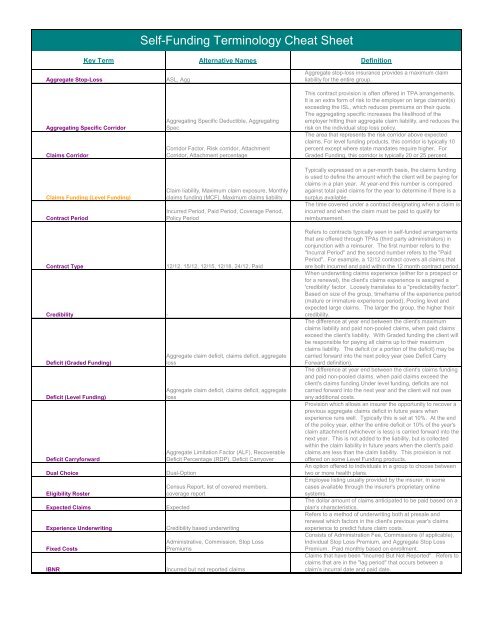

Self-Funding Terminology Cheat Sheet

Self-Funding Terminology Cheat Sheet

Self-Funding Terminology Cheat Sheet

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Self</strong>-<strong>Funding</strong> <strong>Terminology</strong> <strong>Cheat</strong> <strong>Sheet</strong><br />

Key Term Alternative Names Definition<br />

Aggregate Stop-Loss<br />

Aggregating Specific Corridor<br />

Claims Corridor<br />

Claims <strong>Funding</strong> (Level <strong>Funding</strong>)<br />

Contract Period<br />

ASL, Agg<br />

Aggregating Specific Deductible, Aggregating<br />

Spec<br />

Corridor Factor, Risk corridor, Attachment<br />

Corridor, Attachment percentage<br />

Claim liability, Maximum claim exposure, Monthly<br />

claims funding (MCF), Maximum claims liability<br />

Incurred Period, Paid Period, Coverage Period,<br />

Policy Period<br />

Aggregate stop-loss insurance provides a maximum claim<br />

liability for the entire group.<br />

This contract provision is often offered in TPA arrangements.<br />

It is an extra form of risk to the employer on large claimant(s)<br />

exceeding the ISL, which reduces premiums on their quote.<br />

The aggregating specific increases the likelihood of the<br />

employer hitting their aggregate claim liability, and reduces the<br />

risk on the individual stop loss policy.<br />

The area that represents the risk corridor above expected<br />

claims. For level funding products, this corridor is typically 10<br />

percent except where state mandates require higher. For<br />

Graded <strong>Funding</strong>, this corridor is typically 20 or 25 percent.<br />

Typically expressed on a per-month basis, the claims funding<br />

is used to define the amount which the client will be paying for<br />

claims in a plan year. At year-end this number is compared<br />

against total paid claims for the year to determine if there is a<br />

surplus available.<br />

The time covered under a contract designating when a claim is<br />

incurred and when the claim must be paid to qualify for<br />

reimbursement.<br />

Contract Type<br />

Credibility -<br />

Deficit (Graded <strong>Funding</strong>)<br />

Deficit (Level <strong>Funding</strong>)<br />

Deficit Carryforward<br />

Dual Choice<br />

Eligibility Roster<br />

Expected Claims<br />

Experience Underwriting<br />

Fixed Costs<br />

IBNR<br />

12/12, 15/12, 12/15, 12/18, 24/12, Paid<br />

Aggregate claim deficit, claims deficit, aggregate<br />

loss<br />

Aggregate claim deficit, claims deficit, aggregate<br />

loss<br />

Aggregate Limitation Factor (ALF), Recoverable<br />

Deficit Percentage (RDP), Deficit Carryover<br />

Dual-Option<br />

Census Report, list of covered members,<br />

coverage report<br />

Expected<br />

Credibility based underwriting<br />

Administrative, Commission, Stop Loss<br />

Premiums<br />

Incurred but not reported claims<br />

Refers to contracts typically seen in self-funded arrangements<br />

that are offered through TPAs (third party administrators) in<br />

conjunction with a reinsurer. The first number refers to the<br />

"Incurral Period" and the second number refers to the "Paid<br />

Period". For example, a 12/12 contract covers all claims that<br />

are both incurred and paid within the 12 month contract period.<br />

When underwriting claims experience (either for a prospect or<br />

for a renewal), the client's claims experience is assigned a<br />

'credibility' factor. Loosely translates to a "predictability factor".<br />

Based on size of the group, timeframe of the experience period<br />

(mature or immature experience period), Pooling level and<br />

expected large claims. The larger the group, the higher their<br />

credibility.<br />

The difference at year end between the client's maximum<br />

claims liability and paid non-pooled claims, when paid claims<br />

exceed the client's liability. With Graded funding the client will<br />

be responsible for paying all claims up to their maximum<br />

claims liability. The deficit (or a portion of the deficit) may be<br />

carried forward into the next policy year (see Deficit Carry<br />

Forward definition).<br />

The difference at year end between the client's claims funding<br />

and paid non-pooled claims, when paid claims exceed the<br />

client's claims funding.Under level funding, deficits are not<br />

carried forward into the next year and the client will not owe<br />

any additional costs.<br />

Provision which allows an insurer the opportunity to recover a<br />

previous aggregate claims deficit in future years when<br />

experience runs well. Typically this is set at 10%. At the end<br />

of the policy year, either the entire deficit or 10% of the year's<br />

claim attachment (whichever is less) is carried forward into the<br />

next year. This is not added to the liability, but is collected<br />

within the claim liability in future years when the client's paid<br />

claims are less than the claim liability. This provision is not<br />

offered on some Level <strong>Funding</strong> products.<br />

An option offered to individuals in a group to choose between<br />

two or more health plans.<br />

Employee listing usually provided by the insurer, in some<br />

cases available through the insurer's proprietary online<br />

systems.<br />

The dollar amount of claims anticipated to be paid based on a<br />

plan's characteristics.<br />

Refers to a method of underwriting both at presale and<br />

renewal which factors in the client's previous year's claims<br />

experience to predict future claim costs.<br />

Consists of Administration Fee, Commissions (if applicable),<br />

Individual Stop Loss Premium, and Aggregate Stop Loss<br />

Premium. Paid monthly based on enrollment.<br />

Claims that have been "Incurred But Not Reported". Refers to<br />

claims that are in the "lag period" that occurs between a<br />

claim's incurral date and paid date.

Immature Rate<br />

Individual Stop Loss<br />

Lag Report<br />

First Year Rate, 10-Month Rate<br />

ISL, SSL, Specific Stop Loss Level, Pooling<br />

Point, Large Claim Deductible<br />

IBNR report<br />

A reduced pricing structure reserved for the first 12 months of<br />

a plan. Such a rate is possible due to reduced claims liability in<br />

months one and two of a first year plan because of the claim<br />

lag. Fully insured carriers may price at an immature level, but<br />

most often this is seen in <strong>Self</strong>-Funded plans offered through<br />

third party administrators. This arrangement typically results in<br />

a maturing factor being applied at renewal.<br />

Individual stop-loss insurance provides reimbursement in the<br />

event an individual plan participant has claims that exceed the<br />

ISL Level during a contract period. In some states mandate<br />

minimum stop loss levels.<br />

Usually requested for a client's accounting/audit purposes, this<br />

report helps them determine an estimated terminal or runout<br />

liability, based on lag times seen on the plan during the<br />

preceding 12 month period.<br />

Lagged Membership -<br />

Refers to a lag applied to membership. Graded <strong>Funding</strong><br />

applies a 2-month lag to membership for determining monthly<br />

claims liability. When underwriting claims experience, it is also<br />

typical to see a 1 or 2 month lag applied to monthly<br />

membership. In both scenarios, the lag is applied to account<br />

for the relationship between enrollment data and paid claims.<br />

Laser -<br />

This is an additional form of risk to the employer. For large<br />

claimants which may be ongoing, the stop loss carrier alters<br />

the ISL coverage for certain claimant(s). For instance, if the<br />

client's ISL level is $25,000, an individual with a serious<br />

ongoing claim may have their own ISL of $150,000. The<br />

difference between the $25,000 and $150,000 may or may not<br />

accumulate to the employer's aggregate claim liability, which<br />

means they will likely reach or exceed claim liability. Some<br />

carriers do not mandate lasers; however, many will consider<br />

this upon employer or broker request.<br />

Mature Rate - Reflects a full, 12-month claims liability.<br />

Minimum Attachment<br />

Monthly Claim Liability<br />

Non-Pooled Claims<br />

Paid Contract -<br />

Plan Year<br />

Pooled Claims<br />

Premium Statement -<br />

Reinsurance Carrier<br />

MA<br />

Claim liability, Maximum claim exposure,<br />

Aggregate Liability, MAF = Monthly Attachment<br />

Factor (Graded <strong>Funding</strong>), MCF = Monthly Claim<br />

<strong>Funding</strong> (Level <strong>Funding</strong>)<br />

Aggregate Claims, claims under the pooling level<br />

Benefit Period<br />

ISL claims, SSL claims, Specific Claims, Large<br />

Claims, Shock Claims<br />

Reinsurer<br />

Run-In Bridge Protection, 15/12<br />

A provision which sets a minimum claim attachment liability in<br />

the event the client's enrollment shrinks. This allows insurer<br />

and the client to control costs and risk should the enrollment<br />

shrink. Calculated based upon a percentage of enrollment<br />

(can be 90%, 95% or 100%) at the time of renewal. This is<br />

typically not included in Level <strong>Funding</strong> products, but is typically<br />

included in the Graded <strong>Funding</strong> product.<br />

The amount, expressed in dollars per employee (and/or<br />

dependent) per month used to define the claim liability for each<br />

month. See Attachment Factor and Claims <strong>Funding</strong>.<br />

Some <strong>Self</strong>-Funded clients buy insurance protection against<br />

large individual claims. Paid claims up to the ISL threshold are<br />

client liability, and accumulate to the client's aggregate stop<br />

loss limits. Anything over the ISL threshold are Pooled claims.<br />

The term non-pooled literally comes from the fact that these<br />

claims are not "pooled" with other groups claims (see Pooled<br />

Claims definition).<br />

Refers to a self-funded contract which is providing stop loss<br />

protection for all claims Incurred under the life of the policy that<br />

are paid during the 12 month contract period. Some contracts<br />

renew to a paid contract at their first renewal.<br />

The 12-month period in which deductible and coinsurance<br />

accumulates toward a plan participant's out-of-pocket<br />

maximums.<br />

Some <strong>Self</strong>-Funded clients buy insurance protection against<br />

large individual claims. Paid claims exceeding the ISL<br />

threshold are not client liability, and go to the "pool", thereby<br />

becoming pooled claims. Some insurers, at renewal pooled<br />

claims are pulled out of the experience analysis to provide<br />

smaller groups more stability in their renewal increases.<br />

This provides a listing of all employees with coverage levels<br />

and premiums being billed. Premiums reflect Fixed Costs<br />

(administrative fees including commissions and stop loss<br />

premium) only.<br />

This is the stop loss carrier providing ISL and/or ASL<br />

protection to an employer. In a TPA arrangement, this is<br />

usually a third party/entity, and therefore is not integrated.<br />

Claims incurred prior to the first contract year and received<br />

after the new effective date. These claims can be paid under a<br />

"current year" contract that includes a run-in provision. Some<br />

insurers can offer run-in protection on ISL, and must be<br />

coordinated/priced for with underwriting. Pricing differs for<br />

bridge protection versus a 15/12 contract (15/12 is more<br />

protective and therefore has a higher premium, typically).

Run-out<br />

State Premium Taxes<br />

Surplus Share (Level <strong>Funding</strong>)<br />

Surplus (Level <strong>Funding</strong>)<br />

Surplus (Graded <strong>Funding</strong>)<br />

Terminal Deficit Carryforward<br />

Terminal Fees<br />

Terminal Fund (Level <strong>Funding</strong>)<br />

Terminal Fund (Graded <strong>Funding</strong>)<br />

Total Costs<br />

TPA<br />

Year-End Reconciliation (Level <strong>Funding</strong>)<br />

Terminal Liability Period, Incurred but not paid<br />

claims, Run-off liability<br />

Claims funding surplus<br />

Claim surplus<br />

TDC<br />

Terminal Fixed Costs, Terminal ISL+ASL+Admin,<br />

Terminal Protection Costs<br />

Runout Liability, IBNR claims, terminals, reserves<br />

Runout Liability, IBNR claims, terminals, terminal<br />

claim liability, Reserves<br />

Maximum Liability, Fully Funded Rates<br />

Third Party Administrator, Administrator<br />

Year-End Accounting, Surplus Accounting<br />

The run-out period refers to the period of time immediately<br />

following termination, during which time all claims incurred<br />

prior to the termination date are being paid. Timely claims<br />

submission, determination of medical necessity, clarification of<br />

issues and claims processing all contribute to the run-out<br />

period. Most contracts provide 3 months or 6 months of run-out<br />

protection. Some insurers will allow 12-15 months.<br />

An assessment levied by a federal or state government,<br />

usually on the net premium income collected in a particular<br />

jurisdiction. Premium taxes on self-funded plans are typically<br />

lower, since only reinsurance premiums are taxed, whereas<br />

the whole premium in a fully insured plan is taxed.<br />

Refers to the underlying contract feature providing for a 'split'<br />

of year-end surplus. Typically, the split will be 2/3 to the client,<br />

and 1/3 to insurer. Other options include 50/50 and Level 100<br />

(where the client retains full surplus).<br />

Any positive amount remaining from annual claims funding<br />

after paying actual claims and adjusting the terminal fund.<br />

After the terminal fund has been adjusted, the remaining is<br />

split typically can be 1/3 to insurer and 2/3 to the group in the<br />

form of an administrative fee credit. (Note: surplus split will<br />

vary based on situs state and underlying surplus share in<br />

contract)<br />

The positive difference at year end between the client's<br />

maximum claims liability and paid non-pooled claims. This full<br />

amount is retained by the client. Since Graded funding offers<br />

the 'pay as you go' banking arrangement, there is no<br />

reimbursement sent to the client, since the client retains all<br />

unspent claim liability funds in their own bank account.<br />

A feature, standard on most graded funding contracts, which<br />

allows insurer to bring forward a previous surplus or deficit<br />

when determining the client's terminal liability. Applies only to<br />

groups which terminate off-anniversary.<br />

Refers to the Fixed Costs which are charged the month after<br />

termination for graded funding clients. These include costs for<br />

administration of the plan, ISL coverage and ASL coverage for<br />

set # of months after termination. Terminal Fees are typically<br />

125% of the current year's admin, ISL and ASL rates and are<br />

only charged once. Clients should pre-fund in the first year<br />

and hold until termination since most insurers only charge a<br />

set percentage in month 1 and remaining percentage in month<br />

2.<br />

Fund that is pre-funded by the client in the first year, held by<br />

insurer and adjusted annually during the Year-End<br />

Reconciliation. This pays for both terminal runout claims and<br />

terminal fees for level funding clients. With level funding<br />

clients, insurer will typically not owe any additional funds at<br />

termination.<br />

Runout Liability Fund that should be pre-funded by the client in<br />

the first year and held until termination. Graded <strong>Funding</strong><br />

allows an employer to fund a percentage of their terminal<br />

liability in months 1 and 2, since most insurers are billing the<br />

client for that same percentage over month 1 and 2. The<br />

terminal liability is held by the client, and may need to be<br />

adjusted annually based on enrollment changes, claim liability<br />

changes, and benefit changes. Client retains terminal fund<br />

until termination. Graded funding clients are also charged<br />

Terminal Fees.<br />

Total amount of liability each month consisting of<br />

administrative and insurance costs plus monthly claim liability.<br />

For level funding clients, this represents the total payment they<br />

will budget for and pay to insurer each month. For graded<br />

funding clients, this represents the total liability they will budget<br />

and may have to pay to insurer each month.<br />

Refers to the third party/entity administering a plan (plan<br />

documents, paying claims, servicing). May or may not<br />

coordinate with employer and broker on other 'pieces' such as<br />

Rental Network, Disease Management, Wellness Programs,<br />

Reinsurance.<br />

Refers to the reconciliation done by underwriting for insurer's<br />

Level <strong>Funding</strong> clients. Accounts for surplus or deficit under<br />

claims funding, terminal fund adjustment, and then splits<br />

surplus (if applicable) according to surplus share in the<br />

contract. In the case of a deficit, if a level funded product, it<br />

may be written off by insurer and there are no additional<br />

charges to the client.

![[Letter Date] [First Name] [Last Name] [Street Address] [City, State ...](https://img.yumpu.com/49910635/1/190x245/letter-date-first-name-last-name-street-address-city-state-.jpg?quality=85)