Module 6: Capital gains and losses - PD Net

Module 6: Capital gains and losses - PD Net

Module 6: Capital gains and losses - PD Net

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Course Schedule Course <strong>Module</strong>s Review <strong>and</strong> Practice Exam Preparation Resources<br />

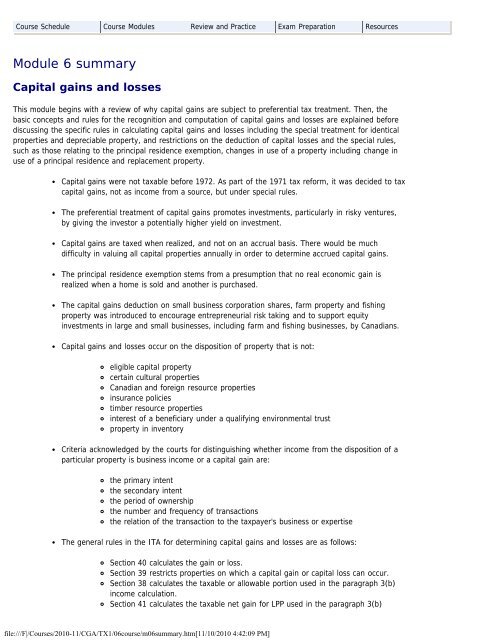

<strong>Module</strong> 6 summary<br />

<strong>Capital</strong> <strong>gains</strong> <strong>and</strong> <strong>losses</strong><br />

This module begins with a review of why capital <strong>gains</strong> are subject to preferential tax treatment. Then, the<br />

basic concepts <strong>and</strong> rules for the recognition <strong>and</strong> computation of capital <strong>gains</strong> <strong>and</strong> <strong>losses</strong> are explained before<br />

discussing the specific rules in calculating capital <strong>gains</strong> <strong>and</strong> <strong>losses</strong> including the special treatment for identical<br />

properties <strong>and</strong> depreciable property, <strong>and</strong> restrictions on the deduction of capital <strong>losses</strong> <strong>and</strong> the special rules,<br />

such as those relating to the principal residence exemption, changes in use of a property including change in<br />

use of a principal residence <strong>and</strong> replacement property.<br />

<strong>Capital</strong> <strong>gains</strong> were not taxable before 1972. As part of the 1971 tax reform, it was decided to tax<br />

capital <strong>gains</strong>, not as income from a source, but under special rules.<br />

The preferential treatment of capital <strong>gains</strong> promotes investments, particularly in risky ventures,<br />

by giving the investor a potentially higher yield on investment.<br />

<strong>Capital</strong> <strong>gains</strong> are taxed when realized, <strong>and</strong> not on an accrual basis. There would be much<br />

difficulty in valuing all capital properties annually in order to determine accrued capital <strong>gains</strong>.<br />

The principal residence exemption stems from a presumption that no real economic gain is<br />

realized when a home is sold <strong>and</strong> another is purchased.<br />

The capital <strong>gains</strong> deduction on small business corporation shares, farm property <strong>and</strong> fishing<br />

property was introduced to encourage entrepreneurial risk taking <strong>and</strong> to support equity<br />

investments in large <strong>and</strong> small businesses, including farm <strong>and</strong> fishing businesses, by Canadians.<br />

<strong>Capital</strong> <strong>gains</strong> <strong>and</strong> <strong>losses</strong> occur on the disposition of property that is not:<br />

eligible capital property<br />

certain cultural properties<br />

Canadian <strong>and</strong> foreign resource properties<br />

insurance policies<br />

timber resource properties<br />

interest of a beneficiary under a qualifying environmental trust<br />

property in inventory<br />

Criteria acknowledged by the courts for distinguishing whether income from the disposition of a<br />

particular property is business income or a capital gain are:<br />

the primary intent<br />

the secondary intent<br />

the period of ownership<br />

the number <strong>and</strong> frequency of transactions<br />

the relation of the transaction to the taxpayer's business or expertise<br />

The general rules in the ITA for determining capital <strong>gains</strong> <strong>and</strong> <strong>losses</strong> are as follows:<br />

Section 40 calculates the gain or loss.<br />

Section 39 restricts properties on which a capital gain or capital loss can occur.<br />

Section 38 calculates the taxable or allowable portion used in the paragraph 3(b)<br />

income calculation.<br />

Section 41 calculates the taxable net gain for LPP used in the paragraph 3(b)<br />

file:///F|/Courses/2010-11/CGA/TX1/06course/m06summary.htm[11/10/2010 4:42:09 PM]

![Management Accounting Fundamentals [MA1]: Module 10 ... - PD Net](https://img.yumpu.com/51417019/1/190x245/management-accounting-fundamentals-ma1-module-10-pd-net.jpg?quality=85)

![Managing Information Systems [MS1]: Module 5 course notes - PD Net](https://img.yumpu.com/49314445/1/190x245/managing-information-systems-ms1-module-5-course-notes-pd-net.jpg?quality=85)

![Financial Accounting - Assets [FA2]: Module 9 course notes - PD Net](https://img.yumpu.com/47639890/1/190x242/financial-accounting-assets-fa2-module-9-course-notes-pd-net.jpg?quality=85)

![Introduction to Personal & Corporate Taxation [TX1] - PD Net](https://img.yumpu.com/46673907/1/190x245/introduction-to-personal-corporate-taxation-tx1-pd-net.jpg?quality=85)