informazioni imu saldo 2012 - Comune di Poviglio

informazioni imu saldo 2012 - Comune di Poviglio

informazioni imu saldo 2012 - Comune di Poviglio

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

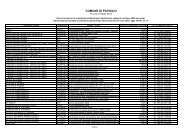

COMUNE DI POVIGLIO<br />

SALDO IMU <strong>2012</strong> - IMPOSTA MUNICIPALE PROPRIA SPERIMENTALE<br />

5,0<br />

Aliquota agevolata del 5 per mille (<strong>di</strong> totale competenza comunale):<br />

ABITAZIONE PRINCIPALE e relative pertinenze C/2, C/6, C/7<br />

• Unica unità immobiliare e pertinenze nel quale il possessore e il suo nucleo familiare<br />

<strong>di</strong>morano abitualmente e risiedono anagraficamente. Nel caso in cui i componenti del<br />

nucleo familiare abbiano stabilito la <strong>di</strong>mora abituale e la residenza anagrafica in<br />

immobili <strong>di</strong>versi situati nel territorio comunale, le agevolazioni per l’abitazione principale<br />

e per le relative pertinenze in relazione al nucleo familiare si applicano per un solo<br />

immobile.<br />

• Unità immobiliare e pertinenze posseduta da anziano o <strong>di</strong>sabile che acquisiscono<br />

la residenza in istituti <strong>di</strong> ricovero o sanitari a seguito <strong>di</strong> ricovero permanente, a<br />

con<strong>di</strong>zione che la stessa non risulti locata.<br />

• Unità immobiliari e pertinenze appartenenti alle cooperative e<strong>di</strong>lizie a proprietà<br />

in<strong>di</strong>visa, a<strong>di</strong>bite ad abitazione principale dei soci assegnatari, nonché agli alloggi<br />

regolarmente assegnati dagli Istituti autonomi per le case popolari (in entrambi i casi<br />

si applica la sola detrazione base prevista per l’abitazione principale <strong>di</strong> € 200,00).<br />

• Unità immobiliare e pertinenze della casa coniugale assegnata al coniuge, a<br />

seguito <strong>di</strong> provve<strong>di</strong>mento <strong>di</strong> separazione legale, annullamento, scioglimento o<br />

cessazione degli effetti civili del matrimonio che, ai soli fini dell’applicazione dell’IMU, si<br />

intende, in ogni caso, assegnata a titolo <strong>di</strong> <strong>di</strong>ritto <strong>di</strong> abitazione.<br />

DETRAZIONI PER ABITAZIONE PRINCIPALE<br />

Dall’imposta annua lorda dovuta per l’abitazione principale e per le relative pertinenze,<br />

compete una detrazione fino a concorrenza del suo ammontare <strong>di</strong><br />

€ 200,00 rapportata al periodo dell’anno in cui si utilizza l’immobile come abitazione principale e<br />

ripartita in parti uguali tra i soggetti proprietari che vi <strong>di</strong>morano abitualmente e vi risiedono<br />

anagraficamente. Per gli anni <strong>2012</strong> e 2013 la detrazione <strong>di</strong> € 200,00 è maggiorata <strong>di</strong> € 50,00 per<br />

ogni figlio <strong>di</strong> età non superiore a 26 anni purchè <strong>di</strong>morante abitualmente e residente<br />

anagraficamente nell’unità immobiliare a<strong>di</strong>bita ad abitazione principale, per un importo massimo<br />

<strong>di</strong> € 400,00 che si aggiunge alla detrazione base <strong>di</strong> € 200,00.<br />

7,6 Aliquota agevolata del 7,6 (<strong>di</strong> cui 3,8 al <strong>Comune</strong> e 3,8 allo Stato)<br />

• Unità immobiliari abitative e pertinenze locate a canone concertato o concordato<br />

(L. 431 del 9/12/1998 ) definito dall’accordo territoriale fra il <strong>Comune</strong> e i soggetti<br />

appositamente in<strong>di</strong>viduati. Per il riconoscimento dell’aliquota agevolata occorre<br />

1,0<br />

8,1<br />

8,6<br />

10,6<br />

produrre idonea <strong>di</strong>chiarazione entro il 31 <strong>di</strong>cembre <strong>2012</strong>.<br />

Aliquota agevolata del 1 per mille (<strong>di</strong> totale competenza comunale):<br />

• Fabbricati Rurali ad uso Strumentale si applica ai fabbricati <strong>di</strong> cui all’articolo 9,<br />

comma 3-bis, del D.L. 557/1993, convertito, con mo<strong>di</strong>ficazioni, dalla L. n° 133/1994.<br />

Aliquota agevolata del 8,1 (<strong>di</strong> cui 4,3 al <strong>Comune</strong> e 3,8 allo Stato)<br />

• Terreni agricoli condotti da coltivatori <strong>di</strong>retti e impren<strong>di</strong>tori agricoli professionali<br />

iscritti nella previdenza agricola, purché dai medesimi condotti, con le agevolazioni<br />

previste dall’art. 4, comma 8-bis, D.L. 16/<strong>2012</strong> convertito nella Legga n. 44 del<br />

26/04/<strong>2012</strong>.<br />

Aliquota or<strong>di</strong>naria del 8,6 (<strong>di</strong> cui 4,8 al <strong>Comune</strong> e 3,8 allo Stato)<br />

• Altri fabbricati non ricompresi in quelle precedenti: in particolare per le categorie<br />

abitative da A/1 ad A/9 affittate con regolare contratto registrato a canone libero e anche<br />

alle relative pertinenze, per i fabbricati destinati alla ven<strong>di</strong>ta dalle imprese costruttrici,<br />

fino a quando permane tale destinazione.<br />

• Terreni Agricoli non ricompresi nella precedente aliquota (terreni agricoli condotti da<br />

coltivatori <strong>di</strong>retti ed impren<strong>di</strong>tori agricoli).<br />

• Si applica a tutte le unità immobiliari non specificatamente inserite in altre<br />

aliquote<br />

Aliquota del 10,6 (<strong>di</strong> cui 6,8 al <strong>Comune</strong> e 3,8 allo Stato)<br />

• Immobili abitativi e pertinenze non locati (vuoti) ed Aree Fabbricabili

$ ! <<br />

<<br />

= <<br />

><br />

7<br />

1 / +! "! ! , "! ", .'! < .,"! *; ,/"! * 5&3<br />

! 3 & 3 * (<br />

(9/0 /( 0( /% ./ < .," *1 ,/"! ;! $ "! 2 ,' '% !<br />

! " + " ' '2 = > ( ','%0 ? #! $ $ %! " . ! ! * ./,<br />

/" . '"! > ( %0 /"! ', / +! " '" , ! , .'<br />

' 3 ? ' 3 %<br />

- $ ? ' 3 = 0. + @ 3/(@3/.@3/;<br />

= 0* - @ 3/,@3/* @3/<br />

= ) +/0 @ & /<br />

= . & & /<br />

= 3/0<br />

$ + ? A $ = !<br />

$ % ! %<br />

( 0(<br />

%<br />

% B ( B<br />

(.<br />

' & ? ' & % (<br />

- $ ? ' & = 0, ! ) .<br />

- $ ? ' & = 00 %<br />

% C ! ) 0<br />

$ + ? - $ = !<br />

$ % ! %<br />

( 0(<br />

" % % %<br />

A A ? A % 0 0 ( 0(<br />

$ + ? A A = 0 .<br />

$ % ! %<br />

( 0(<br />

" % % %<br />

8 * @ 6 &= *1 ,/"! %, // +! ! ''.!<br />

',' ! " +, ! * ,-' / '-, ! ! "! (<br />

" $5 6 % 9<br />

% % %<br />

%<br />

" %<br />

%<br />

% %<br />

$ % $3$<br />

!<br />

< .! '", -.! *! - ,$ < .! 1,$ $ -, * %0 ! ! " +, 8<br />

/, ", *! A - ''! , & ! * %0 ! ! 2 ,' * + // / '"! "!<br />

'" , 5 ',+ $<br />

. " , '#, ! 2 ,' +, - /<br />

* , .' *<br />

! * & B : 3 (<br />

6 = C9 D D 35 #! > = C9 D =<br />

C ! %6/,'% ' E %, .' 6 ,+ - ,6 6 "<br />

", * , .' FFF6%, .' 6 ,+ - ,6 6 "<br />

1<br />

" # #<br />

$ %<br />

% &<br />

' () ( * *<br />

! %<br />

+ #<br />

& ' ././( 0 1 ,) 2 %<br />

% % /<br />

, 3 & & ' ././( 0 1 ,) "<br />

%<br />

/<br />

! " #! $ $ %! " & " ' ! #! $ $ %! $ (<br />

%<br />

!<br />

%<br />

, + -<br />

4 ) * % $ % %<br />

% !<br />

3 ( 0( ! " +, %,'-.! - , /. !<br />

! ! "!<br />

%,'" $ . '" %0 1! $ "! 2 ,' '% !<br />

% %<br />

" ! " 3 - .-', )<br />

/ "" $ ) * % $ *. ! " *<br />

! %%,'", % ! 45<br />

* 1 ,/"! ! ''.! 6 " * /! *, %<br />

% !<br />

3 ( 0( ! " +, %,'-.! - ,<br />

/. 1! ,'"! ","! * *. ! " + /! "<br />

4 0) % % % ,<br />

4 ) * % $ % %<br />

% ! 3<br />

( 0( ! 0 ! " +, %,'-.! - ,<br />

/. ! ! ! "!<br />

7<br />

1<br />

5<br />

$ % .'1.' %!<br />

/, .2 ,' '" , ) * % $<br />

% ! 3 ( 0(<br />

1<br />

$ % $5 6 7<br />

8 (* .<br />

,* % %! "! /"! * , .' * 8 9 : )<br />

,* % " $ .", ! -! '", * ; %,' ,* , :<br />

, ,- ! ,$<br />

,* %<br />

< .,"! , .'<br />

+ ,90(<br />

8<br />

,90,<br />

,* %<br />

< .,"! "! ",<br />

: ,90* ,90<br />

+ ,90. ,90;<br />

+ ,90) ,909