Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Handy<br />

WEEKLY 39.2011<br />

Scrap market at a turning point,<br />

what are the drivers?<br />

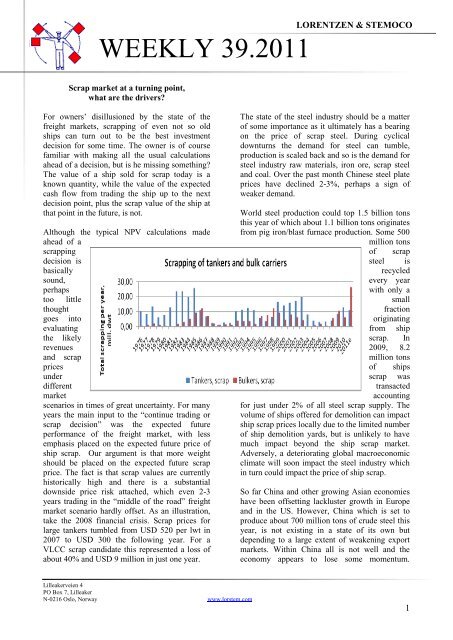

For owners’ disillusioned by the state of the<br />

freight markets, scrapping of even not so old<br />

ships can turn out to be the best investment<br />

decision for some time. The owner is of course<br />

familiar with making all the usual calculations<br />

ahead of a decision, but is he missing something?<br />

The value of a ship sold for scrap today is a<br />

known quantity, while the value of the expected<br />

cash flow from trading the ship up to the next<br />

decision point, plus the scrap value of the ship at<br />

that point in the future, is not.<br />

Although the typical NPV calculations made<br />

ahead of a<br />

scrapping<br />

decision is<br />

basically<br />

sound,<br />

perhaps<br />

too little<br />

thought<br />

goes into<br />

evaluating<br />

the likely<br />

revenues<br />

and scrap<br />

prices<br />

under<br />

different<br />

market<br />

scenarios in times of great uncertainty. For many<br />

years the main input to the “continue trading or<br />

scrap decision” was the expected future<br />

performance of the freight market, with less<br />

emphasis placed on the expected future price of<br />

ship scrap. Our argument is that more weight<br />

should be placed on the expected future scrap<br />

price. The fact is that scrap values are currently<br />

historically high and there is a substantial<br />

downside price risk attached, which even 2-3<br />

years trading in the “middle of the road” freight<br />

market scenario hardly offset. As an illustration,<br />

take the 2008 financial crisis. Scrap prices for<br />

large tankers tumbled from USD 520 per lwt in<br />

2007 to USD 300 the following year. For a<br />

VLCC scrap candidate this represented a loss of<br />

about 40% and USD 9 million in just one year.<br />

Lilleakerveien 4<br />

PO Box 7, Lilleaker<br />

N-0216 Oslo, Norway www.lorstem.com<br />

LORENTZEN & STEMOCO<br />

The state of the steel industry should be a matter<br />

of some importance as it ultimately has a bearing<br />

on the price of scrap steel. During cyclical<br />

downturns the demand for steel can tumble,<br />

production is scaled back and so is the demand for<br />

steel industry raw materials, iron ore, scrap steel<br />

and coal. Over the past month Chinese steel plate<br />

prices have declined 2-3%, perhaps a sign of<br />

weaker demand.<br />

World steel production could top 1.5 billion tons<br />

this year of which about 1.1 billion tons originates<br />

from pig iron/blast furnace production. Some 500<br />

million tons<br />

of scrap<br />

steel is<br />

recycled<br />

every year<br />

with only a<br />

small<br />

fraction<br />

originating<br />

from ship<br />

scrap. In<br />

2009, 8.2<br />

million tons<br />

of ships<br />

scrap was<br />

transacted<br />

accounting<br />

for just under 2% of all steel scrap supply. The<br />

volume of ships offered for demolition can impact<br />

ship scrap prices locally due to the limited number<br />

of ship demolition yards, but is unlikely to have<br />

much impact beyond the ship scrap market.<br />

Adversely, a deteriorating global macroeconomic<br />

climate will soon impact the steel industry which<br />

in turn could impact the price of ship scrap.<br />

So far China and other growing Asian economies<br />

have been offsetting lackluster growth in Europe<br />

and in the US. However, China which is set to<br />

produce about 700 million tons of crude steel this<br />

year, is not existing in a state of its own but<br />

depending to a large extent of weakening export<br />

markets. Within China all is not well and the<br />

economy appears to lose some momentum.<br />

1

WEEKLY 39.2011<br />

Recent headlines, pointing to 65 millions of<br />

unsold apartments and potential wave of<br />

corporate bankrupt resulting from unsound<br />

lending practices and too rapid expansion, give<br />

reasons for concern. A deterioration of the<br />

Chinese economy could curb steel production<br />

and reduce demand for iron ore and scrap steel<br />

with price falls to follow also impacting ship<br />

demolition prices. A large share of the Chinese<br />

economic expansion has been in building new<br />

production capacity and infrastructure, sectors<br />

which are highly steel intensive. A shift to higher<br />

consumer spending, which has already been<br />

called for some time by China’s main trading<br />

partners, would almost certainly be less steel<br />

intensive.<br />

Conclusion: Scrapping activity is up sharply this<br />

year, led by a surge in dry bulk ship demolition.<br />

With a massive tonnage overhang of large<br />

tankers and a much younger age profile<br />

compared to the dry bulk fleet, drastic measures<br />

are called for. With trading conditions looking<br />

distinctly difficult for the next 2-3 years and with<br />

secondhand prices already approaching current<br />

scrap prices an early move to scrap even 15-16<br />

year old ships can well turn out to be the best<br />

decision for the tanker owner.<br />

Have a continued nice week!<br />

Knut Stangebye Olsen<br />

LORENTZEN & STEMOCO<br />

2

WEEKLY 39.2011<br />

Last Week<br />

(USD/day)<br />

This week<br />

(USD/day)<br />

SMX (max. 15 yr. old<br />

craned) grabber<br />

T/A r/v 16000 16000<br />

Pac. r/v 14000 14000<br />

Cont./F.East 22250 22500<br />

F.East/Europe 9000 9000<br />

12 mos T/C 52,000 dwt 14500 14500<br />

SUPRAMAX PACIFIC<br />

It was a steady week for the short period market and<br />

not very much exiting happening at the beginning of<br />

the week. Mid week there was more activity as many<br />

of the Chinese and Koreans needed to cover their<br />

position prior the forth coming holidays. When Friday<br />

came it seemed that many had covered and the day<br />

went by quietly.<br />

Fixtures<br />

'Marylisa V' 2003 52174 dwt dely PG end September<br />

trip redel China $16700 daily - Grand Win Shipping<br />

'Jiu Hua Hai' 2008 53393 dwt dely dop Beira 28/29<br />

September 4/6 months trading redel Atlantic $14500<br />

daily - cnr -<br />

'Agonistis' 2010 58000 dwt dely CJK spot trip via<br />

Australia redel China $14000 daily - Klaveness<br />

'Mykali' 2011 56200 dwt dely Hondagua 2/4 October<br />

trip via Australia redel China $17500 daily -<br />

Klaveness<br />

'Flag Alexandros' 2010 56180 dwt dely Lanshan<br />

29/30 September trip redel WC India intention steels<br />

$14500 daily - cnr<br />

'Jin Yuan' 2007 55400 dwt dely Beihai 29/30<br />

September trip via Se Asia redel China intention<br />

nickel ore $18500 daily - cnr<br />

'Navios Celestial' 2009 58063 dwt dely S Korea end<br />

Sept/ely Oct trip via Nopac redel Singapore-Japan<br />

approx $14750 daily - cnr<br />

'Desert Condor' 2011 56000 dwt dely Japan early<br />

October 2 laden legs redel Singapore-Japan 1st leg<br />

intention Q'land-Indonesia sugar approx $15000 daily<br />

- STX Pan Ocean - <br />

'Efi Theo' 1997 45423 dwt dely Beihai spot trip via<br />

N.Australia redel Singapore-Japan $13500 daily -<br />

Pacbasin<br />

LORENTZEN & STEMOCO<br />

'Christine Star' 2011 56854 dwt dely Lianyungang<br />

spot trip via SE Asia redel China intention nickel ore<br />

$16500 daily - cnr<br />

'Grebe Arrow' 1997 55671 dwt dely Jeddah 5/10<br />

October trip via Red Sea redel India $17800 daily -<br />

Bulkmarine<br />

'Prabhu Mihika' 2005 55557 dwt dely Jintang spot trip<br />

via Nopac redel SE Asia approx $14000 daily - Fednav<br />

'Kastro' 2008 58780 dwt dely Qingdao spot 3/5<br />

months trading redel worldwide $14600 daily - WBC -<br />

<br />

SUPRAMAX ATLANTIC<br />

With a quiet pacific market due to Golden Week. The<br />

Atlantic is staying firm in all areas for the Supras.<br />

Still showing strong levels in the USG, with a lack of<br />

tonnage and more and more cargoes hitting the market<br />

it seems that it will stay strong in the week to come.<br />

All in all strong number all over the line, but the next<br />

weeks will show if it will hold up.<br />

The markets are still showing some activity and<br />

interest for shorter period.<br />

Fixtures<br />

'Star Manx' 2009 58193 dwt dely ECUK spot trip<br />

redel Singapore-Japan $23500 daily - cnr<br />

'Kibali' 2011 58000 dwt dely S.Brazil early October<br />

trip redel Singapore-Japan approx $22000 daily +<br />

approx $375000 bb - cnr<br />

'Banos A' 2010 57000 dwt dely N Brazil early<br />

October trip redel China $21000 daily + approx<br />

$400000 bb - cnr<br />

'United Stars' 1995 43991 dwt dely S Brazil spot trip<br />

redel Singapore-Japan $20000 daily + $400000 bb -<br />

Dreyfus<br />

'Elegant Sky' 2007 53549 dwt dely aps USGulf spot<br />

trip redel Continent approx $27500 daily - Dreyfus<br />

3

WEEKLY 39.2011<br />

'Yangtze Pioneer' 2011 32688 dwt dely Antonina<br />

early October about 3/5 months trading redel<br />

worldwide approx $17000 daily - cnr<br />

'Mateo Tres' 2010 57000 dwt dely aps N Brazil<br />

early/mid October trip via PG redel PMO $24500<br />

daily + $450000 bb - cnr<br />

'Leo Advance' 2007 56600 dwt dely aps USGulf spot<br />

trip redel Morocco approx $30500 daily - Oldendorff<br />

'Navios Kypros' 2003 55222 dwt dely USGulf spot<br />

trip redel Med $26400 daily - U-Sea Bulk<br />

'Jaeger' 2004 52483 dwt dely USGulf early October<br />

trip redel Peru $28000 daily - Pacbasin<br />

'Tigris' 2003 52454 dwt dely W.Africa spot trip via N<br />

Brazil and AG redel PMO approx $25000 daily -<br />

Pacbasin - <br />

'Glory Sanye' 1994 45216 dwt dely EC Florida spot<br />

trip via USGulf redel W Africa $22000 daily - ABC<br />

'Tubarao' 2007 53350 dwt dely USGulf mid October<br />

trip redel Singapore-Japan intention grain approx<br />

$31000 daily - Noble<br />

'Kang Fu' 2002 51069 dwt dely USGulf 15/20<br />

October trip redel China intention pet coke approx<br />

$35500 daily - STX Pan Ocean<br />

'Elena Topic' 1999 49928 dwt dely Continent spot<br />

trip redel E Med intention scrap $21000 daily - cnr<br />

'Glory Sanye' 1994 45216 dwt dely EC Florida spot<br />

trip via USGulf redel W.Africa $23000 daily -<br />

ABCML - <br />

'Tektoneos' 1993 43620 dwt dely Continent spot trip<br />

redel Turkey intention scrap $19000 daily - Nordic<br />

Bulk Carriers<br />

LORENTZEN & STEMOCO<br />

'POS Island' 2006 55710 dwt dely W.Africa 8/11<br />

October 3/5 months trading redel worldwide $19750<br />

daily - Copenship<br />

PANAMAX<br />

Modern Panamax<br />

Last Week<br />

(USD/day)<br />

Last Week<br />

(USD/day)<br />

Trans Atlantic r/v 14 100 14 900<br />

Pacific r/v 11 300 11 750<br />

Trip Atl./F.East 22 650 23 900<br />

Trip F.East/Atl. 4 470 4 650<br />

12 mos. T/C 14 500 14 500<br />

CAPESIZE<br />

Capesize<br />

Last Week<br />

(USD/mt)<br />

Tubarao/Beilun-Baoshan 27.8 26.8<br />

Richards Bay/Rotterdam 13.0 12.6<br />

Tubarao/Rotterdam 14.6 14.0<br />

Bolivar/Rotterdam 15.7 15.0<br />

Dampier/Beilun-Baoshan 11.7 11.1<br />

This Week<br />

(USD/mt)<br />

Del.Cont.-Med. TCT F.East 48 400 46 200<br />

Del. Gib-Hbg T/A r/v 33 860 29 900<br />

Del.China-Jpn TCT Cont.-Med. 6 460 5 690<br />

F.East r/v 26 800 24 560<br />

One year T/C 170,000 dwt 19 250 19 000<br />

4

WEEKLY 39.2011<br />

INTERMEDIATE/FLEXI (10/25,000 DWT) NWE<br />

This week we have seen an increase in intermediate<br />

activity all over North West Europe, and also on the<br />

sub 10kt parcels. Although cargoes ex Grangemouth<br />

are being reported at USD 145,000 lumpsum this<br />

week, cargoes ex WC Sweden have strengthened to<br />

USD 140 - 145,000 lumpsum. Naphta cargoes ex<br />

Baltic are holding firm with more fixtures reported at<br />

USD 235,000 lumpsum as last week. We are still<br />

expecting to see an increase in movements ex Baltic as<br />

we move into October. As seen in the below graph,<br />

the index for September increased with lower bunker<br />

costs and slightly higher realized rates on average,<br />

compared to the previous month.<br />

Outlook: Firmer<br />

CLEAN<br />

Clean outlook: Firmer<br />

Handy/MR<br />

Last<br />

Week<br />

This<br />

Week<br />

(WS) (WS)<br />

Average<br />

earnings<br />

This week<br />

(USD/day)<br />

37.000 CONT/USAC R/V 161 178 11 700<br />

25.000 CROSS UKC R/V 181 215 14 650<br />

27.500 MED/UKCM R/V 153 160 8 800<br />

28.500 CARIBS/USAC R/V 130 133 850<br />

33.000 MEG/JAPAN R/V 150 145 4 200<br />

30.000 SPORE/JAPAN R/V 155 153 5 800<br />

LR1/LR2<br />

70.000 CONT/USAC R/V 115 110 7 200<br />

55.000 MEG/JAPAN R/V 133 125 7 550<br />

LORENTZEN & STEMOCO<br />

VLCC trades ended last week on a year to date low<br />

with earnings remaining below opex for the majority of<br />

fixtures. Other sectors were mostly unchanged with<br />

relatively little activity and long position lists showing<br />

spot availability of vessels.<br />

Looking ahead, US inventory draws of both crude and<br />

products in the week ended October 5 th , gives some<br />

support for the weeks ahead. In addition the VLCC<br />

availability in the MEG has declined compared to last<br />

week, however the oversupply lingers on. In the MED,<br />

weather delays in the Turkish Straights are causing<br />

inefficiencies which could continue to support Owners’<br />

bargaining position in the week to come. Both Afra’s<br />

and Suezmax vessels have seen greatly improved rates<br />

as charterers are looking to secure tonnage in<br />

anticipation of further delays.<br />

Product tanker trades in the Caribbean are maintaining<br />

their strength on the back of continued inquiries for<br />

products in Latin America.<br />

DIRTY<br />

Crude outlook: Steady<br />

VLCC<br />

MT 290.000<br />

MEG/Continent<br />

MT 250.000<br />

MEG/Japan<br />

Suezmax<br />

Last<br />

Week<br />

This<br />

Week<br />

(WS) (WS)<br />

Average<br />

earnings<br />

This week<br />

(USD/day)<br />

34 32 -10 000<br />

45 41 -8 000<br />

MT 130.000 WAF/USG 75 73 9 700<br />

MT 130.000 Sidi<br />

Kerir/Lavera<br />

Aframax<br />

88 80 10 150<br />

80.000 N.Sea/USAC 105 105 11 750<br />

80.000 N.Sea/UK-Cont 97 98 4 450<br />

80.000 MEG/Singapore 100 100 7 950<br />

70.000 Caribs/USAC-G 90 90 3 800<br />

Panamax<br />

50.000 Caribs/USG 124 124 8 900<br />

5

WEEKLY 39.2011<br />

For further information on Gas, request a copy of our<br />

Weekly Gas Report on e-mail: lorgas@lorstem.no<br />

BULK CARRIER<br />

LORENTZEN & STEMOCO<br />

TYPE NAME DWT BUILT YARD GIR PRICE (m$) BYERS COMMENTS<br />

CAPE<br />

CAPE<br />

CAPE<br />

UNIVERSAL<br />

Hull no 124<br />

UNIVERSAL<br />

Hull no 125<br />

UNIVERSAL<br />

Hull no 149<br />

205,000 2011<br />

205,000 2011/12<br />

205,000 2011/12<br />

CAPE HENG SHAN 174,145 2007<br />

CAPE<br />

CAPE<br />

WAKABA<br />

171,978 1996<br />

CAPE C. OASIS 165,693 1996<br />

PAMX GH POWER 76,421 2002<br />

PMAX<br />

PMAX<br />

SMAX<br />

SMAX<br />

SMAX<br />

SMAX<br />

BUNGA SAGA<br />

9<br />

TRIDENT<br />

ENDEAVOR<br />

SUNNY<br />

GLOBE<br />

ATLANTIC<br />

ADVENTURE<br />

OCEAN<br />

SPIRIT<br />

SANKO<br />

SUMMIT<br />

73,127 1999<br />

68,789 1990<br />

Universal<br />

Shipbuilding<br />

Universal<br />

Shipbuilding<br />

Universal<br />

Shipbuilding<br />

SWS -Shanghai<br />

Waigaoqiao<br />

Kawasaki HI -<br />

Sakaide<br />

CSBS - China<br />

Shipbuilding<br />

Tsuneishi Shbldg -<br />

Tadotsu<br />

Hyundai Heavy<br />

Industries<br />

Hyundai Heavy<br />

Industries<br />

55,715 2005 Oshima Shipbuilding<br />

55,709 2006 Oshima Shipbuilding<br />

55,614 2006<br />

NACKS - Nantong<br />

COSCO KHI<br />

50,655 1998 Namura Shipbuilding<br />

SMAX FREE LADY 50,246 2003 Mitsui Tamano<br />

HMAX DE SHAN 37,489 1984 Mitsubishi Nagasaki<br />

HANSY SUNRISE 86 23,987 1981 Imabari Shipbuilding<br />

C 4 x<br />

30<br />

C 4 x<br />

30<br />

C 4 x<br />

31<br />

C 4 x<br />

30<br />

C 4 x<br />

31<br />

C 3 x<br />

30<br />

C 2 x<br />

15<br />

C 4 x<br />

25<br />

$56.25<br />

$56.50<br />

$56.50<br />

$36.00<br />

$18.20<br />

Clients of<br />

China Steel<br />

Express<br />

Clients of Hsin<br />

Chien Marine<br />

Chinese<br />

interests<br />

Clients of<br />

Cyprus<br />

Maritime<br />

$17.00 KAMCO<br />

Dely Dec 2011<br />

Enbloc deal<br />

under<br />

negotiations. Dely<br />

2011/2012<br />

$19.50 Greek under negos<br />

$16.75 Greek<br />

$10.50<br />

$25.00<br />

$28.80<br />

$25.00<br />

$16.50<br />

European<br />

interests<br />

Undisclosed<br />

Interests<br />

Undisclosed<br />

Interests<br />

Undisclosed<br />

Interests<br />

Undisclosed<br />

Interests<br />

$21.90 Greek<br />

$5.20<br />

$2.90<br />

Taiwanese<br />

interests<br />

Chinese<br />

interests<br />

ss due 3/2015<br />

open hatch. 8/8<br />

ho/ha<br />

6

WEEKLY 39.2011<br />

TANKER<br />

LORENTZEN & STEMOCO<br />

TYPE NAME DWT BUILT YARD IMO PRICE (m$) BYERS COMMENTS<br />

VLCC TAKASE 314,250 1999 Mitsui Chiba Ichihara $27.50<br />

MR PAFOS 41,354 1993<br />

STST SPRING URSA 16,026 1997<br />

STST<br />

SICHEM<br />

PEACE<br />

8,807 2005<br />

Minami-Nippon<br />

Usuki<br />

Shin Kurushima<br />

Akitsu<br />

Usuki Shipyard Co<br />

Ltd<br />

IMO<br />

II/III<br />

IMO<br />

II/III<br />

IMO<br />

II<br />

-<br />

$8.70<br />

$10.00<br />

Clients of<br />

Polembros<br />

Undisclosed<br />

Interests<br />

Undisclosed<br />

Interests<br />

South East<br />

Asian<br />

interests<br />

undisclosed price<br />

Stainless steel<br />

tanks<br />

Stainless steel<br />

tanks<br />

7