Applied Econometrics

Applied Econometrics

Applied Econometrics

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

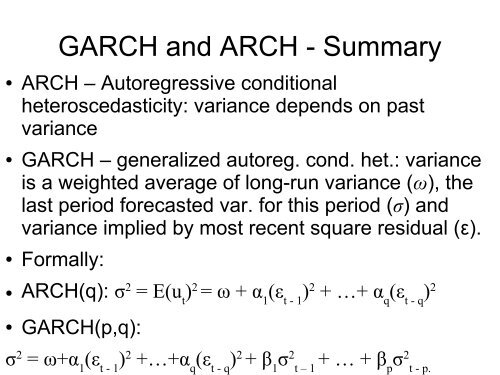

GARCH and ARCH - Summary<br />

● ARCH – Autoregressive conditional<br />

heteroscedasticity: variance depends on past<br />

variance<br />

● GARCH – generalized autoreg. cond. het.: variance<br />

is a weighted average of long-run variance (ω), the<br />

last period forecasted var. for this period (σ) and<br />

variance implied by most recent square residual (ε).<br />

● Formally:<br />

● ARCH(q): σ 2 = E(u t ) 2 = ω + α 1 (ε t - 1 ) 2 + …+ α q (ε t - q ) 2<br />

● GARCH(p,q):<br />

σ 2 = ω+α 1 (ε t - 1 ) 2 +…+α q (ε t - q ) 2 + β 1 σ 2<br />

t – 1 + … + β p σ2<br />

t - p.