AA1000 ASSURANCE STANDARD 2008 - AccountAbility

AA1000 ASSURANCE STANDARD 2008 - AccountAbility

AA1000 ASSURANCE STANDARD 2008 - AccountAbility

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

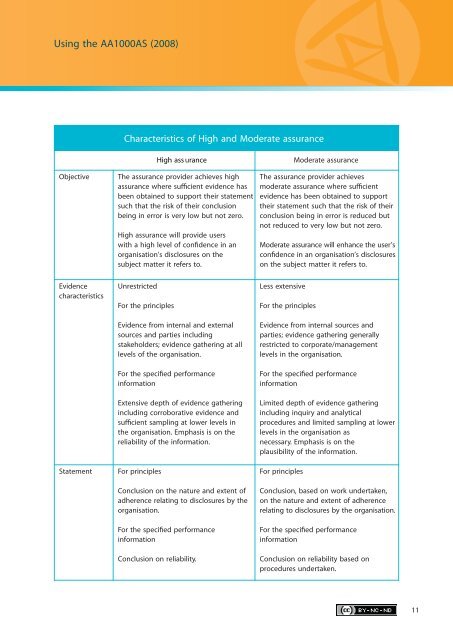

Using the <strong>AA1000</strong>AS (<strong>2008</strong>)Characteristics of High and Moderate assuranceObjectiveHigh ass uranceThe assurance provider achieves highassurance where sufficient evidence hasbeen obtained to support their statementsuch that the risk of their conclusionbeing in error is very low but not zero.High assurance will provide userswith a high level of confidence in anorganisation’s disclosures on thesubject matter it refers to.Moderate assuranceThe assurance provider achievesmoderate assurance where sufficientevidence has been obtained to supporttheir statement such that the risk of theirconclusion being in error is reduced butnot reduced to very low but not zero.Moderate assurance will enhance the user’sconfidence in an organisation’s disclosureson the subject matter it refers to.EvidencecharacteristicsStatementUnrestrictedFor the principlesEvidence from internal and externalsources and parties includingstakeholders; evidence gathering at alllevels of the organisation.For the specified performanceinformationExtensive depth of evidence gatheringincluding corroborative evidence andsufficient sampling at lower levels inthe organisation. Emphasis is on thereliability of the information.For principlesConclusion on the nature and extent ofadherence relating to disclosures by theorganisation.For the specified performanceinformationConclusion on reliability.Less extensiveFor the principlesEvidence from internal sources andparties; evidence gathering generallyrestricted to corporate/managementlevels in the organisation.For the specified performanceinformationLimited depth of evidence gatheringincluding inquiry and analyticalprocedures and limited sampling at lowerlevels in the organisation asnecessary. Emphasis is on theplausibility of the information.For principlesConclusion, based on work undertaken,on the nature and extent of adherencerelating to disclosures by the organisation.For the specified performanceinformationConclusion on reliability based onprocedures undertaken.11