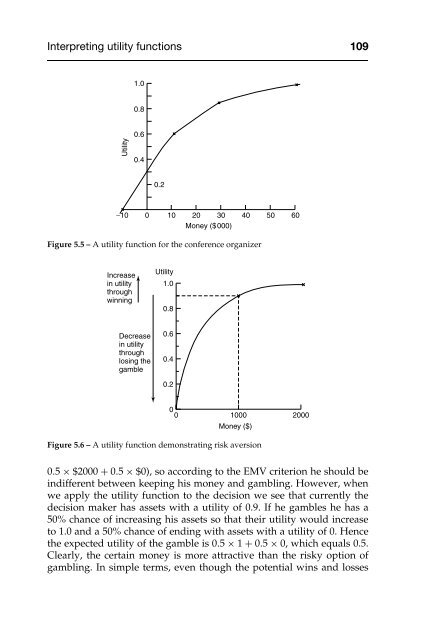

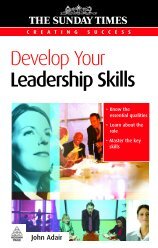

- Page 108 and 109: 92 Introduction to probability (5)

- Page 110 and 111: 94 Introduction to probability (a)

- Page 112 and 113: 96 Decision making under uncertaint

- Page 114 and 115: 98 Decision making under uncertaint

- Page 116 and 117: 100 Decision making under uncertain

- Page 118 and 119: 102 Decision making under uncertain

- Page 120 and 121: 104 Decision making under uncertain

- Page 122 and 123: 106 Decision making under uncertain

- Page 126 and 127: 110 Decision making under uncertain

- Page 128 and 129: 112 Decision making under uncertain

- Page 130 and 131: 114 Decision making under uncertain

- Page 132 and 133: 116 Decision making under uncertain

- Page 134 and 135: 118 Decision making under uncertain

- Page 136 and 137: 120 Decision making under uncertain

- Page 138 and 139: 122 Decision making under uncertain

- Page 140 and 141: 124 Decision making under uncertain

- Page 142 and 143: 126 Decision making under uncertain

- Page 144 and 145: 128 Decision making under uncertain

- Page 146 and 147: 130 Decision making under uncertain

- Page 148 and 149: 132 Decision making under uncertain

- Page 150 and 151: 134 Decision making under uncertain

- Page 152 and 153: 136 Decision making under uncertain

- Page 154 and 155: 138 Decision making under uncertain

- Page 156 and 157: 140 Decision making under uncertain

- Page 159 and 160: 6 Decision trees and influence diag

- Page 161 and 162: Constructing a decision tree 145 be

- Page 163 and 164: Determining the optimal policy 147

- Page 165 and 166: Decision trees and utility 149 succ

- Page 167 and 168: Decision trees involving continuous

- Page 169 and 170: Practical applications of decision

- Page 171 and 172: Assessment of decision structure 15

- Page 173 and 174: Assessment of decision structure 15

- Page 175 and 176:

Eliciting decision tree representat

- Page 177 and 178:

Eliciting decision tree representat

- Page 179 and 180:

Summary 163 where the resulting dec

- Page 181 and 182:

Exercises 165 other elements of the

- Page 183 and 184:

Exercises 167 (b) Assuming that Wes

- Page 185 and 186:

Exercises 169 is not hired, given t

- Page 187 and 188:

Exercises 171 failing to meet the p

- Page 189 and 190:

Exercises 173 why it was rational f

- Page 191 and 192:

Exercises 175 (11) In the Eagle Mou

- Page 193 and 194:

References 177 ABC Chemicals are pl

- Page 195 and 196:

7 Applying simulation to decision p

- Page 197 and 198:

Monte Carlo simulation 181 Of cours

- Page 199 and 200:

Monte Carlo simulation 183 Table 7.

- Page 201 and 202:

Applying simulation to a decision p

- Page 203 and 204:

Applying simulation to a decision p

- Page 205 and 206:

Applying simulation to a decision p

- Page 207 and 208:

Applying simulation to a decision p

- Page 209 and 210:

Applying simulation to a decision p

- Page 211 and 212:

Applying simulation to a decision p

- Page 213 and 214:

Applying simulation to investment d

- Page 215 and 216:

Applying simulation to investment d

- Page 217 and 218:

Applying simulation to investment d

- Page 219 and 220:

Applying simulation to investment d

- Page 221 and 222:

Summary 205 Hull 10 ), some of them

- Page 223 and 224:

Exercises 207 (c) Use your simulati

- Page 225 and 226:

Exercises 209 For each factor the f

- Page 227 and 228:

Exercises 211 (b) Suppose that your

- Page 229:

References 213 6 million Therefore

- Page 232 and 233:

216 Revising judgments in the light

- Page 234 and 235:

218 Revising judgments in the light

- Page 236 and 237:

220 Revising judgments in the light

- Page 238 and 239:

222 Revising judgments in the light

- Page 240 and 241:

224 Revising judgments in the light

- Page 242 and 243:

226 Revising judgments in the light

- Page 244 and 245:

228 Revising judgments in the light

- Page 246 and 247:

230 Revising judgments in the light

- Page 248 and 249:

232 Revising judgments in the light

- Page 250 and 251:

234 Revising judgments in the light

- Page 252 and 253:

236 Revising judgments in the light

- Page 254 and 255:

238 Revising judgments in the light

- Page 256 and 257:

240 Revising judgments in the light

- Page 258 and 259:

242 Revising judgments in the light

- Page 260 and 261:

244 Revising judgments in the light

- Page 263 and 264:

9 Biases in probability assessment

- Page 265 and 266:

Introduction 249 of people watching

- Page 267 and 268:

The availability heuristic 251 make

- Page 269 and 270:

The representativeness heuristic 25

- Page 271 and 272:

The representativeness heuristic 25

- Page 273 and 274:

The representativeness heuristic 25

- Page 275 and 276:

The anchoring and adjustment heuris

- Page 277 and 278:

The anchoring and adjustment heuris

- Page 279 and 280:

Other judgmental biases 263 Other j

- Page 281 and 282:

Is human probability judgment reall

- Page 283 and 284:

Is human probability judgment reall

- Page 285 and 286:

Is human probability judgment reall

- Page 287 and 288:

Exercises 271 Did you receive timel

- Page 289 and 290:

References 273 have been taken from

- Page 291 and 292:

References 275 18. Hamilton, D. L.

- Page 293 and 294:

10 Methods for eliciting probabilit

- Page 295 and 296:

Preparing for probability assessmen

- Page 297 and 298:

Preparing for probability assessmen

- Page 299 and 300:

Preparing for probability assessmen

- Page 301 and 302:

Consistency and coherence checks 28

- Page 303 and 304:

Assessment of the validity of proba

- Page 305 and 306:

Assessment of the validity of proba

- Page 307 and 308:

Assessing probabilities for very ra

- Page 309 and 310:

Exercises 293 Odds in favor of even

- Page 311:

References 295 13. Wright, G. and W

- Page 314 and 315:

298 Risk and uncertainty management

- Page 316 and 317:

300 Risk and uncertainty management

- Page 318 and 319:

302 Risk and uncertainty management

- Page 320 and 321:

304 Risk and uncertainty management

- Page 322 and 323:

306 Risk and uncertainty management

- Page 324 and 325:

308 Risk and uncertainty management

- Page 326 and 327:

310 Decisions involving groups of i

- Page 328 and 329:

312 Decisions involving groups of i

- Page 330 and 331:

314 Decisions involving groups of i

- Page 332 and 333:

316 Decisions involving groups of i

- Page 334 and 335:

318 Decisions involving groups of i

- Page 336 and 337:

320 Decisions involving groups of i

- Page 338 and 339:

322 Decisions involving groups of i

- Page 340 and 341:

324 Decisions involving groups of i

- Page 342 and 343:

326 Decisions involving groups of i

- Page 344 and 345:

328 Decisions involving groups of i

- Page 346 and 347:

330 Resource allocation and negotia

- Page 348 and 349:

332 Resource allocation and negotia

- Page 350 and 351:

334 Resource allocation and negotia

- Page 352 and 353:

336 Resource allocation and negotia

- Page 354 and 355:

338 Resource allocation and negotia

- Page 356 and 357:

340 Resource allocation and negotia

- Page 358 and 359:

342 Resource allocation and negotia

- Page 360 and 361:

344 Resource allocation and negotia

- Page 362 and 363:

346 Resource allocation and negotia

- Page 364 and 365:

348 Resource allocation and negotia

- Page 366 and 367:

350 Resource allocation and negotia

- Page 368 and 369:

352 Resource allocation and negotia

- Page 371 and 372:

14 Decision framing and cognitive i

- Page 373 and 374:

How people frame decisions 357 Figu

- Page 375 and 376:

Imposing imaginary constraints and

- Page 377 and 378:

Inertia in strategic decision makin

- Page 379 and 380:

Studies in the psychological labora

- Page 381 and 382:

Studies in the psychological labora

- Page 383 and 384:

Studies in the psychological labora

- Page 385 and 386:

Overcoming inertia? 369 it is diffi

- Page 387 and 388:

Studies in the psychological labora

- Page 389 and 390:

Discussion questions 373 frame anal

- Page 391 and 392:

References 375 References 1. Luchin

- Page 393 and 394:

15 Scenario planning: an alternativ

- Page 395 and 396:

Introduction 379 documented in Chap

- Page 397 and 398:

Scenario construction: the extreme-

- Page 399 and 400:

Using scenarios in decision making

- Page 401 and 402:

Using scenarios in decision making

- Page 403 and 404:

Scenario construction: the driving

- Page 405 and 406:

Scenario construction: the driving

- Page 407 and 408:

Scenario construction: the driving

- Page 409 and 410:

Case study of a scenario interventi

- Page 411 and 412:

Case study of a scenario interventi

- Page 413 and 414:

Case study of a scenario interventi

- Page 415 and 416:

Case study of a scenario interventi

- Page 417 and 418:

Table 15.1 - The components of the

- Page 419 and 420:

Illustrative case study 403 (b) Att

- Page 421 and 422:

Illustrative case study 405 Stage 4

- Page 423 and 424:

Illustrative case study 407 importa

- Page 425 and 426:

Conclusion 409 combinations. Often

- Page 427:

References 411 2. Van der Heijden,

- Page 430 and 431:

414 The analytic hierarchy process

- Page 432 and 433:

416 The analytic hierarchy process

- Page 434 and 435:

418 The analytic hierarchy process

- Page 436 and 437:

420 The analytic hierarchy process

- Page 438 and 439:

422 The analytic hierarchy process

- Page 440 and 441:

424 The analytic hierarchy process

- Page 443 and 444:

17 Alternative decision-support sys

- Page 445 and 446:

Expert systems 429 generally agreed

- Page 447 and 448:

Expert systems 431 that knowledge e

- Page 449 and 450:

Expert systems 433 (1) That the sub

- Page 451 and 452:

Expert systems 435 information syst

- Page 453 and 454:

Expert systems 437 to focus on ‘t

- Page 455 and 456:

Expert systems 439 On the basis of

- Page 457 and 458:

Is there any intention/expectation

- Page 459 and 460:

Expert systems 443 described above

- Page 461 and 462:

Expert systems 445 body of knowledg

- Page 463 and 464:

Statistical models of judgment 447

- Page 465 and 466:

Statistical models of judgment 449

- Page 467 and 468:

Statistical models of judgment 451

- Page 469 and 470:

Comparisons 453 ‘broken leg’ cu

- Page 471 and 472:

Some final words of advice 455 Ques

- Page 473 and 474:

Some final words of advice 457 of t

- Page 475 and 476:

References 459 Table 17.1 - Summary

- Page 477 and 478:

References 461 20. Eisenhart, J. (1

- Page 479 and 480:

Chapter 3 Suggested answers to sele

- Page 481 and 482:

Suggested answers to selected quest

- Page 483 and 484:

Suggested answers to selected quest

- Page 485:

Suggested answers to selected quest

- Page 488 and 489:

472 Index Brown, C.E. 446 Brown, S.

- Page 490 and 491:

474 Index HIVIEW 58 Hodgkinson, G.P

- Page 492 and 493:

476 Index scenario intervention cas