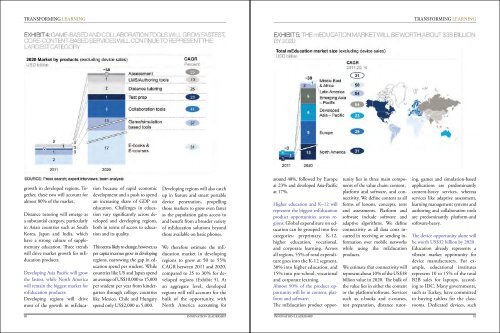

TRANSFORMING LEARNINGTRANSFORMING LEARNINGstudents and tailor lessons to theirneeds. This is just one example ofmEducation’s tremendous potential.ENHANCING EDUCATIOALOUTCOMES USING MOBILETECHNOLOGYOur research shows that mEducationoffers three advantages withthe potential to improve educationdelivery and thereby enhancelearning outcomes:• It simplifies access to contentand experts, overcoming traditionalconstraints of time, locationand collaboration• It personalizes education solutionsfor individual learners,helping educators customize theteaching process, using softwareand interactive media that adaptlevels of difficulty to individualstudents’ understanding and pace• It addresses specific challengesthat lower the efficiency of educationalsystems worldwide. Casein point: MIT’s Education CollaborationServices gives teachersaccess to best practices.THE REVOLUTION IS COM-INGThe market for mEducation productsand services today is worthapproximately US$3.4 billion—asliver of the US$4 trillion spent oneducation globally. But students,educators and e-learning playersare warming up to the potentialof mEducation. Five trends createa fertile environment to supportmEducation growth:Portable device form factors arerapidly evolving. Increased availabilityand penetration of smartportable devices with advancedfunctionalities, such as accelerometersthat sense motion, willlower costs and open a world ofnew possibilities for mEducationsolutionsA digital native and technologyliterategeneration is fast emerging.We are adopting mobile solutionsand devices in our lives ata faster pace. Children will adaptespecially well to learning throughmobile devicesGovernments are turning to thepotential of mEducation. Manycountries are promoting the use ofinformation and communicationstechnology in schools and investingin portable devices that enablenew ways of learning – all in a bidto improve learning outcomesMobile applications are increasinglypopular for educationalcontent. More recently, mobiledevice users are downloading educationalapps at higher prices thanentertainment or gaming appsPilots are leading to viable productswith commercial potential,such as mobile-based learningmanagement systems, game-basedapplications, and voice and textbasedsolutions. This is in turnattracting more investment intomEducation providers.THE M-EDUCATION PROD-UCT LANDSCAPEAlthough mEducation is a nascentmarket, publishing houses, mobilenetwork operators and devicemanufacturers have been focusingon it for years. We have classifiedmore than hundred commercialmEducation offerings into sevenproduct and solution archetypes:(i) educational e-books and coursesaccessed through portable devices;(ii) learning management systems(LMS) and authoring tools;(iii) game or simulation-basedlearning tools;(iv) collaboration tools(v) adaptive assessment services;(vi) test preparation support(vii) distance tutoring and homework support.SIZING THE M-EDUCATIONOPPORTUNITYThe world is spending more oneducation than ever before. By2020, we expect global spend todouble to US$8 trillion. mEducationmay address up to US$70billion of this market throughspecialized product offerings anda growing market for devices.mEducation products can representa USD 38 billion marketopportunity by 2020 The sevenproduct and solution archetypesof mEducation could be a US$38billion revenueopportunity by2020. Looking at the mEducationmarket along three conventionaldimensions—geographic, endusersegments and value chaincomponents—we foresee the followingtrends:• Education spend will grow thefastest in developing Asia-Pacificat a CAGR of 54% between2011-20, while North Americawill remain the biggest market inabsolute terms with a total annualspend of US$15 billion for mEducationproducts and solutionsby 2020• 75-80% of spending willbe in higher education and K-12,while corporate learning will accountfor 10-20%, varying bymarket• In parallel with online educationspend, almost 90% of mEducationservices will rely oncontent-enabling platforms andsoftware.The device opportunity alone willbe worth US$32 billion by 2020.With the anticipated growth inmEducation, manufacturers arelikely to see rapid growth in demandfor dedicated devices for usein education. While most of thegrowth, around US$30 billion,will be for B2B (educational institutions)solutions, we estimatethe B2C (individual learners) categorywill grow to around US$2billion over the same period.HOW MOBILE OPERATORSCAN TAP THE MARKETDepending on their aspirationsand capabilities, mobile operatorscan tap the potential of mEducationin three ways:• Ride the connectivity wave:This is the immediate opportunityfor mobile operators and wherethey have the most natural rightto play. It will be worth approximatelyUS$4 billion in annualrevenue by 2020• Enable the mEducation ecosystem:mEducation providers willrequire a broad range of technicalsupport and enablers such asIT, network, content, hosting anddata management services. Mobileoperators can develop theircapabilities to offer this support,tapping into a revenue pool of approximatelyUS$20 billionLead as an end-to-end mEducationprovider: MNOs can investupfront and enter the market ontheir own, providing the entirerange of services that include inhousecontent and/or devices.This throws open the entire mEducationopportunity, worth approximatelyUS$70 billion.mEducation, now at a tippingpoint, offers significant opportunitiesfor mobile operators, whileenhancing educational access andoutcomes for learners and educatorsaround the world.The mEducation opportunity canbe US$70 billion by 2020Growing consistently at about 7%per annum over the last decade,education spend has doubledfrom about US$2 trillion in 2000to US$4 trillion in 2011 and is expectedto grow at 8% per annumto reach US$8 trillion by 2020.The opportunity for mEducationwill also grow rapidly over this decade.We expect the total annual marketopportunity for mEducationto reach US$70 billion by 2020.mEducation products representUS$38 billion of this figure, whilethe remaining US$32 billion willcome from the sale of devices.mEducation products will representa US$38 billion marketopportunity by 2020Together, the seven archetypes ofmEducation products will representa US$38 billion annual revenueopportunity in 2020 (Exhibit 4).E-books and e-courses deliveredover mobile networks and accessedon portable devices will continueto represent the biggest productsegment on the back of stronggrowth in developing regions.This will be followed by game- andsimulation-based tools, which willemerge as the second significantcategory, on the back of strong88 <strong>INNOVATION</strong> <strong>LEADERSHIP</strong> <strong>INNOVATION</strong> <strong>LEADERSHIP</strong> 89

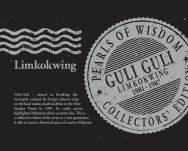

TRANSFORMING LEARNINGTRANSFORMING LEARNINGgrowth in developed regions. Together,these two will account foralmost 80% of the market.Distance tutoring will emerge asa substantial category, particularlyin Asian countries such as SouthKorea, Japan and India, whichhave a strong culture of supplementaryeducation. Three trendswill drive market growth for mEducationproducts.Developing Asia Pacific will growthe fastest, while North Americawill remain the biggest market formEducation products:Developing regions will drivemost of the growth in mEducationbecause of rapid economicdevelopment and a push to spendan increasing share of GDP oneducation. Challenges in educationvary significantly across developedand developing regions,both in terms of access to educationand its quality.This seems likely to change, however, asper capita incomes grow in developingregions, narrowing the gap in educationspend per student. Whilecountries like US and Japan spendan average of US$10,000 to 15,000per student per year from kindergartenthrough college, countrieslike Mexico, Chile and Hungaryspend only US$2,000 to 5,000.Developing regions will also catchup in feature and smart portabledevice penetration, propellingthose markets to grow even fasteras the population gains access toand benefit from a broader varietyof mEducation solutions beyondthose available on basic phones.We therefore estimate the mEducationmarket in developingregions to grow at 50 to 55%CAGR between 2011 and 2020,compared to 25 to 30% for developedregions (Exhibit 5). Atan aggregate level, developedregions will still account for thebulk of the opportunity, withNorth America accounting foraround 40%, followed by Europeat 23% and developed Asia-Pacificat 17%.Higher education and K–12 willrepresent the biggest mEducationproduct opportunities across regions:Global expenditure on educationcan be grouped into fivecategories: preprimary, K-12,higher education, vocational,and corporate learning. Acrossall regions, 55% of total expendituregoes into the K-12 segment,30% into higher education, and15% into pre-school, vocationaland corporate learning.Almost 90% of the product opportunitywill be in content, platformand software:The mEducation product opportunitylies in three main componentsof the value chain: content,platform and software, and connectivity.We define content as allforms of lessons, concepts, testsand assessments. Platform andsoftware include software andadaptive algorithms. We defineconnectivity as all data costs incurredin receiving or sending informationover mobile networkswhile using the mEducationproducts.We estimate that connectivity willrepresent about 10% of the US$38billion value in 2020. The bulk ofthe value lies in either the contentor the platform/software. Servicessuch as e-books and e-courses,test preparation, distance tutoring,games and simulation-basedapplications are predominantlycontent-heavy services, whereasservices like adaptive assessment,learning management systems andauthoring and collaboration toolsare predominantly platform-andsoftware-heavy.The device opportunity alone willbe worth US$32 billion by 2020Education already represents avibrant market opportunity fordevice manufacturers. For example,educational institutesrepresent 10 to 15% of the totalB2B sales for laptops, accordingto IDC. Many governments,such as Turkey, have committedto buying tablets for the classrooms.Dedicated devices, such90 <strong>INNOVATION</strong> <strong>LEADERSHIP</strong> <strong>INNOVATION</strong> <strong>LEADERSHIP</strong> 91