“Everything goes well but also can failbecause of relationships.”ßMeasurable and attained metrics: Understandably,clearly measured improvements in service levels tocustomers (55%) and clearly measured cost reductions(48%) are also cited as contributing factors tosuccessful 3PL relationships.The takeaway: Setting, and then driving toward, a commonlyheld set of expectations is an essential element of success.Interestingly, the larger the revenue group, the moreimportance 3PL users place on a carefully designed and signedcontract that supports innovative arrangements between a3PL and a customer. Although this was not a specific area ofinquiry within the <strong>2008</strong> survey, one plausible explanation isthat higher-revenue companies may be more sensitive aboutcarefully drafted contracts, as they may have more at stakefinancially and otherwise. Also, higher-revenue companiesmay have policies and procedures in place that requireuse of a more formal agreement or contract that includes acommensurate level of detail.Results are slightly more mixed when respondents are askedwhether “3PLs provide us with new and innovative waysto improve logistics effectiveness.” A full 90% of those inLatin America agree, compared with 72% in North America,61% in Asia Pacific, and 46% in Europe. Clearly, theimpact of 3PLs on logistics effectiveness differs among thegeographies studied. As indicated below, however, many ofthese same companies also indicate room for improvementwith the service offerings that are provided.Interesting findings within these results include:ßßßßAlmost two-thirds feel their use of 3PL services hashad a positive impact on the services they provide totheir own customers.The same fraction indicate their use of 3PLs has positivelyimpacted business process efficiencies.Slightly less than half of 3PL users say their 3PLsprovide them with visibility into key processessuch as warehouse management, transportationmanagement and supply chain management.About 40% are able to measure return on investment(ROI) from using a 3PL. While this finding may seemsurprising considering the high marks 3PL userstypically give their 3PL relationships, as discussedpreviously, it may be that some users are makingmore qualitative, rather than quantitative, judgments.Of course, no relationship, or service provider, is perfect.Some 3PL users report areas in which their 3PLs couldimprove. The most frequently occurring issues, as reportedin Figure 5, are those one would naturally expect: unrealizedservice-level commitments, lack of continuous improvementsand achievements in offerings, and cost reductions notrealized. As in past surveys, insufficient IT capabilities arealso an issue. This topic is discussed in greater detail below.Figure 5: Customers Also Report a Number ofContinuing Problems with 3PL ProvidersOutsourced <strong>Logistics</strong> ServiceThere is also room for improvement in 3PL managementcapabilities: Approximately one-third of 3PL users reportproblems with a lack of project management skills,ineffective management of key performance indicators andunsatisfactory transition during the implementation stage.What 3PL Users SpendAll RegionsService level commitments not realized 51%Lack of continuous, ongoing improvements and achievements inofferingsInformation technology capabilities not sufficient 39Cost reductions not realized 36Lack of project management skills 35Ineffective management of key performance indicators (KPIs) 34Unsatisfactory transition during implementation stage 30Errors caused by excessive manual steps within businessprocessesLack of global capabilities 27Lack of consultative/knowledge-based skills 25Lack of business process integration across regions and supplychain servicesInability to form meaningful and trusting relationships 17Poor post-merger integration of acquired companies 13No problems 12Another area the survey probes each year is the totalpercentage of current logistics expenditures directed tooutsourcing. For <strong>2008</strong>, respondents in North America planto devote 49%, in Europe it’s 61%, Asia Pacific averages57%, and Latin American respondents will allocate 48%.Within three to five years, 3PL users expect these proportionsto grow: North America to 56%, Europe to 69%, Asia Pacificto 64%, and Latin America to 59%.Interestingly, a look back at results from this question forthe past few years reveals there does not appear to be anymeasurable growth from year to year in the percentages ofoverall logistics expenditures for 3PL services. Since total42282012

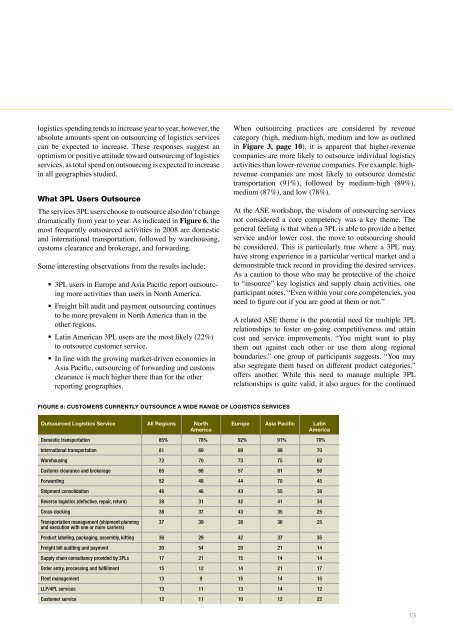

logistics spending tends to increase year to year, however, theabsolute amounts spent on outsourcing of logistics servicescan be expected to increase. These responses suggest anoptimism or positive attitude toward outsourcing of logisticsservices, as total spend on outsourcing is expected to increasein all geographies studied.What 3PL Users OutsourceThe services 3PL users choose to outsource also don’t changedramatically from year to year. As indicated in Figure 6, themost frequently outsourced activities in <strong>2008</strong> are domesticand international transportation, followed by warehousing,customs clearance and brokerage, and forwarding.Some interesting observations from the results include:ßßßß3PL users in Europe and Asia Pacific report outsourcingmore activities than users in North America.Freight bill audit and payment outsourcing continuesto be more prevalent in North America than in theother regions.Latin American 3PL users are the most likely (22%)to outsource customer service.In line with the growing market-driven economies inAsia Pacific, outsourcing of forwarding and customsclearance is much higher there than for the otherreporting geographies.When outsourcing practices are considered by revenuecategory (high, medium-high, medium and low as outlinedin Figure 3, page 10), it is apparent that higher-revenuecompanies are more likely to outsource individual logisticsactivities than lower-revenue companies. For example, highrevenuecompanies are most likely to outsource domestictransportation (91%), followed by medium-high (89%),medium (87%), and low (78%).At the ASE workshop, the wisdom of outsourcing servicesnot considered a core competency was a key theme. Thegeneral feeling is that when a 3PL is able to provide a betterservice and/or lower cost, the move to outsourcing shouldbe considered. This is particularly true where a 3PL mayhave strong experience in a particular vertical market and ademonstrable track record in providing the desired services.As a caution to those who may be protective of the choiceto “insource” key logistics and supply chain activities, oneparticipant notes, “Even within your core competencies, youneed to figure out if you are good at them or not.”A related ASE theme is the potential need for multiple 3PLrelationships to foster on-going competitiveness and attaincost and service improvements. “You might want to playthem out against each other or use them along regionalboundaries,” one group of participants suggests. “You mayalso segregate them based on different product categories,”offers another. While this need to manage multiple 3PLrelationships is quite valid, it also argues for the continuedFigure 6: Customers Currently Outsource a Wide range of <strong>Logistics</strong> ServicesOutsourced <strong>Logistics</strong> Service All Regions NorthAmericaEurope Asia Pacific LatinAmericaDomestic transportation 85% 78% 92% 91% 70%International transportation 81 69 89 89 70Warehousing 72 70 73 75 62Customs clearance and brokerage 65 66 57 81 56Forwarding 52 48 44 70 45Shipment consolidation 46 46 43 55 38Reverse logistics (defective, repair, return) 38 31 42 41 34Cross-docking 38 37 43 35 25Transportation management (shipment planningand execution with one or more carriers)37 39 38 36 25Product labeling, packaging, assembly, kitting 36 29 42 37 35Freight bill auditing and payment 30 54 20 21 14Supply chain consultancy provided by 3PLs 17 21 15 14 14Order entry, processing and fulfillment 15 12 14 21 17Fleet management 13 9 15 14 15LLP/4PL services 13 11 13 14 12Customer service 12 11 10 12 2213