Answers - ACCA

Answers - ACCA

Answers - ACCA

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

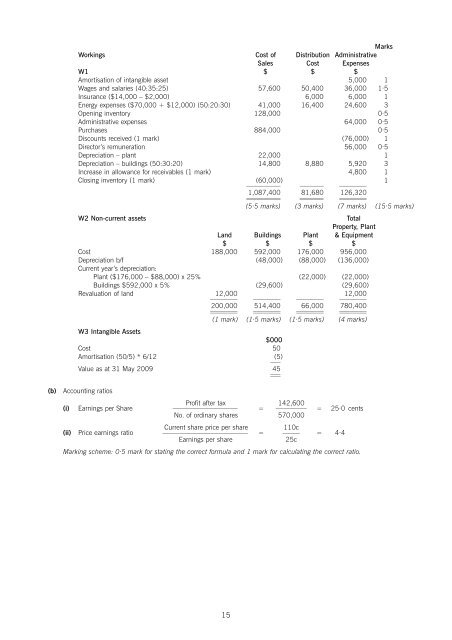

Workings Cost of Distribution<br />

Marks<br />

Administrative<br />

Sales Cost Expenses<br />

W1 $ $ $<br />

Amortisation of intangible asset 5,000 1<br />

Wages and salaries (40:35:25) 57,600 50,400 36,000 1·5<br />

Insurance ($14,000 – $2,000) 6,000 6,000 1<br />

Energy expenses ($70,000 + $12,000) (50:20:30) 41,000 16,400 24,600 3<br />

Opening inventory 128,000 0·5<br />

Administrative expenses 64,000 0·5<br />

Purchases 884,000 0·5<br />

Discounts received (1 mark) (76,000) 1<br />

Director’s remuneration 56,000 0·5<br />

Depreciation – plant 22,000 1<br />

Depreciation – buildings (50:30:20) 14,800 8,880 5,920 3<br />

Increase in allowance for receivables (1 mark) 4,800 1<br />

Closing inventory (1 mark) (60,000)<br />

–––––––––– ––––––– ––––––––<br />

1<br />

1,087,400<br />

––––––––––<br />

81,680<br />

–––––––<br />

126,320<br />

––––––––<br />

(5·5 marks) (3 marks) (7 marks) (15·5 marks)<br />

W2 Non-current assets Total<br />

Land Buildings Plant<br />

Property, Plant<br />

& Equipment<br />

$ $ $ $<br />

Cost 188,000 592,000 176,000 956,000<br />

Depreciation b/f<br />

Current year’s depreciation:<br />

(48,000) (88,000) (136,000)<br />

Plant ($176,000 – $88,000) x 25% (22,000) (22,000)<br />

Buildings $592,000 x 5% (29,600) (29,600)<br />

Revaluation of land 12,000<br />

–––––––– –––––––– ––––––––<br />

12,000<br />

––––––––<br />

200,000<br />

––––––––<br />

514,400<br />

––––––––<br />

66,000<br />

––––––––<br />

780,400<br />

––––––––<br />

(1 mark) (1·5 marks) (1·5 marks) (4 marks)<br />

W3 Intangible Assets<br />

$000<br />

Cost 50<br />

Amortisation (50/5) * 6/12 (5)<br />

–––<br />

Value as at 31 May 2009 45<br />

–––<br />

(b) Accounting ratios<br />

(i) Earnings per Share<br />

Profit after tax<br />

––––––––––––––––––– =<br />

142,600<br />

–––––––––<br />

No. of ordinary shares 570,000<br />

= 25·0 cents<br />

(ii) Price earnings ratio<br />

Current share price per share<br />

––––––––––––––––––––––––– =<br />

110c<br />

––––– = 4·4<br />

Earnings per share 25c<br />

Marking scheme: 0·5 mark for stating the correct formula and 1 mark for calculating the correct ratio.<br />

15