On portfolio delegation with moral hazard under translation ... - HIM

On portfolio delegation with moral hazard under translation ... - HIM

On portfolio delegation with moral hazard under translation ... - HIM

SHOW LESS

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

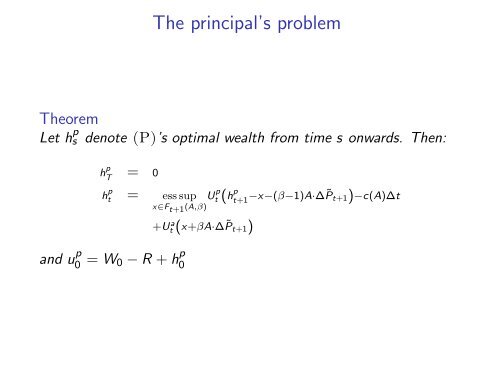

The principal’s problem<br />

Theorem<br />

Let h p s denote (P)’s optimal wealth from time s onwards. Then:<br />

h p T<br />

= 0<br />

h p t = ess sup U p t (h p t+1 −x−(β−1)A·∆˜P t+1)−c(A)∆t<br />

x∈F t+1 (A,β)<br />

+U a t (x+βA·∆˜P t+1)<br />

and u p 0 = W 0 − R + h p 0