The Valuation of Basket Credit Derivatives: A Copula Function ...

The Valuation of Basket Credit Derivatives: A Copula Function ...

The Valuation of Basket Credit Derivatives: A Copula Function ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

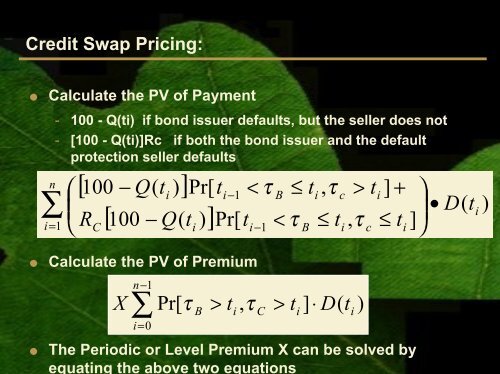

<strong>Credit</strong> Swap Pricing:<br />

● Calculate the PV <strong>of</strong> Payment<br />

- 100 - Q(ti) if bond issuer defaults, but the seller does not<br />

- [100 - Q(ti)]Rc if both the bond issuer and the default<br />

protection seller defaults<br />

[ 100 − Q(<br />

t ] i ) Pr[<br />

R [ 100 − Q(<br />

t ) ]<br />

n ⎛<br />

ti<br />

1 < B ≤<br />

∑<br />

− τ<br />

⎜<br />

= 1 ⎝ C<br />

i Pr[ ti<br />

−1<br />

< τ<br />

● Calculate the PV <strong>of</strong> Premium<br />

● <strong>The</strong> Periodic or Level Premium X can be solved by<br />

equating the above two equations<br />

, τ<br />

, τ<br />

i B i c i<br />

∑ − n 1<br />

i=<br />

0<br />

X Pr[ τ<br />

> t , τ<br />

B<br />

i<br />

C<br />

><br />

t<br />

i<br />

t<br />

i<br />

≤<br />

t<br />

c<br />

] ⋅ D(<br />

t<br />

i<br />

><br />

)<br />

t<br />

] + ⎞<br />

•<br />

t ] ⎟<br />

≤ ⎠<br />

i<br />

D(<br />

t<br />

i<br />

)