âAño del Estado de Derecho y de Gobernabilidad Democráticaâ

âAño del Estado de Derecho y de Gobernabilidad Democráticaâ

âAño del Estado de Derecho y de Gobernabilidad Democráticaâ

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

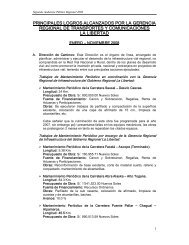

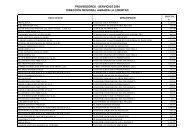

SUB GERENCIA DECONTABILIDADNOTA A LOS ESTADOS FINANCIEROS - PLIEGO 451 - GOBIERNO REGIONAL LALIBERTAD AL 31 DE DICIEMBRE DEL 2005NOTA 01 : ACTIVIDAD DE LA ENTIDADLa Entidad Gobierno Regional La Libertad, fue creada mediante Ley Nº 27867 Ley Orgánica <strong>de</strong>Gobiernos Regionales publicada el 16 <strong>de</strong> Noviembre <strong><strong>de</strong>l</strong> 2002, modificada por Ley Nº 27902, publicada el01 <strong>de</strong> Enero <strong><strong>de</strong>l</strong> 2003, tiene como finalidad esencial fomentar el Desarrollo Regional Integral sostenible <strong><strong>de</strong>l</strong>a Región La Libertad, integrada 29 Unida<strong>de</strong>s Ejecutoras.Tiene como misión primordial organizar y conducir la gestión pública regional <strong>de</strong> acuerdo a suscompetencias exclusivas compartidas y <strong><strong>de</strong>l</strong>egadas en el marco <strong>de</strong> las políticas nacionales y sectoriales,para contribuir al <strong>de</strong>sarrollo integral y sostenible <strong>de</strong> la Región, utilzando los recursos y las competenciasasignadas con eficiencia y eficacia.NOTA 02 : PRINCIPALES PRACTICAS CONTABLESLos <strong>Estado</strong>s Financieros muestran la situación financiera, los resultados y los flujos <strong>de</strong> efectivo <strong>de</strong> laEntidad y tiene como finalidad suministrar información útil para la toma <strong>de</strong> <strong>de</strong>cisiones, así como efectuarla rendición <strong>de</strong> cuentas <strong>de</strong> los recursos recibidos y ejecutados durante el ejercicio 2005.Los principios y prácticas contables principales, aplicados para el registro <strong>de</strong> operaciones y preparación<strong>de</strong> los <strong>Estado</strong>s Financieros , son:a) Los <strong>Estado</strong>s Financieros han sido preparados <strong>de</strong> acuerdo a Principios <strong>de</strong> ContabilidadGubernamental Aceptados que constituyen la base teórica sobre la cual se fundamenta el procesocontable gubernamental y es complementada por los Instructivos Contables emitidos por laContaduría Pública <strong>de</strong> la Nación, como la Resolución <strong>de</strong> Contaduría Nº 189-05 – EF/93.01 queaprueba el Instructivo Nº 23-2004-EF/93.11 “CIERRE CONTABLE Y PRESENTACION DEINFORMACION PARA LA CUENTA GENERAL DE LA REPUBLICA”.b) El proceso <strong>de</strong> la Contabilización <strong>de</strong> las Operaciones Contables Administrativas se efectúa <strong>de</strong>conformidad con la Resolución Vice Ministerial Nº 029-98-EF/11 que establece la obligatoriedad<strong>de</strong> la utilización <strong><strong>de</strong>l</strong> Sistema Integrado <strong>de</strong> Administración Financiera <strong><strong>de</strong>l</strong> Sector Publico (SIAF –SP), para el registro <strong>de</strong> los datos relacionados con la ejecución <strong>de</strong> ingresos y gastos, que se llevaa cabo en las Unida<strong>de</strong>s Ejecutoras <strong><strong>de</strong>l</strong> Presupuesto <strong><strong>de</strong>l</strong> Sector Público a Nivel Nacional.c) Los <strong>Estado</strong>s Financieros <strong><strong>de</strong>l</strong> Pliego Gobierno Regional La Libertad al 29 <strong>de</strong> Diciembre <strong><strong>de</strong>l</strong>2006, compren<strong>de</strong> la consolidación <strong>de</strong> la información contable y presupuestaria <strong>de</strong> 29 Unida<strong>de</strong>sEjecutoras:Se<strong>de</strong> Central, Dirección Regional <strong>de</strong> Agricultura, Dirección Regional <strong>de</strong> Transporte, DirecciónRegional <strong>de</strong> Educación, UGEL Chepén, UGEL Pacasmayo, UGEL Ascope, UGEL Gran Chimú,UGEL Otuzco, UGEL Santiago <strong>de</strong> Chuco, UGEL Sánchez Carrión , UGEL Pataz, , UGELBolívar, UGEL Julcán, Colegio Militar Ramón Castilla, Dirección Regional <strong>de</strong> Salud, InstitutoLos Brillantes Nº 650 Urb. Santa Inés – Trujillo.Telefax 231305

AgroSciences, Indianapolis), diflubenzuron(MicromiteÒ 80WGS; Chemtura,Middlebury, CT), fenpropathrin(Danitol 2.4 EC; Valent, WalnutCreek, CA), and zeta-cypermethrin(Mustang; FMC, Phila<strong><strong>de</strong>l</strong>phia). Allof these Special Local Needs labelsrequire air-blast or air-assisted sprayerswith application rates of no less than2 gal/acre and with volume mediandroplet diameters of 90 mm or larger.Most labels allow the addition ofadjuvants or other tank-mix partnersas long as the other restrictions aremaintained; however, fenpropathrindoes not allow use of additional adjuvants.No information is given regardingthe reasoning behind the90-mm lower limit, though it is likelybased on risk assessment analysis forspray drift. The Special Local Needslabels also do not specify an upperlimit on the droplet size. Given thatspray droplet size is <strong>de</strong>pen<strong>de</strong>nt on andchanges with varying combinationsof spray equipment, equipment setup,and spray product (Hoffmann et al.,2007b), the objectives of this workwere: 1) evaluate three sprayers, un<strong>de</strong>rlaboratory conditions, for dropletsize produced from a.i. formulationsand the necessary equipment adjustmentsnee<strong>de</strong>d to meet the SpecialLocal Needs label; 2) conduct ‘‘onsite’’evaluations of production applicationequipment for droplet sizewhen operating un<strong>de</strong>r normal conditions;3) adjust the individual sprayer’soperating parameters to produce a volumemedian diameter of 90 mm orgreater to ensure compliance with theSpecial Local Needs labels; and 4)document the general operationalmodifications required for machinetype to provi<strong>de</strong> guidance for futurespray calibrations.Materials and methodsSprayer droplet size testing wascompleted in two stages: one lookingat three sprayers and five a.i. un<strong>de</strong>rlaboratory conditions and the second,a field-based evaluation of productionsprayers brought to a central locationby local applicators. The first laboratory-basedwork was conducted atthe U.S. Department of Agriculture-Agricultural Research Service (USDA-ARS) Areawi<strong>de</strong> Pest ManagementResearch Unit’s Riversi<strong>de</strong> campus facilitiesin College Station, TX. The threesprayers to be evaluated were provi<strong>de</strong>dby the equipment manufacturers. Thefield-based evaluations were conductedat two locations in centralFlorida. Both sets of trials followedthe same testing protocols with theexception of the field-based trials notusing a.i. formulations. These procedures,along with greater <strong>de</strong>tails on thesite-specific testing, are discussed furtherin the following sections.GENERAL TESTING PROCEDURES.To evaluate the droplet size producedby a particular sprayer and spray formulationcombination, the sprayerwas first operated un<strong>de</strong>r its normalfactory or user-established settings.Basically, the sprayer was initially operatedas-is. A droplet measurementsystem (Sympatec, Clausthal, Germany)mounted on a custom-ma<strong>de</strong>forklift mount was used to measuredroplet size at the sprayer nozzleoutlet. The unit was positioned suchthat the location of measurement was1 to 2 m from the outlet of thesprayer (Fig. 1). This distance variedsomewhat from sprayer to sprayer<strong>de</strong>pending on the droplet <strong>de</strong>nsity ofthe resulting spray cloud and thewidth of the spray plume. Wi<strong>de</strong>r sprayplumes required a closer distance toavoid <strong>de</strong>positing spray material on thelenses of the droplet measurementunit. Denser sprays required furtherdistance to insure that the spray cloud<strong>de</strong>nsity did not prevent the diffractedlaser light from reaching the measurementsensor. The spray cloud fromthe sprayer was directed through thelaser beam for 10 to 20 s duringwhich time droplet size measurementsof the spray cloud were ma<strong>de</strong>.The time that the spray cloud wasdirected through the optical path ofthe laser varied between sprayers<strong>de</strong>pending on the width of the sprayplume generated by the sprayer. Theentire spray plume for each sprayerwas measured by traversing the laserthrough the plume using the forklift(ASTM International, 2009). Threereplicated measures were ma<strong>de</strong> foreach unique piece of equipment andspecific set of operational conditions.DROPLET SIZING SYSTEM. TheHelos laser diffraction droplet sizingsystem (Sympatec), which uses a 623-nm helium-neon laser, was fitted withan R5 lens, resulting in a dynamic sizerange from 0.5 to 875 mm in 32 sizingbins. The authors found that whenusing the laser system un<strong>de</strong>r adverseconditions (outdoors and mountedto a forklift), the last channel (i.e.,sizing bins) of the Helos systemshould be turned off such that it isnot factored into the droplet sizemeasurement results. This channelrepresents the largest droplet sizeand tends to pick up some ‘‘noise’’or random signals that typically resultfrom equipment vibration or scatteredambient light. With this channelturned off, the dynamic range of theinstrument was from 0.5 to 735 mm.These channels were not turned off ifany droplets were measured withintwo sizing bins of the nearest <strong>de</strong>activatedchannel.The spray droplet size data were<strong>de</strong>termined and reported as a meanand standard <strong>de</strong>viation correspondingto the data measured during thethree replications for each combinationof sprayer and pestici<strong>de</strong>. Meansand standard <strong>de</strong>viations of the volumemedian diameter [VMD or D V0.5(ASTM International E1620-97,2004)], D V0.1 , and D V0.9 were <strong>de</strong>termined.The D V0.5 is the dropletdiameter in micrometers where 50%of the spray volume is contained indroplets smaller than this value (ASTMFig. 1. Testing setup showing the droplet measurement system with the sprayplume from the citrus sprayer directed through the laser beam of the dropletmeasurement system.• June 2010 20(3) 633

SUB GERENCIA DECONTABILIDADn) El Cálculo <strong>de</strong> Provisión para Beneficios Sociales <strong>de</strong> los Trabajadores Nombrados se ha efectuado<strong>de</strong> acuerdo al Inciso c) Art. 54º <strong><strong>de</strong>l</strong> Decreto Legislativo Nº 276 “Ley <strong>de</strong> la Carrera Administrativa<strong><strong>de</strong>l</strong> Servidor Público” modificado por la Ley Nº 25524, Ley <strong><strong>de</strong>l</strong> Profesorado y su ReglamentoDecreto Supremo Nº 19990 – ED, Ley <strong><strong>de</strong>l</strong> Profesional Médico Decreto Ley Nº 559.o) La empresa ASFALL S.A. En Proceso <strong>de</strong> Formación no muestra inversión <strong>de</strong> Capital <strong><strong>de</strong>l</strong>Gobierno Regional; y la Cartera Pesada <strong>de</strong> Ex Fon<strong>de</strong>agro en proceso Legal <strong>de</strong> Recuperación ytransferencia; en Cuentas <strong>de</strong> Or<strong>de</strong>n.p) Para el registro <strong>de</strong> Gasto e Ingreso, se consi<strong>de</strong>ra el gasto <strong>de</strong>vengado y el ingreso realizado enconcordancia a los Principios <strong>de</strong> Contabilidad Generalmente Aceptados.q) Los ingresos y gastos por intereses son reconocidos en los resuilatdos a medida que se <strong>de</strong>vengan,tomando en cuenta el principio <strong>de</strong> ralización y la Norma Internacional <strong>de</strong> Contabilidad para elSector Público – NICSP Nª 9 INGRESOS PROVENIENTES DE TRANSACCIONES DEINTERCAMBIO.Los Brillantes Nº 650 Urb. Santa Inés – Trujillo.Telefax 231305