CREDIT RISK SUMMIT - Finance Concepts

CREDIT RISK SUMMIT - Finance Concepts

CREDIT RISK SUMMIT - Finance Concepts

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

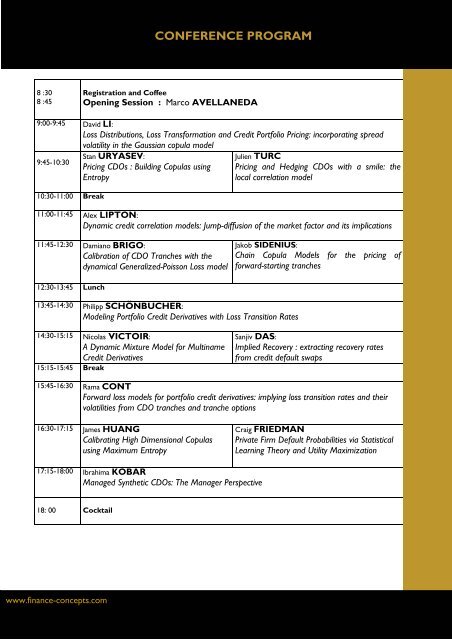

CONFERENCE PROGRAM8 :308 :45Registration and CoffeeOpening Session : Marco AVELLANEDA9:00-9:45 David LI:Loss Distributions, Loss Transformation and Credit Portfolio Pricing: incorporating spreadvolatility in the Gaussian copula model9:45-10:3010:30-11:00 BreakStan URYASEV:Pricing CDOs : Building Copulas usingEntropyJulien TURCPricing and Hedging CDOs with a smile: thelocal correlation model11:00-11:45 Alex LIPTON:Dynamic credit correlation models: Jump-diffusion of the market factor and its implications11:45-12:30 Damiano BRIGO:Calibration of CDO Tranches with thedynamical Generalized-Poisson Loss modelJakob SIDENIUS:Chain Copula Models for the pricing offorward-starting tranches12:30-13:45 Lunch13:45-14:30 Philipp SCHÖNBUCHER:Modeling Portfolio Credit Derivatives with Loss Transition Rates14:30-15:15 Nicolas VICTOIR:A Dynamic Mixture Model for MultinameCredit Derivatives15:15-15:45 BreakSanjiv DAS:Implied Recovery : extracting recovery ratesfrom credit default swaps15:45-16:30 Rama CONTForward loss models for portfolio credit derivatives: implying loss transition rates and theirvolatilities from CDO tranches and tranche optionsRama CONT16:30-17:15 James HUANGCalibrating High Dimensional Copulasusing Maximum EntropyCraig FRIEDMANPrivate Firm Default Probabilities via StatisticalLearning Theory and Utility Maximization17:15-18:00 Ibrahima KOBARManaged Synthetic CDOs: The Manager Perspective18: 00 Cocktailwww.finance-concepts.com