ACFE - Cross Border Investigations (Part 1)

Confronting the challengesof #cross-border #fraudexaminations by #RobinSingh the #whitecollarinvestigator

Confronting the challengesof #cross-border #fraudexaminations by #RobinSingh the #whitecollarinvestigator

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

FRAUD BASICS<br />

Fundamentals for all<br />

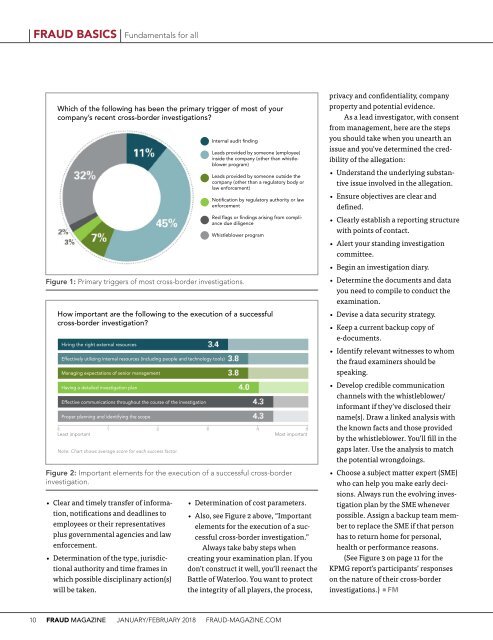

Which of the following has been the primary trigger of most of your<br />

company’s recent cross-border investigations?<br />

Internal audit finding<br />

Leads provided by someone (employee)<br />

inside the company (other than whistleblower<br />

program)<br />

Leads provided by someone outside the<br />

company (other than a regulatory body or<br />

law enforcement)<br />

Notification by regulatory authority or law<br />

enforcement<br />

Red flags or findings arising from compliance<br />

due diligence<br />

Whistleblower program<br />

privacy and confidentiality, company<br />

property and potential evidence.<br />

As a lead investigator, with consent<br />

from management, here are the steps<br />

you should take when you unearth an<br />

issue and you’ve determined the credibility<br />

of the allegation:<br />

• Understand the underlying substantive<br />

issue involved in the allegation.<br />

• Ensure objectives are clear and<br />

defined.<br />

• Clearly establish a reporting structure<br />

with points of contact.<br />

• Alert your standing investigation<br />

committee.<br />

• Begin an investigation diary.<br />

Figure 1: Primary triggers of most cross-border investigations.<br />

How important are the following to the execution of a successful<br />

cross-border investigation?<br />

Hiring the right external resources<br />

Effectively utilizing internal resources (including people and technology tools)<br />

Managing expectations of senior management<br />

Having a detailed investigation plan<br />

Effective communications throughout the course of the investigation<br />

Proper planning and identifying the scope<br />

Least important<br />

Note: Chart shows average score for each success factor.<br />

Most important<br />

• Determine the documents and data<br />

you need to compile to conduct the<br />

examination.<br />

• Devise a data security strategy.<br />

• Keep a current backup copy of<br />

e-documents.<br />

• Identify relevant witnesses to whom<br />

the fraud examiners should be<br />

speaking.<br />

• Develop credible communication<br />

channels with the whistleblower/<br />

informant if they’ve disclosed their<br />

name(s). Draw a linked analysis with<br />

the known facts and those provided<br />

by the whistleblower. You’ll fill in the<br />

gaps later. Use the analysis to match<br />

the potential wrongdoings.<br />

Figure 2: Important elements for the execution of a successful cross-border<br />

investigation.<br />

• Clear and timely transfer of information,<br />

notifications and deadlines to<br />

employees or their representatives<br />

plus governmental agencies and law<br />

enforcement.<br />

• Determination of the type, jurisdictional<br />

authority and time frames in<br />

which possible disciplinary action(s)<br />

will be taken.<br />

• Determination of cost parameters.<br />

• Also, see Figure 2 above, “Important<br />

elements for the execution of a successful<br />

cross-border investigation.”<br />

Always take baby steps when<br />

creating your examination plan. If you<br />

don’t construct it well, you’ll reenact the<br />

Battle of Waterloo. You want to protect<br />

the integrity of all players, the process,<br />

• Choose a subject matter expert (SME)<br />

who can help you make early decisions.<br />

Always run the evolving investigation<br />

plan by the SME whenever<br />

possible. Assign a backup team member<br />

to replace the SME if that person<br />

has to return home for personal,<br />

health or performance reasons.<br />

(See Figure 3 on page 11 for the<br />

KPMG report’s participants’ responses<br />

on the nature of their cross-border<br />

investigations.) n FM<br />

10 FRAUD MAGAZINE JANUARY/FEBRUARY 2018 FRAUD-MAGAZINE.COM