Lululemon Athletica - University of Oregon Investment Group

Lululemon Athletica - University of Oregon Investment Group

Lululemon Athletica - University of Oregon Investment Group

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Key Statistics<br />

52 Week Price Range<br />

50-Day Moving Average<br />

Estimated Beta<br />

Dividend Yield<br />

Market Capitalization<br />

3-Year Revenue CAGR<br />

Trading Statistics<br />

Diluted Shares Outstanding<br />

Average Volume (3-Month)<br />

Institutional Ownership<br />

Insider Ownership<br />

EV/EBITDA<br />

Margins and Ratios<br />

Gross Margin<br />

EBITDA Margin<br />

Net Margin<br />

Debt to Enterprise Value<br />

Leverage Ratio<br />

Covering Analysts: Ryan<br />

Swift, Ryans@uoregon.edu,<br />

Nitin Agrawal<br />

$41.18 - $77.13<br />

$XX$XX.XX<br />

$73.37<br />

1.60<br />

N/A<br />

$10.07 Billion<br />

41.47%<br />

143.56 million<br />

1.916950 million<br />

105.80%<br />

10.27%<br />

32.12<br />

59.90%<br />

32%<br />

18%<br />

0.00%<br />

0.00x<br />

Ticker: LULU<br />

Current Price: $71.93<br />

<strong>Investment</strong> Thesis<br />

1<br />

<strong>Lululemon</strong> <strong>Athletica</strong><br />

4/17/2012<br />

Consumer Goods<br />

<strong>Lululemon</strong> is a firm with a unique business model that has experienced<br />

tremendous growth over the past few years and should continue to see<br />

strong revenues for the next few years<br />

Analysts are over estimating the amount <strong>of</strong> stores to be opened in the<br />

coming years<br />

Recommended a hold due to lack <strong>of</strong> patents on innovations and, from a<br />

valuation basis, it seems as though the market has factored in a lot <strong>of</strong> the<br />

growth that the company could experience in the future<br />

$90.00<br />

$80.00<br />

$70.00<br />

$60.00<br />

$50.00<br />

$40.00<br />

$30.00<br />

$20.00<br />

$10.00<br />

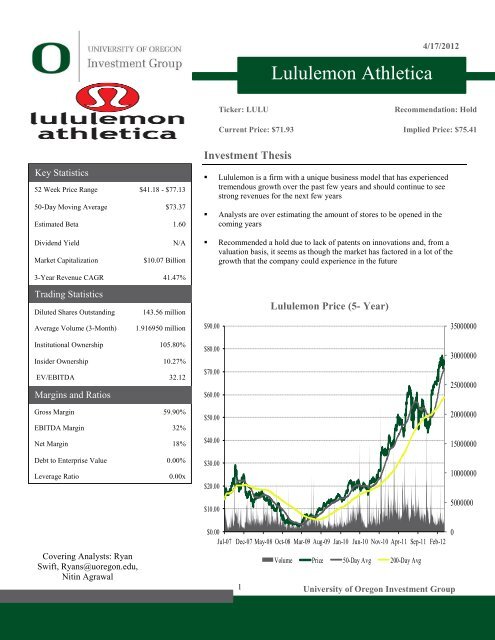

<strong>Lululemon</strong> Price (5- Year)<br />

Recommendation: Hold<br />

Implied Price: $75.41<br />

$0.00<br />

Jul-07 Dec-07 May-08 Oct-08 Mar-09 Aug-09 Jan-10 Jun-10 Nov-10 Apr-11 Sep-11 Feb-12<br />

Volume Price 50-Day Avg 200-Day Avg<br />

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

35000000<br />

30000000<br />

25000000<br />

20000000<br />

15000000<br />

10000000<br />

5000000<br />

0

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

2500<br />

2000<br />

1500<br />

1000<br />

500<br />

0<br />

Sales per<br />

square foot<br />

2008 2009 2010 2011<br />

Business Overview<br />

4/17/2012<br />

<strong>Lululemon</strong> <strong>Athletica</strong> was founded by Chip Wilson who took a commercial yoga<br />

class in Vancouver and was immediately drawn in to the concept. After<br />

spending many years in the surf, skate, and snowboarding business, Chip found<br />

that the post-yoga rush provided a similar experience to surfing and<br />

snowboarding. It only seemed natural that yoga would become a popular<br />

ideology again. At the time, yoga was performed using cotton clothing and this<br />

seemed inappropriate because it neither removed sweat adequately nor did it<br />

allow for maximum flexibility. Given his passion and expertise in technical<br />

athletic fabrics, he began a movement in yoga clothing where he relied on<br />

feedback from yoga instructors to optimize his apparel.<br />

<strong>Lululemon</strong> was founded in 1998 to meet these goals. It opened its first store in<br />

November 2000 in Kitsilano, a beach area <strong>of</strong> Vancouver BC. Beyond getting<br />

feedback from instructors on how to improve the performance <strong>of</strong> the apparel, the<br />

firm sought to act as a community hub where people can interact and share the<br />

physical and mental aspects <strong>of</strong> having a healthy lifestyle.<br />

The firm currently has three reportable segments: corporate-owned stores, direct<br />

to consumers, and other.<br />

Corporate-Owned Stores<br />

The corporate-owned stores segment includes all sales to customers through<br />

corporate-owned stores in North America and Australia. In 2011, net revenue<br />

from <strong>Lululemon</strong>’s corporate-owned stores increased from $591,031,000 to<br />

$817,318,000 representing an increase <strong>of</strong> $226.3 million or 38%. Additionally,<br />

comparable stores sales saw an increase <strong>of</strong> 20% or $114.2 million in fiscal<br />

2011when excluding the effects <strong>of</strong> foreign currency fluctuations. This segment<br />

is by far <strong>Lululemon</strong>’s largest revenue base. Going forward the segment will<br />

continue to be successful as <strong>Lululemon</strong> looks to expand its base in 2012 by<br />

opening 30 stores in the United States and 2 ivivva athletica stores in Canada.<br />

Direct To Consumers<br />

The Direct to Consumers segment involves <strong>Lululemon</strong>’s e-commerce website.<br />

Currently, only 10.62% <strong>of</strong> revenue comes from the Direct to Consumer segment<br />

while 81.66% comes from the corporate-owned stores; however, the firm<br />

believes this will become an increasingly important segment going forward.<br />

Total revenue for Fiscal 2011 was up $48,965,000 to $106,313,000 representing<br />

a growth rate <strong>of</strong> 85.38%. As the retail world shifts from brick-and-mortar stores<br />

to online channels, <strong>Lululemon</strong>’s commitment to increasing its presence in ecommerce<br />

will help the company expand its customer base and improve brand<br />

awareness in new markets, particularly in those outside <strong>of</strong> the United States.<br />

Other<br />

The Other segment <strong>of</strong> <strong>Lululemon</strong>’s business includes a wholesale channel<br />

through which <strong>Lululemon</strong> sells its products to premium yoga studios, health<br />

clubs, and fitness centers. Aside from wholesale, “Other” also includes franchise<br />

sales, wholesale accounts, sales from company-operated showrooms, and<br />

warehouse sales and outlets. Sales in this segment rose in the fiscal year <strong>of</strong> 2011<br />

from $63,325,000 to $77,208,000 representing a growth <strong>of</strong> 7.71% year over<br />

year. The wholesale channel is meant to provide greater, more convenient access<br />

UOIG 2

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

4/17/2012<br />

to <strong>Lululemon</strong>’s products for its customers and it also believes that by targeting<br />

premium outlets, it can improve the brand image.<br />

While previously franchise sales were part <strong>of</strong> the "Other" category, the company<br />

reported that it will no longer partake in the business and that it had reacquired<br />

its four remaining franchise stores during fiscal 2011. <strong>Lululemon</strong> used to enter<br />

into franchise agreements to distribute its products and to more quickly<br />

disseminate its brand name in exchange for one-time franchising fees and<br />

ongoing royalties based on gross revenue. Going forward, this segment should<br />

grow by opening new showroom locations and increasing its list <strong>of</strong> wholesale<br />

partners.<br />

Strategic Positioning<br />

Grassroots Marketing<br />

A key to <strong>Lululemon</strong>’s success in the retailing world is based on their community<br />

marketing approach. <strong>Lululemon</strong> seeks to differentiate its brand through a<br />

community-based approach <strong>of</strong> building brand awareness and customer loyalty<br />

by employing social media and in-store community boards. All <strong>of</strong> <strong>Lululemon</strong>’s<br />

stores <strong>of</strong>fer free yoga and fitness classes to local communities. The company<br />

dedicates a significant amount <strong>of</strong> time to understanding the market it is entering<br />

and then tailoring the experience appropriately. The classes are led by<br />

<strong>Lululemon</strong> ambassadors who embody the <strong>Lululemon</strong> brand by training and<br />

teaching exclusively in <strong>Lululemon</strong> gear. In exchange they receive 15% <strong>of</strong>f <strong>of</strong><br />

merchandise.<br />

Many <strong>of</strong> <strong>Lululemon</strong>’s competitors seek to promote their brands through<br />

traditional forms <strong>of</strong> advertisement such as print media, television commercials,<br />

and celebrity endorsements. This <strong>of</strong>ten increases sales in new markets more<br />

rapidly. <strong>Lululemon</strong>, however, seeks to build extreme brand loyalty through its<br />

inclusive community with hopes the overall experience is what will drive its<br />

consumer-base going forward.<br />

Vertical Retailing Strategy<br />

<strong>Lululemon</strong> is sold exclusively through the firm’s own stores, high-end lifestyle<br />

centers and yoga studios. Its stores are primarily placed in urban shopping<br />

districts and malls that cater toward the high-income, trendy crowds. Unlike<br />

larger athletic companies such as Nike that sell their products to large<br />

department stores, <strong>Lululemon</strong> has stayed true to its boutique approach which has<br />

helped them achieve higher pr<strong>of</strong>it margins and cemented its position in<br />

consumers’ minds as an elite performance company.<br />

<strong>Lululemon</strong> believes that the experience it creates with consumers is central to its<br />

strategy. Its sales associates, who are referred to as “educators”, seek to develop<br />

a personal connection with each customer and undergo 30 hours <strong>of</strong> in-house<br />

training. The vertical retailing strategy also allows stores to retain control over<br />

its operations to ensure that this experience is provided. Further, vertical<br />

retailing allows <strong>Lululemon</strong> to reduce response time and provide new products to<br />

the market within a month.<br />

UOIG 3

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Business Growth Strategies<br />

4/17/2012<br />

Although <strong>Lululemon</strong> has experienced dramatic growth in the past few years, it<br />

will look to expand further by increasing the number <strong>of</strong> domestic and<br />

international stores, creating new technologies, and increasing the range <strong>of</strong> its<br />

athletic activities and target markets.<br />

Domestic and International Expansion<br />

As <strong>of</strong> January 29 2012, <strong>Lululemon</strong> owned 155 stores in North America (47 in<br />

Canada and 108 in the United States). According to management, it expects the<br />

majority <strong>of</strong> near-term store growth to occur in the United States. Management<br />

has forecasted that North America has capacity for 350 stores. It hopes to open<br />

thirty more stores in the United States along with two Ivivva <strong>Athletica</strong> stores (a<br />

youth brand that creates technical apparel for dancers, gymnasts, ice skaters,<br />

etc.) in Canada.<br />

In order to broaden the appeal <strong>of</strong> their Products <strong>Lululemon</strong> will be branching out<br />

from yoga apparel. During Q1 2012 <strong>Lululemon</strong> will be launching swimming and<br />

surfing apparel and in the future, road biking, commuting, cold weather, spin<br />

and outerwear lines.<br />

In addition to expanding within the United States, <strong>Lululemon</strong> has also hinted at<br />

stepping up its international expansion plans. The company already operates<br />

stores in New Zealand and Australia and is expected to open approximately five<br />

stores in fiscal 2012 in these markets. <strong>Lululemon</strong> also opened a London<br />

showroom in mid-April and is expected to open a second Hong Kong showroom<br />

by the end <strong>of</strong> May. If the firm is successful in marketing its products within<br />

these countries, it will serve as a huge catalyst for growth in the future.<br />

<strong>Lululemon</strong>’s management has also expressed interest in forming joint-ventures<br />

with other Asian countries, which will further its revenues as well.<br />

Industry<br />

Overview<br />

Women’s Apparel<br />

<strong>Lululemon</strong> chiefly operates in the Women’s Apparel market, which is a large,<br />

mature, and fragmented market that is extremely sensitive to economic trends.<br />

The main activities <strong>of</strong> this industry include selling maternity wear, skirts and<br />

dresses, pants, jeans and shirts. Sports apparel, the niche that <strong>Lululemon</strong><br />

currently occupies, also falls under this category. Revenue has declined at an<br />

annual rate <strong>of</strong> 1.1% from 2006 to 2011, which has taken a toll on the pr<strong>of</strong>its <strong>of</strong><br />

retailers. In spite <strong>of</strong> the challenging business cycle, the industry expended the<br />

number <strong>of</strong> stores at an average rate <strong>of</strong> 0.9% per year in 2011. Additionally,<br />

IBISworld predicts that revenue will grow at an average annual rate <strong>of</strong> 3.4% to a<br />

total market size <strong>of</strong> $47.9 billion in 2016. While the growth in revenue will<br />

initially be slow due to macroeconomic uncertainty and high unemployment,<br />

consumer confidence and disposable income is projected to rise, which will be a<br />

major catalyst for firms operating within this industry.<br />

Firms within the Women’s Apparel market are also sensitive to changes in the<br />

price <strong>of</strong> cotton, an important raw input. In 2008, as the price <strong>of</strong> cotton and other<br />

UOIG 4

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

40000<br />

35000<br />

30000<br />

25000<br />

20000<br />

15000<br />

10000<br />

5000<br />

0<br />

Per Capita Disposable Income<br />

1981<br />

1983<br />

1985<br />

1987<br />

1989<br />

1991<br />

1993<br />

1995<br />

1997<br />

1999<br />

2001<br />

2003<br />

2005<br />

2007<br />

2009<br />

2011<br />

2013<br />

2015<br />

2017<br />

4/17/2012<br />

commodities surged, the bottom-line <strong>of</strong> many retailers took a large hit. Although<br />

producers are typically able to pass <strong>of</strong>f some <strong>of</strong> the rise in commodity costs to<br />

consumers, weakening demand and lower disposable incomes made it difficult<br />

to increase prices. As a way <strong>of</strong> coping with this environment, retailers tried to<br />

cut costs in other ways by cutting the wages <strong>of</strong> workers or laying <strong>of</strong>f employees<br />

and replacing many <strong>of</strong> their jobs with automated technology. As a result, the<br />

number <strong>of</strong> workers employed in the Women’s Apparel industry has decreased at<br />

an average annual rate <strong>of</strong> 1.7% till 2011. (Information taken from IBISworld).<br />

<strong>Lululemon</strong> is not as sensitive to these fluctuations as the majority <strong>of</strong> its raw<br />

materials are petroleum based.<br />

Gym, Health, and Fitness Clubs in the US<br />

Although <strong>Lululemon</strong> is not itself a gym, fitness centers act as a complementary<br />

industry to the company and thus positive trends in this industry act as a positive<br />

sign for <strong>Lululemon</strong>. This industry has benefited from consumer trends fighting<br />

against obesity and improving health and wellness. As a result, gym<br />

memberships have increased during the past 10 years from 36.3 million in 2002<br />

to an estimated 43.6 million in 2012. The introduction <strong>of</strong> women-oriented gyms<br />

has also increased the customer base by encouraging more women to partake in<br />

fitness.<br />

There is an element <strong>of</strong> seasonality for industry participants where the greatest<br />

growth in gym memberships occurs during the first three months <strong>of</strong> the year. On<br />

average, 30% <strong>of</strong> new members join during this period due to New Year’s<br />

resolutions. In spite <strong>of</strong> favorable consumer trends, the gym industry is not<br />

recession-pro<strong>of</strong>. During the financial crisis, consumers halted gym memberships<br />

and membership numbers began to decline for the first time in years. However,<br />

the increase in leisure time helped protect membership sales. Gym, health, and<br />

fitness clubs are also expected to benefit from the increased interest from youth<br />

and baby boomers, which will contribute to the average annual industry growth<br />

rate <strong>of</strong> 2.8% to $29 billion in 2017.<br />

Macro factors<br />

The macro factors that will be central to <strong>Lululemon</strong>’s success include per capita<br />

disposable income, time spent on leisure and sports, as well as consumer<br />

sentiment.<br />

Per Capita Disposable Income<br />

Per Capita disposable income, which measures a person’s ability to purchase<br />

goods or services, is computed by taking total income, subtracting taxes,<br />

savings, and non-tax payments, and dividing by the total population. According<br />

to IBISworld, the estimated value in 2012 is $32,953 with a forecasted value <strong>of</strong><br />

$36,845, representing a compound growth rate <strong>of</strong> 2.3% for the next five years.<br />

From 2007-2012, the compound average growth rate was 0.1%. After the<br />

financial crisis, credit tightened and unemployment increased from 4.6% to<br />

10.6% in the time period between 2007 and 2010. Wages failed to increase<br />

during the crisis and the savings rate rose from 1.4% in 2005 to 4.9% in 2009,<br />

decreasing the funds available for purchasing goods.<br />

Conditions began to stabilize in 2010 as corporate pr<strong>of</strong>its began to increase,<br />

which not only aided investor stock portfolios, but also removed pressure on<br />

businesses to depress wages. Therefore, while disposable income growth<br />

dropped by 3.2% in 2009; it grew 0.9% in 2010. Challenges still remain as a<br />

depressed housing market, high unemployment, and rising prices continue to<br />

stunt growth in disposable income. Additionally, if the United States continues<br />

UOIG 5

120<br />

100<br />

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

80<br />

60<br />

40<br />

20<br />

5.3<br />

5.25<br />

5.2<br />

5.15<br />

5.1<br />

5.05<br />

4.95<br />

0<br />

5<br />

1990<br />

1992<br />

1994<br />

Hours Spent On<br />

Leisure and Sports<br />

1996<br />

1998<br />

2000<br />

2002<br />

Consumer Sentiment Index<br />

2004<br />

2006<br />

2008<br />

2010<br />

2012<br />

2014<br />

2016<br />

4/17/2012<br />

to run a fiscal deficit, higher tax rates may be necessary in order to balance the<br />

deficit which would have a negative impact on discretionary income.<br />

Time Spent on Leisure and Sports<br />

Time spent on leisure and sports includes time spent socializing and<br />

communicating, watching television, browsing the internet, playing games,<br />

reading, playing sports, exercising as well as time spent traveling to and from<br />

these activities. The estimated value <strong>of</strong> this metric was 5.20 hours per day in<br />

2011 and it experienced a compound annual growth rate <strong>of</strong> 0.43% from 2006-<br />

2011. On average, Americans spend approximately 2 hours and 45 minutes<br />

watching TV, 45 minutes socializing, and 20 minutes on sports, exercise or<br />

recreation. These numbers are typically driven by changes in the unemployment<br />

rate, since Americans who are employed have less time for leisure than those<br />

who do not.<br />

IBISworld forecasts time spent on leisure and sports to decrease to 5.08 hours<br />

per day in 2016 representing a compound annual growth rate <strong>of</strong> -0.47%. This is<br />

driven by an uptick in employment due to a recovering economy.<br />

Because <strong>Lululemon</strong> more specifically operates in the athletic apparel industry, it<br />

is also worth looking at participation in sports, which has an estimated value <strong>of</strong><br />

18.6% in 2012 and a forecasted value <strong>of</strong> 19.2% in 2017. This represents a<br />

growth <strong>of</strong> 0.6% versus the 0.13% from 2007 to 2012. Participation in sports is<br />

also driven by unemployment and while this may reduce the participation rate<br />

for working individuals, the aging population will retire and push growth<br />

upward. There are two other favorable trends that may help <strong>Lululemon</strong>’s target<br />

demographic. The first is that the public appears to be moving away from<br />

participation in team sports and more toward individualized fitness activities,<br />

which has increased the number <strong>of</strong> gym memberships issued during the past five<br />

years. Additionally, there is a rise in alternative fitness techniques. Participation<br />

rates in activities such as yoga, tai chi, and pilates should increase due this trend.<br />

Consumer Sentiment<br />

Consumer sentiment is measured using a survey conducted by the <strong>University</strong> <strong>of</strong><br />

Michigan. In the survey, participants are asked to comment on household<br />

finances, business conditions, unemployment, inflation, among other items. The<br />

CSI took a hit with the dot com bubble and plunged further in 2008 after the<br />

collapse <strong>of</strong> Bear Stearns and Lehman Brothers. It remained low through 2009,<br />

but as housing prices stabilized and corporations regained pr<strong>of</strong>itability has<br />

slowly improved.<br />

IBIS world’s expected value in 2012 is 67.7, which represents a compound<br />

annual growth rate <strong>of</strong> -4.59% from 2007 to 2012, but it is expected to increase to<br />

70.8 in 2017 indicating a modest compound growth rate <strong>of</strong> 0.92%. Due to the<br />

magnitude <strong>of</strong> the crisis, total economic recovery will take place slowly. By 2017<br />

the CSI will be well below the 2007 average <strong>of</strong> 85.6.<br />

Competition<br />

Despite occupying a unique niche within the athletic apparel industry,<br />

<strong>Lululemon</strong> has recently gained competitors in recent years. Traditionally, big<br />

companies such as Nike, Adidas, and Under Armour have dominated the athletic<br />

apparel industry and these firms continue to have an impact on the markets<br />

today. These firms are large with market caps upward <strong>of</strong> $5 Billion and try to<br />

distinguish themselves amongst competitors by securing endorsements by high-<br />

UOIG 6

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Gross Margin 2008 2009 2010 2011<br />

Under Armour 48.9% 48.2% 49.9% 48.2%<br />

Nike 45.0% 44.6% 46.2% 45.1%<br />

Gap 36.1% 37.5% 40.3% 40.4%<br />

<strong>Lululemon</strong> 53.3% 50.7% 49.3% 55.5%<br />

4/17/2012<br />

pr<strong>of</strong>ile athletes, creative marketing campaigns, and creating innovative<br />

technologies. With the exception <strong>of</strong> a commitment to creating innovative<br />

products in apparel, these initiatives are in contrast to <strong>Lululemon</strong>s. In order to<br />

market its products, <strong>Lululemon</strong> completely shuns away from print or media<br />

advertising and instead focuses on selecting ambassadors within carefully<br />

selected markets. As a result, it’s possible for <strong>Lululemon</strong>’s competitors to<br />

achieve and maintain brand awareness and market share more quickly. These<br />

firms are more diversified in terms <strong>of</strong> the products they produce. Some <strong>of</strong> their<br />

competitors manufacture footwear and sporting goods. Furthermore, <strong>Lululemon</strong><br />

is targeted towards women and focused on yoga and running activities. It also is<br />

only beginning its international expansion. Under Armour, Nike, and Adidas are<br />

targeted towards men and women <strong>of</strong> all ages, are diversified amongst virtually<br />

all sports and, with the exception <strong>of</strong> Under Armour, are well on their way to<br />

international markets.<br />

Aside from the big name athletic apparel manufacturers, other competitors such<br />

as Gap’s Athleta brand, Lucy Activewear Inc. and Bebe Stores’ BEBE SPORT<br />

collection have emerged as competitors to <strong>Lululemon</strong>. Athleta was introduced as<br />

its own separate brand <strong>of</strong> Gap Inc. in 2009 and <strong>of</strong>fers women’s yoga clothing,<br />

swimwear, running clothing, as well as athletic apparel for fitness, golf and<br />

tennis to women at a lower price point than <strong>Lululemon</strong>. BEBE SPORT and Lucy<br />

Activewear also manufacture similar products aimed at women and are roughly<br />

priced within the same price category. Although these brands were recently<br />

introduced and do not seem to have impacted <strong>Lululemon</strong>’s revenues, as<br />

familiarity with these products gains, <strong>Lululemon</strong> could be forced to sell their<br />

products at a lower price thus reducing margins. Finally, it should be noted that<br />

<strong>Lululemon</strong> does not own any patents or exclusive intellectual property rights to<br />

the technology, fabrics, or processes that underlie its products. This makes it<br />

easier for current and future competitors to manufacture and sell products with<br />

similar performance capabilities and styling.<br />

Management and Employee Relations<br />

CEO: Christine Day<br />

Christine Day is the Chief Executive Officer and Director <strong>of</strong> <strong>Lululemon</strong><br />

<strong>Athletica</strong> Inc. She previously served as the Executive Vice President <strong>of</strong> retail<br />

operations from January 2008 through April 2008 and was appointed as Chief<br />

Operating Officer in April 2008. Prior to <strong>Lululemon</strong>, she worked at Starbucks<br />

Corporation where she was the President <strong>of</strong> the Asia Pacific <strong>Group</strong> from July<br />

2004 through February 2007 and as the Co-president for Starbucks C<strong>of</strong>fee<br />

International from July 2003 to October 2003. She earned her BA in<br />

Administrative Management from Central Washington <strong>University</strong> and is a<br />

graduate <strong>of</strong> Harvard Business School’s Advanced Management Program.<br />

According to Reuters, her total compensation is $3,472,890 and also has stock<br />

options with an estimated market value <strong>of</strong> $3,837,570.<br />

CFO: John Currie<br />

John Currie is the Chief Financial <strong>of</strong>ficer and Executive Vice President <strong>of</strong><br />

<strong>Lululemon</strong> <strong>Athletica</strong> since January 2007. Before working for <strong>Lululemon</strong>, he<br />

worked for Intrawest Corporation from 1996 to 2006 and was the CFO from<br />

2004 to 2006 as well as Senior Vice President <strong>of</strong> Financing and Taxation from<br />

1997 to 2004. He is a chartered accountant and received his Bachelor <strong>of</strong><br />

Commerce degree from the <strong>University</strong> <strong>of</strong> British Columbia. According to<br />

Reuters, his basic compensation was $1,105,580 and has stock options with an<br />

estimated market value <strong>of</strong> $7,819,560.<br />

UOIG 7

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Recent News<br />

4/17/2012<br />

April 17th, 2012 – <strong>Lululemon</strong> Ducks the Radar and Lands in<br />

London (CNBC.com)<br />

This article covers <strong>Lululemon</strong>’s ventures into London and how it is expected to<br />

open a showroom there. Other key facts covered are that the company ranks<br />

fourth in sales per square foot in retail ($2004 behind Apple, Tiffany, and<br />

Coach) and achieved same-store sales growth <strong>of</strong> 20% the previous year.<br />

Furthermore, it also discusses <strong>Lululemon</strong>’s grassroots initiatives as opposed to<br />

traditional print advertising and how with strong sales in the United States,<br />

international expansion could be the icing on the cake for the company.<br />

2/2/2012 <strong>Lululemon</strong> CEO: Wilson Knew it was Time to Go<br />

(Forbes.com)<br />

This article discusses the resignation <strong>of</strong> <strong>Lululemon</strong>’s CEO from the company<br />

two years ago. Chief Product <strong>of</strong>ficer Sheree Waterson has taken over as<br />

Wilson’s replacement. Wilson, will be best known for his controversial<br />

marketing campaign where he placed the phrase, “who is John Galt” on<br />

<strong>Lululemon</strong>’s tote bags, which were not well-received products by consumers,<br />

but created a buzz that Wilson really enjoyed. Since his departure, <strong>Lululemon</strong><br />

has not seemed to struggle and instead the author argued that the former CEO<br />

mostly realized that he was not CEO-material and that the company would be<br />

left in better hands upon his resignation.<br />

Catalysts<br />

Upside<br />

Increased interest and demand for alternative fitness activities such as<br />

yoga<br />

Uptick in the economy will allow for more disposable income and thus<br />

more money to spend on <strong>Lululemon</strong>’s products<br />

New initiatives for men will broaden product <strong>of</strong>ferings and improve<br />

brand awareness if successful<br />

Potential for international expansion<br />

Downside<br />

L<strong>of</strong>ty growth expectations could lead to down turns in stock prices if it<br />

does not meet expectations<br />

Potential for substitute products at a lower cost is an especially big risk<br />

because they do not own patents on their products<br />

Comparable Analysis<br />

When evaluating comparable firms, the chief metrics used in selection were<br />

revenue growth rates as well as margins. <strong>Lululemon</strong> has high forecasted growth<br />

rates and is earning strong margins relative to its peers. This is what sets the firm<br />

apart from its competitors. Choosing a firm with lower growth rates and or low<br />

margins would artificially depress the multiple and thus makes the comparables<br />

analysis less accurate in determining a fair price for <strong>Lululemon</strong>. In addition to<br />

these metrics, the overall business model was into consideration when choosing<br />

UOIG 8

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

4/17/2012<br />

companies to use for the comparables. Of the companies chosen (Under<br />

Armour, Deckers, Tiffany and Company, and Coach Inc.), Under Armour and<br />

Deckers were given a slightly higher weighting than the other two due to the fact<br />

that the companies were more similar to <strong>Lululemon</strong> in terms <strong>of</strong> actual revenues,<br />

EBIT, EBITDA, and also having similar growth rates while being in the same<br />

general industry as <strong>Lululemon</strong>. Tiffany is mostly into the retailing <strong>of</strong> jewelry,<br />

which is not the same industry as <strong>Lululemon</strong>, and Coach is simply bigger than<br />

all <strong>of</strong> the comparables, which means that it is not as comparable in terms <strong>of</strong><br />

market cap or market size in general.<br />

Under Armour – 40% Weight<br />

“Under Armour, Inc. engages in the design, development, marketing, and<br />

distribution <strong>of</strong> apparel, footwear, and accessories for men, women, and youth<br />

worldwide. The company <strong>of</strong>fers its apparel in three fit types: compression,<br />

fitted, and loose that are designed to be worn in hot, cold, and changing<br />

temperatures. Its footwear products include football, baseball, lacrosse, s<strong>of</strong>tball<br />

and soccer cleats, as well as slides, performance training footwear, running<br />

footwear, basketball footwear, and hunting boots for athletes. The company’s<br />

accessories comprise baseball batting, football, golf, and running gloves; and<br />

licensees <strong>of</strong>fer socks, team uniforms, baby and kids’ apparel, eyewear, and<br />

custom-molded mouth guards, as well as hats and bags. Under Armour, Inc.<br />

sells its products primarily under the UA and UNDER ARMOUR brands<br />

through wholesale channels, which include independent and specialty retailers,<br />

institutional athletic departments, leagues and teams, national and regional<br />

sporting goods chains, and department store chains; independent distributors;<br />

and directly to consumers through its own specialty and factory house stores,<br />

and Website. The company was founded in 1996 and is headquartered in<br />

Baltimore, Maryland.”<br />

Deckers Outdoor Corporation – 20% Weight<br />

“Deckers Outdoor Corporation engages in the design, manufacture, and<br />

marketing <strong>of</strong> footwear and accessories for outdoor activities and casual lifestyle<br />

use for men, women, and children. The company <strong>of</strong>fers luxury footwear,<br />

handbags, apparel, and cold weather accessories under the UGG brand name;<br />

open and closed-toe outdoor lifestyle footwear, multi-sport shoes, light hiking<br />

shoes, amphibious footwear, and rugged outdoor travel shoes under the Teva<br />

brand name; action sport footwear under the Sanuk brand name; high-end casual<br />

footwear for men and women under the TSUBO brand name; outdoor<br />

performance and lifestyle footwear under the Ahnu brand name; and work<br />

footwear under the MOZO brand name. The company sells its products<br />

primarily to specialty retailers, department stores, outdoor retailers, sporting<br />

goods retailers, shoe stores, and online retailers. Deckers Outdoor Corporation<br />

also sells its products directly to end-user consumers through its Websites, call<br />

centers, retail concept stores, and retail outlet stores, as well as through retailers<br />

in the United States. In addition, the company distributes its products through<br />

independent distributors and retailers in Europe, Canada, Australia, Asia, and<br />

Latin America. It has a joint venture with Stella International Holdings Limited<br />

for the opening <strong>of</strong> retail stores and wholesale distribution for the UGG brand in<br />

China. Deckers Outdoor Corporation was founded in 1973 and is headquartered<br />

in Goleta, California. “<br />

UOIG 9

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Tiffany & Co. – 20% Weight<br />

4/17/2012<br />

“Tiffany & Co., through its subsidiaries, engages in the design, manufacture,<br />

and retail <strong>of</strong> fine jewelry worldwide. Its jewelry products include fine and<br />

solitaire jewelry; diamond engagement rings and wedding bands to brides and<br />

grooms; and non-gemstone, sterling silver, gold, and platinum jewelry. The<br />

company also provides timepieces, sterling silver goods, china, crystal,<br />

stationery, fragrances, personal accessories, and leather goods. Tiffany & Co.<br />

sells its products through retail sales, Internet and catalog sales, business-tobusiness<br />

sales, and wholesale distribution primarily in the Americas, the Asia-<br />

Pacific, Japan, and Europe. The company also sells its products through its<br />

stores, as well as through department store in Japan. As <strong>of</strong> January 31, 2012, it<br />

operated 247 stores, including 102 in the Americas, 58 in Asia-Pacific, 55 in<br />

Japan, and 32 in Europe. The company was founded in 1837 and is<br />

headquartered in New York, New York.”<br />

Coach Inc. – 20% Weight<br />

“Coach, Inc. designs and markets accessories and gifts for women and men in<br />

the United States and internationally. It primarily <strong>of</strong>fers handbags, women’s and<br />

men’s bag, accessories, business cases, footwear, wearables, jewelry, sunwear,<br />

travel bags, watches, and fragrance products. The company’s accessories,<br />

include money pieces, wristlets, cosmetic cases, wallets, card cases, time<br />

management and electronic accessories, key rings, charms, and women’s and<br />

men’s belts; business cases, such as computer bags, messenger-style bags, and<br />

totes; wearables comprise jackets, sweaters, gloves, hats, and scarves; jewelry<br />

consisting <strong>of</strong> bangle bracelets, necklaces, rings, and earrings; and luggage and<br />

related accessories, such as travel kits and valet trays. It provides women’s<br />

fragrance collections, including eau de perfume spray, eau de toilette spray,<br />

purse spray, body lotion, and body splashes. The company operates stores in<br />

North America, Japan, Hong Kong, Macau, and mainland China, as well as sells<br />

through the Internet and the Coach catalog. It also sells its products to wholesale<br />

customers and distributors in approximately 20 countries. As <strong>of</strong> July 2, 2011, it<br />

had 345 retail and 143 factory leased stores located in North America; 169<br />

Coach-operated department store shop-in-shops, retail stores, and factory stores<br />

in Japan; and 66 Coach-operated department store shop-in-shops, retail stores,<br />

and factory stores in Hong Kong, Macau, and mainland China. The company<br />

was founded in 1941 and is headquartered in New York, New York.” (Company<br />

descriptions taken from Yahoo Finance)<br />

Other Considerations<br />

Aside from the aforementioned firms, other companies that were considered for<br />

the comparables analysis included Nike, Whole Foods Markets, Saks, Bebe, and<br />

Liz Claiborne. Nike was considered because it has also begun targeting women<br />

through its Nike Women campaign and has created similar products (Dri-Fit<br />

Training Capris) while also operating in the same industry as <strong>Lululemon</strong>.<br />

However, because the company is not growing as rapidly and has lower<br />

margins, it is trading at a lower multiple and would not be appropriate to include<br />

in the analysis.<br />

Whole Foods Markets was considered because it can be considered a play on the<br />

alternative lifestyle market, and thus could be an indicator <strong>of</strong> the potential<br />

growth within this segment <strong>of</strong> the population that <strong>Lululemon</strong> is trying to target.<br />

UOIG 10

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Company EV/EBITDA<br />

Under Armour 25.71<br />

TIFFANY 10.39<br />

DECKERS 30.90<br />

COACH 13.95<br />

<strong>Lululemon</strong> 26.14<br />

Average 21.42<br />

4/17/2012<br />

However, because it operates in the retail <strong>of</strong> food, it’s EBIT and EBITDA<br />

margins as well as its growth rates were not comparable.<br />

Finally, Saks, Liz Clairborne, and Bebe were considered because they are<br />

higher-end brands that are <strong>of</strong>ten frequented by women, and, in the case <strong>of</strong> Bebe,<br />

an indirect competitor to <strong>Lululemon</strong> through particular product lines. However,<br />

these firms simply did not have the requisite growth and margins needed to be<br />

truly comparable to <strong>Lululemon</strong>.<br />

Discounted Cash Flow Analysis<br />

COGS<br />

Cost <strong>of</strong> goods sold was also projected using a “cost per square foot” metric and<br />

was initially increased in the first two years, but brought back down slightly due<br />

to economies <strong>of</strong> scale in the long run.<br />

Beta<br />

For computing the betas, the Vasicek 5 year monthly and 1 year weekly betas<br />

were calculated along with the Hamada 5 year monthly and 1 year weekly betas.<br />

The Vasicek was used in order to adjust for variances within the industry, which<br />

are important in an industry like retail where companies can have a wide variety<br />

<strong>of</strong> expected returns and volatility levels. The Hamada beta was used to compare<br />

<strong>Lululemon</strong>s beta to the equity beta <strong>of</strong> its competitors as it adjusts for capital<br />

structure.<br />

Revenue Model<br />

In order to construct the revenue model, the total number <strong>of</strong> stores, was<br />

estimated using historical data and management guidance. From there, the total<br />

square footage can also be computed once the average store size was figured<br />

out. For the projection years, it was assumed that the store size would not<br />

increase because <strong>Lululemon</strong>’s small store size is actually vital to its commitment<br />

to providing an overall shopping experience for its consumers. Sales per square<br />

foot were assumed to increase due to managements comments that existing<br />

stores have excess capacity for future growth.<br />

Exit Multiple<br />

For an exit multiple we used EV/EBITDA as it is most commonly used. In order<br />

to calculate the exit multiple we took an average <strong>of</strong> the trailing twelve months<br />

EV/EBITDA for <strong>Lululemon</strong> and the companies used in the comparables<br />

analysis. We obtained a multiple <strong>of</strong> 21.42x EBITDA.<br />

Recommendation<br />

<strong>Lululemon</strong> is growing rapidly and has a unique business model that will help it<br />

see solid increases in revenues for the next few years. However, based on our<br />

discounted cash flow and comparables analysis there does not appear to be a<br />

significant undervaluation. Therefore, LULU is a HOLD for all portfolios.<br />

UOIG 11

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Appendix 1 – Comparables Analysis<br />

4/17/2012<br />

Comparables Analysis Analysis Ticker UA TIF DECK COH<br />

($ in millions) LULU Under Armour TIFFANY DECKERS COACH<br />

Stock Characteristics Max Min Weight Avg. Median 40.00% 20.00% 20.00% 20.00%<br />

Current Price $96.21 $67.56 $80.03 $70.10 $71.95 $96.21 $68.26 $67.56 $71.93<br />

50 Day Moving Average $95.82 $66.05 $80.52 $72.46 $73.40 $95.82 $68.69 $66.05 $76.22<br />

200 Day Moving Average $86.66 $60.24 $77.89 $75.80 $60.24 $83.25 $68.34 $86.66 $67.96<br />

Beta $1.85 $0.77 $1.46 $1.58 1.60 1.50 1.85 0.77 1.66<br />

Size<br />

Short-Term Debt 173.80 0.00 37.67 3.84 0.00 6.88 173.80 0.00 0.80<br />

Long-Term Debt 538.40 0.00 185.76 103.40 0.00 183.61 538.40 0.00 23.20<br />

Cash and Cash Equivalent 1,085.60 175.38 428.43 352.90 409.44 175.38 442.20 263.61 1,085.60<br />

Non-Controlling Interest 5.49 0.00 1.10 0.00 4.81 0.00 0.00 5.49 0.00<br />

Preferred Stock 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00<br />

Diluted Basic Shares 296.09 52.81 136.77 141.06 113.31 52.81 128.42 153.69 296.09<br />

Market Capitalization 21,048.91 5,070.39 10,052.94 9,537.51 8,119.21 5,070.39 8,691.48 10,383.54 21,048.91<br />

Enterprise Value 19,987.31 5,085.49 9,849.04 9,543.45 7,714.58 5,085.49 8,961.48 10,125.42 19,987.31<br />

Pr<strong>of</strong>itability Margins<br />

Gross Margin 72.3% 48.4% 55.5% 54.2% 56.9% 48.4% 59.0% 49.3% 72.3%<br />

EBIT Margin 30.9% 10.9% 18.6% 20.1% 28.7% 10.9% 19.4% 20.7% 30.9%<br />

EBITDA Margin 33.7% 13.4% 21.3% 23.1% 31.7% 13.4% 23.5% 22.8% 33.7%<br />

Net Margin 21.2% 6.6% 12.2% 13.4% 18.5% 6.6% 12.1% 14.7% 21.2%<br />

Credit Metrics<br />

Interest Expense $48.57 $0.00 $11.30 $2.05 $0.00 $3.84 $48.57 $0.25 $0.00<br />

Debt/EV 0.08 0.00 0.03 0.02 0.00 0.04 0.08 0.00 0.00<br />

Leverage Ratio 0.97 0.00 0.56 0.42 0.00 0.97 0.83 0.00 0.02<br />

Interest Coverage Ratio 1262.28 0.00 276.49 34.44 0 51.29 17.59 1262.28 0<br />

Operating Results<br />

Revenue $4,481.39 $1,000.84 $2,489.40 $2,557.81 $1,000.84 $1,472.68 $3,642.94 $1,377.28 $4,481.39<br />

Gross Pr<strong>of</strong>it 3,242.06 569.27 1,499.58 1,432.00 569.27 712.84 2,151.15 679.00 3,242.06<br />

EBIT 1,382.76 160.70 539.59 496.88 286.96 160.70 708.43 285.33 1,382.76<br />

EBITDA 1,509.47 197.00 614.43 584.33 317.22 197.00 854.36 314.31 1,509.47<br />

Net Income 950.97 96.92 357.17 320.52 184.96 96.92 439.19 201.86 950.97<br />

Valuation<br />

EV/Revenue 7.71x 2.46x 4.24x 3.96x 7.71x 3.45x 2.46x 7.35x 4.46x<br />

EV/Gross Pr<strong>of</strong>it 14.91x 4.17x 7.90x 6.65x 13.55x 7.13x 4.17x 14.91x 6.17x<br />

EV/EBIT 35.49x 12.65x 25.18x 23.05x 26.88x 31.65x 12.65x 35.49x 14.45x<br />

EV/EBITDA 32.21x 10.49x 21.51x 19.53x 24.32x 25.81x 10.49x 32.21x 13.24x<br />

EV/Net Income 52.47x 20.40x 39.31x 35.59x 41.71x 52.47x 20.40x 50.16x 21.02x<br />

Multiple Weight<br />

EV/Revenue 40.98 20.00%<br />

EV/Gross Pr<strong>of</strong>it 43.27 0.00%<br />

EV/EBIT 67.33 40.00%<br />

EV/EBITDA 63.80 40.00%<br />

EV/Net Income 67.73 0.00%<br />

Price Target 60.65<br />

Current Price 72.1<br />

Overvalued 18.88%<br />

UOIG 12

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Appendix 2 – Discounted Cash Flows Analysis<br />

Discounted Cash Flow Analysis<br />

4/17/2012<br />

($ in millions) 2007A 2008A 2009A 2010A 2011A 2012E 2013E 2014E 2015E 2016E<br />

Total Revenue 269.94 353.49 452.90 711.70 1000.84 1370.91 1699.20 2081.37 2334.69 2546.93<br />

% YoY Growth - 30.95% 28.12% 57.14% 40.63% 36.98% 23.95% 22.49% 12.17% 9.09%<br />

Cost <strong>of</strong> Goods Sold 116.72 158.60 208.98 292.14 401.31 433.20 599.85 760.60 851.47 923.27<br />

% Revenue 43.24% 44.87% 46.14% 41.05% 40.10% 31.60% 35.30% 36.54% 36.47% 36.25%<br />

Gross Pr<strong>of</strong>it $153.22 $194.89 $243.92 $419.56 $599.53 $937.71 $1,099.35 $1,320.77 $1,483.22 $1,623.67<br />

Gross Margin 56.76% 55.13% 53.86% 58.95% 59.90% 68.40% 64.70% 63.46% 63.53% 63.75%<br />

Selling General and Administrative Expense 93.38 118.10 136.16 212.78 282.31 383.85 475.78 582.78 653.71 713.14<br />

% Revenue 34.59% 33.41% 30.06% 29.90% 28.21% 28.00% 28.00% 28.00% 28.00% 28.00%<br />

Depreciation and Amortization 8.29 15.82 20.83 24.61 30.26 43.67 57.22 70.90 82.70 83.00<br />

% Revenue 3.07% 4.48% 4.60% 3.46% 3.02% 3.19% 3.37% 3.41% 3.54% 3.26%<br />

Provision for Impairment and Lease Exit Costs 0.00 4.41 0.38 1.72 0.00 7.18 8.90 10.90 12.23 13.34<br />

% Revenue 0.00% 1.25% 0.08% 0.24% 0.52% 0.52% 0.52% 0.52% 0.52% 0.52%<br />

Earnings Before Interest & Taxes $51.55 $56.56 $86.55 $180.441 $286.96 $503.00 $557.45 $656.18 $734.57 $814.18<br />

% Revenue 19.10% 16.00% 19.11% 25.35% 28.67% 36.69% 32.81% 31.53% 31.46% 31.97%<br />

Other Income (expense) 1.03 0.82 0.16 2.89 2.50 3.58 5.10 6.66 7.94 8.66<br />

% Revenue .38% .23% .04% .41% .25% .26% .30% .32% .34% .34%<br />

Earnings Before Taxes 52.58 57.39 86.71 183.33 289.46 499.42 552.35 649.52 726.64 805.52<br />

% Revenue 19.48% 16.23% 19.15% 25.76% 28.92% 36.43% 32.51% 31.21% 31.12% 31.63%<br />

Less Taxes (Benefits) 20.46 16.88 28.43 61.08 104.49 182.29 198.85 233.83 261.59 289.99<br />

Tax Rate 38.92% 29.42% 32.79% 33.32% 36.10% 36.50% 36.00% 36.00% 36.00% 36.00%<br />

Net Income From Continuing Operations 32.12 40.50 58.28 122.25 184.96 317.13 353.51 415.69 465.05 515.54<br />

% Revenue 11.90% 11.46% 12.87% 17.18% 18.48% 23.13% 20.80% 19.97% 19.92% 20.24%<br />

Net Income Attributable To Non-Controlling Interest 0.00 0.00 0.00 0.35 0.90 1.37 1.70 2.08 2.33 2.55<br />

% Revenue 0.00% 0.00% 0.00% .05% .09% .10% .10% .10% .10% .10%<br />

Net Loss from Discontued Operations ($1.27) ($1.14) -<br />

% Revenue (.47%) (.32%) 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%<br />

Net Income $30.84 $39.36 $58.28 $121.897 $184.06 $317.13 $353.51 $415.69 $465.05 $515.54<br />

Net Margin 11.43% 11.14% 12.87% 17.13% 18.39% 23.13% 20.80% 19.97% 19.92% 20.24%<br />

Add Back: Depreciation and Amortization 8.29 15.82 20.83 24.61 30.26 43.67 57.22 70.90 82.70 83.00<br />

Add Back: Interest Expense*(1-Tax Rate) 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00<br />

Operating Cash Flow $39.13 $55.19 $79.11 $146.51 $214.32 $360.80 $410.73 $486.60 $547.75 $598.54<br />

% Revenue 14.50% 15.61% 17.47% 20.59% 21.41% 26.32% 24.17% 23.38% 23.46% 23.50%<br />

Current Assets 99.82 121.10 220.94 395.69 535.45 679.57 778.63 768.46 761.70 809.40<br />

% Revenue 36.98% 34.26% 48.78% 55.60% 53.50% 49.57% 45.82% 36.92% 32.63% 31.78%<br />

Current Liabilities 36.14 45.34 58.68 85.36 103.44 154.50 193.54 239.77 271.88 296.97<br />

% Revenue 13.39% 12.83% 12.96% 11.99% 10.34% 11.27% 11.39% 11.52% 11.65% 11.66%<br />

Net Working Capital $63.68 $75.76 $162.26 $310.32 $432.01 $525.07 $585.09 $528.69 $489.82 $512.43<br />

% Revenue 23.59% 21.43% 35.83% 43.60% 43.16% 38.30% 34.43% 25.40% 20.98% 20.12%<br />

Change in Working Capital 12.09 86.50 148.06 121.69 93.06 60.02 -56.41 -38.86 22.60<br />

Capital Expenditures 30.01 42.80 15.50 43.90 122.31 74.00 78.00 91.20 92.07 98.58<br />

% Revenue 11.12% 12.11% 3.42% 6.17% 12.22% 5.40% 4.59% 4.38% 3.94% 3.87%<br />

Acquisitions 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00<br />

% Revenue 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%<br />

Unlevered Free Cash Flow 9.12 0.30 (22.88) (45.45) (29.68) 193.74 272.71 451.80 494.54 477.35<br />

Discounted Free Cash Flow 170.75 211.81 309.26 298.33 253.78<br />

EBITDA 59.8 72.4 107.4 205.1 317.2 546.7 614.7 727.1 817.3 897.2<br />

EBITDA Margin 22.17% 20.48% 23.71% 28.81% 31.70% 39.88% 36.17% 34.93% 35.01% 35.23%<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

UOIG 13<br />

-

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Appendix 3 – Revenue Model<br />

4/17/2012<br />

Total Stores 2007A 2008A 2009A 2010A 2011A 2012E 2013E 2014E 2015E 2016E<br />

Canada 37 42 44 44 47 55 63 72 79 85<br />

Change in # 5 2 0 3 8 8 9 7 6<br />

% Growth 13.51% 4.76% 0.00% 6.82% 17.02% 14.55% 14.29% 9.72% 7.59%<br />

United States 30 61 66 78 108 138 168 198 223 243<br />

Change in # 31 5 12 30 30 30 30 25 20<br />

% Growth 103.33% 8.20% 18.18% 38.46% 27.78% 21.74% 17.86% 12.63% 8.97%<br />

Australia 0 0 0 11 18 21 23 24 25 26<br />

Change in # 0 0 11 7 3 2 1 1 1<br />

% Growth - - - 63.64% 16.67% 9.52% 4.35% 4.17% 4.00%<br />

New Zealand 0 0 0 0 1 2 3 5 6 6<br />

Change in # 0 0 0 1 2 1 2 1 0<br />

% Growth - - - - 100.00% 50.00% 66.67% 20.00% 0.00%<br />

Japan 4 0 0 0 0 0 0 0 0 0<br />

Change in # -4 0 0 0 0 0 0 0 0<br />

% Growth -100.00% - - - - - - - -<br />

Hong Kong 0 0 0 0 0 1 2 3 3 3<br />

Change in # 0.00% 0.00% 0.00% 0.00% 100.00% 100.00% 100.00% 0.00% 0.00%<br />

% Growth - - - - - 100.00% 50.00% 0.00% 0.00%<br />

Other International 0 0 0 0 0 0 1 2 5 9<br />

Change in # 0.00 0.00 0.00 0.00 0.00 1.00 1.00 3.00 4.00<br />

% Growth - - - - - - - - -<br />

Total 71 103 110 133 174 217 260 304 341 372<br />

Estimating Total Revenue 2007A 2008A 2009A 2010A 2011A 2012E 2013E 2014E 2015E 2016E<br />

Sales Per Square Foot 1700 1450 1318 1726 2004 2030 2100 2200 2200 2200<br />

% Growth -14.71% -9.10% 30.96% 16.11% 1.30% 3.45% 4.76% 0.00% 0.00%<br />

Total Square Footage 161,595.88 243,784.83 343,625.19 412,342.99 541,504.41 675,324.46 809,144.52 946,076.67 1,061,224.15 1,157,697.48<br />

Average Store Size 2276.00 2366.84 3123.87 3100.32 3112.09 3112.09 3112.09 3112.09 3112.09 3112.09<br />

Total Revenue 274,713,000.00 353,488,000.00 452,898,000.00 711,704,000.00 1,000,839,000.00 1,370,908,658.02 1,699,203,485.23 2,081,368,664.70 2,334,693,140.33 2,546,934,456.00<br />

UOIG 14

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Appendix 4 – Working Capital Model<br />

Working Capital Model<br />

4/17/2012<br />

($ in millions) 2007A 2008A 2009A 2010A 2011A 2012E 2013E 2014E 2015E 2016E<br />

Total Revenue $274.71 $353.49 $452.90 $711.70 $1,000.84 $1,370.91 $1,699.20 $2,081.37 $2,334.69 $2,546.93<br />

Current Assets<br />

Cash & Cash Equivalents 52.54 56.80 159.57 316.29 409.44 494.50 528.00 462.50 418.50 435.00<br />

% <strong>of</strong> Revenue 19.13% 16.07% 35.23% 44.44% 40.91% 36.07% 31.07% 22.22% 17.93% 17.08%<br />

Cash per store opened 1.64 8.11 6.94 7.71 9.52 11.50 12.00 12.50 13.50 14.50<br />

Accounts Receivable 4.30 4.03 8.24 9.12 5.20 9.60 16.99 20.81 23.35 25.47<br />

% <strong>of</strong> Revenue 1.57% 1.14% 1.82% 1.28% 0.52% 0.70% 1.00% 1.00% 1.00% 1.00%<br />

Inventory 37.93 52.05 44.07 57.47 104.10 150.80 203.90 249.76 280.16 305.63<br />

Days Inventory Outstanding 118.61 120.12 76.97 71.80 94.94 127.06 124.07 119.86 120.43 120.83<br />

% <strong>of</strong> Revenue 13.81% 14.72% 9.73% 8.07% 10.40% 11.00% 12.00% 12.00% 12.00% 12.00%<br />

Prepaid Expenses 2.52 4.11 4.53 6.41 8.36 13.71 16.99 20.81 23.35 25.47<br />

% <strong>of</strong> Revenue 0.92% 1.16% 1.00% 0.90% 0.83% 1.00% 1.00% 1.00% 1.00% 1.00%<br />

Assets <strong>of</strong> Discontinued Operations 2.52 4.11 4.53 6.41 8.36 10.97 12.74 14.57 16.34 17.83<br />

% <strong>of</strong> Revenue 0.92% 1.16% 1.00% 0.90% 0.83% 0.80% 0.75% 0.70% 0.70% 0.70%<br />

Total Current Assets 99.816775 121.099 220.939 395.687 535.45 679.5726688 778.6325141 768.4611937 761.6998916 809.399365<br />

% <strong>of</strong> Revenue<br />

Long Term Assets<br />

36.33% 34.26% 48.78% 55.60% 53.50% 49.57% 45.82% 36.92% 32.63% 31.78%<br />

Net PP&E Beginning 18.18 43.60 61.66 61.59 70.95 163.01 280.68 301.45 321.75 331.12<br />

Capital Expenditures 30.013 41.045 15.497 30.357 122.311 74 78 91.2 92.07 98.58<br />

Cap Ex per Store $ 0.42 $ 0.40 $ 0.14 $ 0.23 $ 0.36 $ 0.20 $ 0.30 $ 0.30 $ 0.27 $ 0.27<br />

Depreciation and Amortization 8.29 15.82 20.83 24.61 30.26 43.67 57.22 70.90 82.70 83.00<br />

Net PP&E Ending 43.6 61.7 61.6 71.0 163.01 280.68 301.45 321.75 331.12 346.70<br />

Total Current Assets & Net PP&E 143.42 182.76 282.53 466.64 698.46 960.25 1080.09 1090.21 1092.82 1156.10<br />

% <strong>of</strong> Revenue<br />

Current Liabilities<br />

15.87% 17.44% 13.60% 9.97% 16.29% 20.47% 17.74% 15.46% 14.18% 13.61%<br />

Accounts Payable 5.40 5.27 11.03 6.66 14.54 20.56 25.83 32.26 36.77 40.50<br />

% <strong>of</strong> Revenue 1.96% 1.49% 2.43% 0.94% 1.45% 1.50% 1.52% 1.55% 1.58% 1.59%<br />

Accrued Charges 15.23 27.97 27.83 42.14 57.41 $78.14 $98.55 $122.80 $140.08 $152.82<br />

% <strong>of</strong> Revenue 5.55% 7.91% 6.15% 5.92% 5.74% 5.70% 5.80% 5.90% 6.00% 6.00%<br />

Income Taxes Payable 5.72 2.13 7.74 18.40 8.72 21.52 26.68 32.68 36.65 39.99<br />

% <strong>of</strong> Revenue 2.08% 0.60% 1.71% 2.59% 0.87% 1.57% 1.57% 1.57% 1.57% 1.57%<br />

Unredeemed Gift Card Liability 8.11 9.28 11.70 18.17 22.77 34.27 42.48 52.03 58.37 63.67<br />

% <strong>of</strong> Revenue 2.95% 2.62% 2.58% 2.55% 2.28% 2.50% 2.50% 2.50% 2.50% 2.50%<br />

Other Current Liabilities 0.78 0.69 0.38 -<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

% <strong>of</strong> Revenue 0.28% 0.20% 0.08% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%<br />

Liabilities <strong>of</strong> Discontinued Operations 0.90 -<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

% <strong>of</strong> Revenue 0.33% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%<br />

Total Current Liabilities 36.14 45.34 58.68 85.36 103.44 154.50 193.54 239.77 271.88 296.97<br />

% <strong>of</strong> Revenue 13.16% 12.83% 12.96% 11.99% 10.34% 11.27% 11.39% 11.52% 11.65% 11.66%<br />

UOIG 15

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Appendix 5 – Discounted Cash Flows Analysis Assumptions<br />

Discounted Free Cash Flow Assumptions<br />

Tax Rate 36.50%<br />

Risk Free Rate 2.00%<br />

Beta 1.64<br />

Market Risk Premium 7.00%<br />

% Equity 100.00%<br />

% Debt 0.00%<br />

Cost <strong>of</strong> Debt 0.00%<br />

CAPM 13.47%<br />

WACC 13.47%<br />

Terminal Value 2,497<br />

PV <strong>of</strong> Terminal Value 1,327<br />

Total Debt 0<br />

Cash & Cash Equivalents 409<br />

Market Capitalization 8,152<br />

Fully Diluted Shares 113<br />

Vasicek 5 Year Monthly 2.13<br />

Vasicek 1 Year Weekly 1.54<br />

Hamada 5 Year Monthly 1.29<br />

Hamada 1 Year Weekly 1.60<br />

LULU Beta 1.6383676<br />

Beta SD Weighting<br />

25.00%<br />

25.00%<br />

25.00%<br />

25.00%<br />

Exit Multiple Calculation<br />

Terminal Year EBITDA 897.18<br />

Exit Multiple 21.22<br />

Terminal Value 19034.47<br />

Discount Period 5<br />

Discount Factor 1.880953<br />

Discounted Terminal Value 10119.59<br />

Present Value <strong>of</strong> FCF 1243.93<br />

Enterprise Value 7714.58<br />

Outstanding Shares 113.31<br />

Implied Price 79.06355<br />

Current Price 72.03<br />

Implied Price Weight<br />

Comps 60.19 30%<br />

DCF 81.93 70%<br />

Target Price 75.41<br />

Current Price 72.03<br />

Undervalued 4.70%<br />

4/17/2012<br />

Company EV/EBITDA<br />

Under Armour 25.81<br />

TIFFANY 10.49<br />

DECKERS 32.21<br />

COACH 13.24<br />

<strong>Lululemon</strong> 24.32<br />

Average 21.22<br />

UOIG 16

<strong>University</strong> <strong>of</strong> <strong>Oregon</strong> <strong>Investment</strong> <strong>Group</strong><br />

Appendix 6 –COGS Model<br />

Appendix 7 – Sources<br />

SEC Filings<br />

Company Investor Relations page<br />

Company presentations<br />

Earnings call<br />

IBIS World<br />

Factset<br />

4/17/2012<br />

Estimating COGS 2007A 2008A 2009A 2010A 2011A 2012E 2013E 2014E 2015E 2016E<br />

Cost Per Square Foot 722.32 650.57 608.16 708.50 800.00 888.24 940.00 900.00 870.00 850.00<br />

Total COGS 116,723,746 158,598,050 208,980,000 292,143,000 433,203,526 599,851,507 760,595,846 851,468,999 923,265,015 984,042,858<br />

UOIG 17