SSD CONSISTENT CRITERIA AND COHERENT RISK MEASURES

SSD CONSISTENT CRITERIA AND COHERENT RISK MEASURES

SSD CONSISTENT CRITERIA AND COHERENT RISK MEASURES

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

0 < λ < α is efficient under he <strong>SSD</strong> rules. In the case of strong <strong>SSD</strong><br />

safety consistency, every such maximal random variable is, unconditionally,<br />

<strong>SSD</strong> efficient. Therefore, the strong <strong>SSD</strong> safety consistency is an important<br />

property of a risk measure.<br />

The stochastic dominance partial orders are defined on distributions.<br />

The risk measures are commonly considered as functions of random variables.<br />

One may focus on a linear space of random variables L = L k (Ω, F, P)<br />

with some k ≥ 1 (assuming k ≥ 2 whenever variance or any related measure<br />

is considered). Although defined for random variables, typical risk measures<br />

depend only on the corresponding distributions themselves and we focus on<br />

such measures. In other words, we assume that ϱ(X) = ϱ( ˆX) whenever random<br />

variables X and ˆX have the same distribution, i.e. F 1 (X, r) = F 1 ( ˆX, r)<br />

for all r ∈ R or equivalently F −1 (X, p) = F −1 ( ˆX, p) for all p ∈ [0, 1].<br />

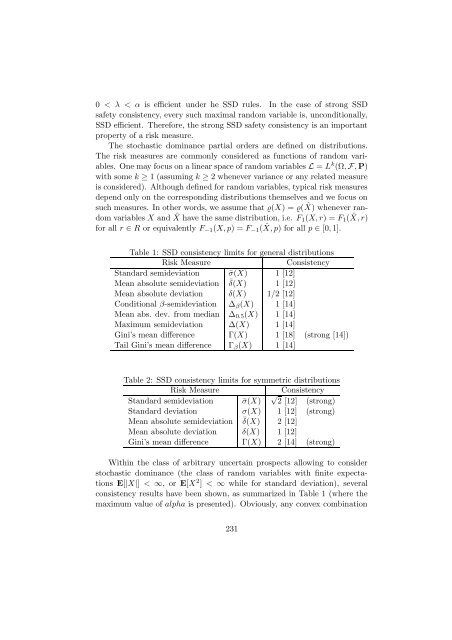

Table 1: <strong>SSD</strong> consistency limits for general distributions<br />

Risk Measure<br />

Consistency<br />

Standard semideviation ¯σ(X) 1 [12]<br />

Mean absolute semideviation ¯δ(X) 1 [12]<br />

Mean absolute deviation δ(X) 1/2 [12]<br />

Conditional β-semideviation ∆ β (X) 1 [14]<br />

Mean abs. dev. from median ∆ 0.5 (X) 1 [14]<br />

Maximum semideviation ∆(X) 1 [14]<br />

Gini’s mean difference Γ(X) 1 [18] (strong [14])<br />

Tail Gini’s mean difference Γ β (X) 1 [14]<br />

Table 2: <strong>SSD</strong> consistency limits for symmetric distributions<br />

Risk Measure<br />

√<br />

Consistency<br />

Standard semideviation ¯σ(X) 2 [12] (strong)<br />

Standard deviation σ(X) 1 [12] (strong)<br />

Mean absolute semideviation ¯δ(X) 2 [12]<br />

Mean absolute deviation δ(X) 1 [12]<br />

Gini’s mean difference Γ(X) 2 [14] (strong)<br />

Within the class of arbitrary uncertain prospects allowing to consider<br />

stochastic dominance (the class of random variables with finite expectations<br />

E[|X|] < ∞, or E[X 2 ] < ∞ while for standard deviation), several<br />

consistency results have been shown, as summarized in Table 1 (where the<br />

maximum value of alpha is presented). Obviously, any convex combination<br />

231