1 - DePa

1 - DePa

1 - DePa

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

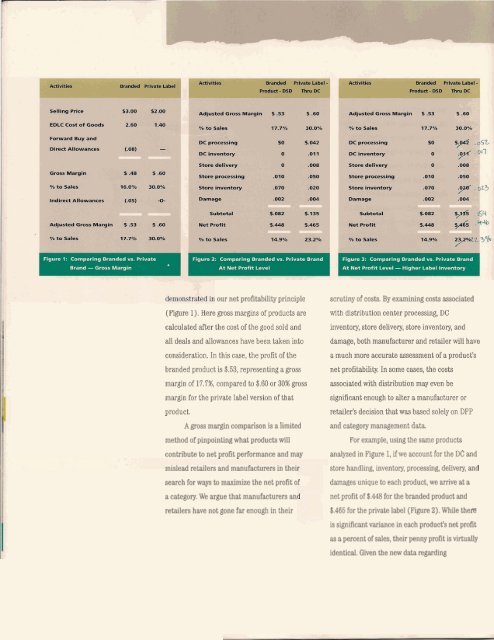

our net profitability principle<br />

(Figure 1). Here gross margins of products are<br />

calculated after the cost of the good sold and<br />

al1 deals and allowances have been taken into<br />

consideration. In this case, the profit of the<br />

branded product is $.53, representing a gross<br />

margin of 17.796, compared to $.60 or 30% gross<br />

margin for the private label version of that<br />

product.<br />

A gross margin comparison is a limited<br />

method of pinpointing what products will<br />

contribute to net profit performance and may<br />

mislead retailers and manufacturen in thei<br />

search for ways to maximize the net profit of<br />

a category. We argue that manufacturen an<br />

retailers have not gone far enough in their<br />

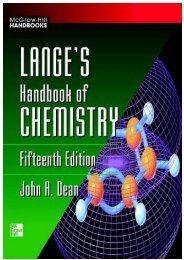

scrutiny of costs. By examining costs associated<br />

with distribution center processing, DC<br />

inventory, store delivery, store inventory, and<br />

damage, both manufacturer and retailer will have<br />

a much more accurate assessment of a product's<br />

net profitability, In some cases, the costs<br />

associated with distribution may even be<br />

significant enough to alter a manufacturer or<br />

retailer's decision that was based solely on DPP<br />

and category management data.<br />

For example, using the same products<br />

analyzed in Figure 1, if we account for the DC and<br />

store handling, inventory, processing, delivery, and<br />

damages unique to each product, we arrive at a<br />

net profit of $.448 for the branded product and<br />

6.465 for the private label (Figure 2). While thefe<br />

is significant variance in each product's net profit<br />

as a percent of sales, their penny profit is virtually<br />

identical. Given the new data regarding

![Síntesis de los isómeros de enlace [Co(NH3)5(ONO)]Cl2 y - DePa](https://img.yumpu.com/16368707/1/190x245/sintesis-de-los-isomeros-de-enlace-conh35onocl2-y-depa.jpg?quality=85)