United Spirits Q1FY13 Earnings Conference Call - July ... - UB Group

United Spirits Q1FY13 Earnings Conference Call - July ... - UB Group

United Spirits Q1FY13 Earnings Conference Call - July ... - UB Group

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

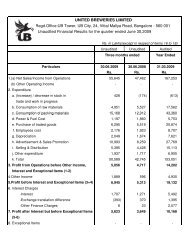

<strong>United</strong> <strong>Spirits</strong><strong>July</strong> 31, 2012capital requirements during the quarter. We have taken many steps to ensure that during thecurrent year there is not much of an expansion in working capital by tightening our bills interms of credit controls etc; we expect almost about 150-200 crores of debtors has to be I meanmonitored and reduced during the current year, so that that much of money can flow into thesystem for managing the working capital much better and so that there is no increasedborrowing on account of working capital. That is what we are tying to do we are put in placevery stringent credit control and I am sure that it will stand in as good stead as we go alongduring the year.Coming to the main subsidiary Whyte & Mackay you would see Whyte and Mackey net salehas dropped to 33 million, from about 37 million and EBITDA has dropped to about 1.9million pounds from 4 million pounds and PBT is loss against break-even last first quarter. Thisis more a timing issue, I would like to reiterate that over the year Whyte & Mackay will getback to the EBITDA level anywhere between 30-35 million pounds I mean during the currentyear also. We have been selling very small parcels of bulk which were there last year andwhich will be there this year with succession of timing and therefore I wouldn't go, I mean, toomuch into the first quarter results of Whyte & Mackay at this point of time and I am alsoconfident that I will go along from second and third quarter onwards we will get back to ourcontribution levels of 26% as compared to 14% that is reported in the first quarter and theEBITDA margin will definitely improve beyond the 11%, I mean, that is the stated year. Sothat is more on the timing issue. But as long as the stock level in Whyte & Mackay isconcerned they still hold almost about 96 million liters of alcohol which as of June almostabout 97 million liters of alcohol as of 30 th June, valued at 531 million pounds by an externalvaluer which shows almost about 81% growth over the stock level on per OLA basis comparedto the value of liquid in May 2007 when we acquired Whyte & Mackay. So there has been anintrinsic growth in the value of the liquid even though we have sold very valuable liquid toDiego in between which was under a contract and therefore this shows that there is an intrinsicvalue growth as far as the liquid is concerned even though the average age of the liquid mighthave come down after we sold valuable liquid in between under contracts That is about theoperating performance of first quarter of USL and its main subsidiary and on the debt level. Asregards the current year outlook as Mr. Capoor explained yes we have taken some priceincreases during the first quarter but we have not taken all of the price increase we probablyhave taken our plan is to take price increase to the extend of almost about 370 crores during thecurrent year out of which probably about 70-80 crores of price increase is yet to be taken andmost of the 270 crores price increase has taken between May and June for the full import of theprice increase will be felt in the quarters going forward and this price increase is as Ashok saidwithout talking about Andhra and we expect Andhra and Kerala price increases to fructify. Infact Kerala, has notified the price increase yesterday about 6% price increase that was onexpected level. In Andhra it is expected to declare the price increases towards the end of thisquarter. So we should have better realization and through price increases during this yearcompared to last year. We have taken almost about 25% more price increases this yearPage 6 of 20