ESF Guidance Manual 4 Annex 11: Article 13: ESF Verification ...

ESF Guidance Manual 4 Annex 11: Article 13: ESF Verification ...

ESF Guidance Manual 4 Annex 11: Article 13: ESF Verification ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

will follow the procedures set out in the Managing Authority <strong>Manual</strong>.<br />

Extrapolation of irregularities – CFOs<br />

31a. Where A<strong>13</strong> On the Spot verification visits establish that there are<br />

irregularities within one or more subset populations being tested (such as<br />

participants with job outcomes) and they have similar characteristics (such as<br />

missing participant records), the sample will be extended. This will establish<br />

whether or not the irregularity is likely to be repeated within the rest of the<br />

subset population.<br />

If the extended sample establishes that there are similar irregularities, the<br />

principle of extrapolation will apply. The extrapolation will cover the remaining<br />

unchecked population in order to calculate the full extent of the irregularity<br />

within that subset population. A formula will be applied to extrapolate the error<br />

across the whole population under that payment type, provision and claim<br />

period. This process is also in line with A16 procedures.<br />

CFOs should also note that the impact may extend beyond the period tested<br />

to the remaining unchecked subset population, other claims or operations. If<br />

this is the case the CFO will be asked to conduct further work on the<br />

remaining population to identify any additional irregular expenditure. CFOs<br />

should inform the MA of the methodology used, subsets and periods covered<br />

by their audit activities to demonstrate the basis for any additional irregular<br />

expenditure. This work may be reviewed by the Managing and Audit<br />

Authorities.<br />

Coverage<br />

32. All CFOs and all their claims will be subject to <strong>Article</strong> <strong>13</strong> on the spot<br />

verification activity. The selection of the expenditure and providers will be<br />

undertaken on a sample basis. The Managing Authority is required to set a<br />

sample size that achieves ‘reasonable assurance as to the legality and<br />

regularity of the underlying transactions’ (extract from EC guidance).<br />

Following consultation with the Audit Authority, the sample <strong>Article</strong> <strong>13</strong> on the<br />

spot verification at CFO level aims to cover a minimum of 20 per cent of <strong>ESF</strong><br />

and match expenditure claimed, but excluding administrative costs, during the<br />

lifetime of the programme. A key principle is that all providers/sub-contractors<br />

may be the subject of an on the spot check during the lifetime of the<br />

programme. The level and frequency of verification activity is summarised in<br />

the tables below.<br />

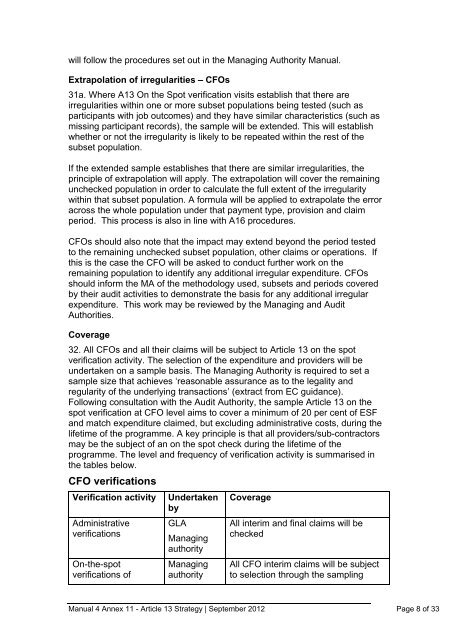

CFO verifications<br />

<strong>Verification</strong> activity<br />

Administrative<br />

verifications<br />

On-the-spot<br />

verifications of<br />

Undertaken<br />

by<br />

GLA<br />

Managing<br />

authority<br />

Managing<br />

authority<br />

Coverage<br />

All interim and final claims will be<br />

checked<br />

All CFO interim claims will be subject<br />

to selection through the sampling<br />

<strong>Manual</strong> 4 <strong>Annex</strong> <strong>11</strong> - <strong>Article</strong> <strong>13</strong> Strategy | September 2012 Page 8 of 33