CEO Remuneration Disclosure Quality: An Australian Perspective

CEO Remuneration Disclosure Quality: An Australian Perspective

CEO Remuneration Disclosure Quality: An Australian Perspective

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

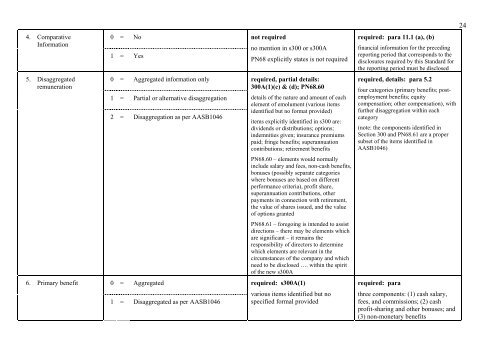

244. ComparativeInformation0 = No1 = Yesnot requiredno mention in s300 or s300APN68 explicitly states is not requiredrequired: para 11.1 (a), (b)financial information for the precedingreporting period that corresponds to thedisclosures required by this Standard forthe reporting period must be disclosed5. Disaggregatedremuneration0 = Aggregated information only1 = Partial or alternative disaggregation2 = Disaggregation as per AASB1046required, partial details:300A(1)(c) & (d); PN68.60details of the nature and amount of eachelement of emolument (various itemsidentified but no format provided)items explicitly identified in s300 are:dividends or distributions; options;indemnities given; insurance premiumspaid; fringe benefits; superannuationcontributions; retirement benefitsrequired, details: para 5.2four categories (primary benefits; postemploymentbenefits; equitycompensation; other compensation), withfurther disaggregation within eachcategory(note: the components identified inSection 300 and PN68.61 are a propersubset of the items identified inAASB1046)PN68.60 – elements would normallyinclude salary and fees, non-cash benefits,bonuses (possibly separate categorieswhere bonuses are based on differentperformance criteria), profit share,superannuation contributions, otherpayments in connection with retirement,the value of shares issued, and the valueof options grantedPN68.61 – foregoing is intended to assistdirections – there may be elements whichare significant – it remains theresponsibility of directors to determinewhich elements are relevant in thecircumstances of the company and whichneed to be disclosed …. within the spiritof the new s300A6. Primary benefit0 = Aggregatedrequired: s300A(1)required: para1 = Disaggregated as per AASB1046various items identified but nospecified formal providedthree components: (1) cash salary,fees, and commissions; (2) cashprofit-sharing and other bonuses; and(3) non-monetary benefits