On portfolio delegation with moral hazard under translation ... - HIM

On portfolio delegation with moral hazard under translation ... - HIM

On portfolio delegation with moral hazard under translation ... - HIM

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

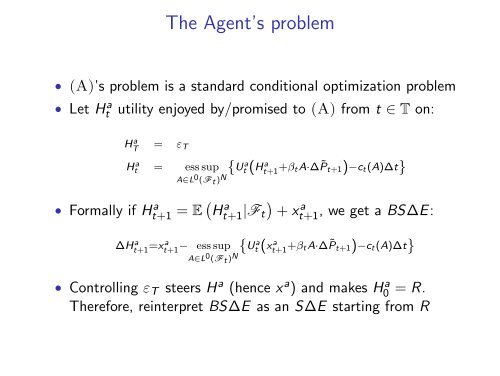

The Agent’s problem<br />

• (A)’s problem is a standard conditional optimization problem<br />

• Let H a t<br />

utility enjoyed by/promised to (A) from t ∈ T on:<br />

H a T = ε T<br />

H a t = ess sup<br />

A∈L 0 (Ft ) N {U a t (H a t+1 +βtA·∆˜P t+1)−c t(A)∆t}<br />

• Formally if H a t+1 = E ( H a t+1 |F t)<br />

+ x<br />

a<br />

t+1 , we get a BS∆E:<br />

∆Ht+1 a =xa t+1 − ess sup {U a<br />

A∈L 0 (Ft ) N t (xt+1 a +βtA·∆˜P t+1)−c t(A)∆t}<br />

• Controlling ε T steers H a (hence x a ) and makes H a 0 = R.<br />

Therefore, reinterpret BS∆E as an S∆E starting from R