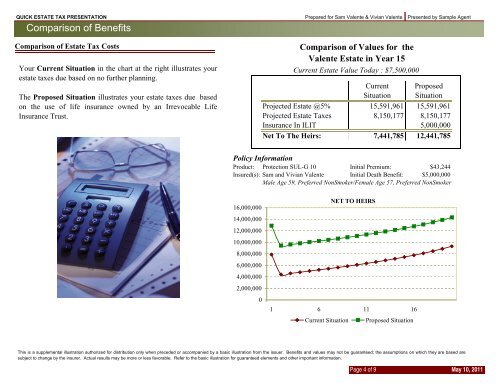

QUICK ESTATE TAX PRESENTATION Comparison of Benefits Comparison of Estate Tax Costs Your Current Situation in the chart at the right illustrates your estate taxes due based on no further planning. The Proposed Situation illustrates your estate taxes due based on the use of life insurance owned by an Irrevocable Life Insurance Trust. Prepared for Sam Valente & Vivian Valente Presented by Sample Agent Comparison of Values for the Valente Estate in Year 15 Current Estate Value Today : $7,500,000 Current Proposed Situation Situation Projected Estate @5% 15,591,961 15,591,961 Projected Estate Taxes 8,150,177 8,150,177 Insurance In ILIT 5,000,000 Net To The Heirs: 7,441,785 12,441,785 Policy Information Product: Protection SUL-G 10 Initial Premium: $43,244 Insured(s): Sam and Vivian Valente Initial Death Benefit: $5,000,000 Male Age 59, Preferred NonSmoker/Female Age 57, Preferred NonSmoker 16,000,000 14,000,000 12,000,000 10,000,000 8,000,000 6,000,000 4,000,000 2,000,000 0 NET TO HEIRS 1 6 11 16 Current Situation Proposed Situation This is a supplemental illustration authorized for distribution only when preceded or accompanied by a basic illustration from the issuer. Benefits and values may not be guaranteed; the assumptions on which they are based are subject to change by the insurer. Actual results may be more or less favorable. Refer to the basic illustration for guaranteed elements and other important information. Page 4 of 9 May 10, 2011

Quick Estate Tax <strong>Presentation</strong> Comparison of Alternatives based on Current Tax Law Prepared for Sam Valente & Vivian Valente Presented by Sample Agent (1) (2) (3) (4) (5) (5) (6) End of Year Proposed Yr. Attained Age Estate Balance (5.0%) Estate Taxes Current Plan Plan Net Net to to Heirs Heirs New ILIT Proceeds Plan Net to Heirs Difference due to to ILIT (1-2) (3+4) (5-3) 1 60/58 7,875,000 0 7,875,000 5,000,000 12,875,000 5,000,000 2 61/59 8,268,750 3,842,813 4,425,938 5,000,000 9,425,938 5,000,000 3 62/60 8,682,188 4,070,203 4,611,984 5,000,000 9,611,984 5,000,000 4 63/61 9,116,297 4,308,963 4,807,334 5,000,000 9,807,334 5,000,000 5 64/62 9,572,112 4,559,661 5,012,450 5,000,000 10,012,450 5,000,000 6 65/63 10,050,717 4,825,430 5,225,287 5,000,000 10,225,287 5,000,000 7 66/64 10,553,253 5,126,952 5,426,301 5,000,000 10,426,301 5,000,000 8 67/65 11,080,916 5,443,549 5,637,366 5,000,000 10,637,366 5,000,000 9 68/66 11,634,962 5,775,977 5,858,985 5,000,000 10,858,985 5,000,000 10 69/67 12,216,710 6,125,026 6,091,684 5,000,000 11,091,684 5,000,000 11 70/68 12,827,545 6,491,527 6,336,018 5,000,000 11,336,018 5,000,000 12 71/69 13,468,922 6,876,353 6,592,569 5,000,000 11,592,569 5,000,000 13 72/70 14,142,369 7,280,421 6,861,947 5,000,000 11,861,947 5,000,000 14 73/71 14,849,487 7,704,692 7,144,795 5,000,000 12,144,795 5,000,000 15 74/72 15,591,961 8,150,177 7,441,785 5,000,000 12,441,785 5,000,000 16 75/73 16,371,559 8,617,936 7,753,624 5,000,000 12,753,624 5,000,000 17 76/74 17,190,137 9,108,776 8,081,362 5,000,000 13,081,362 5,000,000 18 77/75 18,049,644 9,581,504 8,468,140 5,000,000 13,468,140 5,000,000 19 78/76 18,952,126 10,077,870 8,874,257 5,000,000 13,874,257 5,000,000 20 79/77 19,899,733 10,599,053 9,300,680 5,000,000 14,300,680 5,000,000 21 80/78 20,894,719 11,146,296 9,748,424 5,000,000 14,748,424 5,000,000 22 81/79 21,939,455 11,720,900 10,218,555 5,000,000 15,218,555 5,000,000 23 82/80 23,036,428 12,324,235 10,712,193 5,000,000 15,712,193 5,000,000 24 83/81 24,188,250 12,957,737 11,230,512 5,000,000 16,230,512 5,000,000 25 84/82 25,397,662 13,622,914 11,774,748 5,000,000 16,774,748 5,000,000 26 85/83 26,667,545 14,321,350 12,346,195 5,000,000 17,346,195 5,000,000 27 86/84 28,000,922 15,054,707 12,946,215 5,000,000 17,946,215 5,000,000 28 87/85 29,400,969 15,824,733 13,576,236 5,000,000 18,576,236 5,000,000 29 88/86 30,871,017 16,633,259 14,237,758 5,000,000 19,237,758 5,000,000 30 89/87 32,414,568 17,482,212 14,932,356 5,000,000 19,932,356 5,000,000 This is a supplemental illustration authorized for distribution only when preceded or accompanied by a basic illustration from the issuer. Benefits and values may not be guaranteed; the assumptions on which they are based are subject to change by the insurer. Actual results may be more or less favorable. Refer to the basic illustration for guaranteed elements and other important informatio Page 5 of 9 May 10, 2011