Slides

Slides

Slides

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

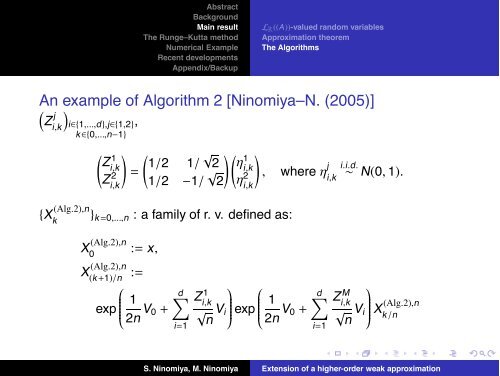

AbstractBackgroundMain resultThe Runge–Kutta methodNumerical ExampleRecent developmentsAppendix/BackupL R ((A))-valued random variablesApproximation theoremThe AlgorithmsAn(example)of Algorithm 2 [Ninomiya–N. (2005)]j Z ,i,ki∈{1,...,d},j∈{1,2}k ∈{0,...,n−1}( ) ( √ )( )Z1i,k 1/2 1/ 2 ηZ 2 =i,k 1/2 −1/ √ 1i,k2 η 2 , where η j i.i.d.∼ N(0, 1).i,ki,k{X (Alg.2),n }k k =0,...,n :afamilyofr.v.definedas:X (Alg.2),n0:= x,X (Alg.2),n :=(k +1)/n⎛1exp ⎜⎝ 2n V 0 +d∑i=1Z 1i,k√ V in⎞⎟⎠⎛⎜⎝ exp 12n V 0 +d∑i=1Z Mi,k√ nV i⎞⎟⎠ X (Alg.2),nk /nS. Ninomiya, M. Ninomiya Extension of a higher-order weak approximation