September 2010 - Association for Corporate Growth

September 2010 - Association for Corporate Growth

September 2010 - Association for Corporate Growth

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Cover Story<br />

“<br />

<br />

<br />

<br />

”<br />

that had been put off <strong>for</strong> decades.<br />

The resuscitation of General Motors is unlike any<br />

turnaround or restructuring ever witnessed. From the<br />

scale of the problem to the Senate hearings and subsequent<br />

government funding, it can be hard <strong>for</strong> any<br />

executive to relate.<br />

SSG Capital Advisors’ J. Scott Victor, founding<br />

partner and managing director at<br />

the firm, says in his view, “There is<br />

no correlation, whatsoever” between<br />

GM’s restructuring and what most<br />

distressed middle-market companies<br />

may encounter.<br />

But as GM’s per<strong>for</strong>mance starts to<br />

reflect the labors of the turnaround,<br />

others believe important lessons can<br />

be pulled from the ef<strong>for</strong>t. AlixPartners’<br />

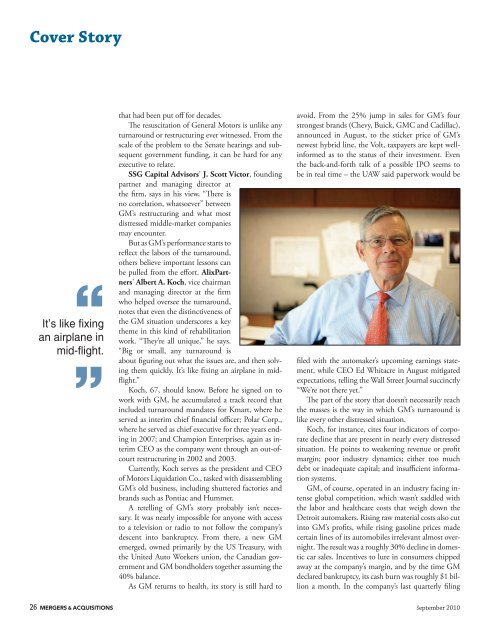

Albert A. Koch, vice chairman<br />

and managing director at the firm<br />

who helped oversee the turnaround,<br />

notes that even the distinctiveness of<br />

the GM situation underscores a key<br />

theme in this kind of rehabilitation<br />

work. “They’re all unique,” he says.<br />

“Big or small, any turnaround is<br />

about figuring out what the issues are, and then solving<br />

them quickly. It’s like fixing an airplane in midflight.”<br />

Koch, 67, should know. Be<strong>for</strong>e he signed on to<br />

work with GM, he accumulated a track record that<br />

included turnaround mandates <strong>for</strong> Kmart, where he<br />

served as interim chief financial officer; Polar Corp.,<br />

where he served as chief executive <strong>for</strong> three years ending<br />

in 2007; and Champion Enterprises, again as interim<br />

CEO as the company went through an out-ofcourt<br />

restructuring in 2002 and 2003.<br />

Currently, Koch serves as the president and CEO<br />

of Motors Liquidation Co., tasked with disassembling<br />

GM’s old business, including shuttered factories and<br />

brands such as Pontiac and Hummer.<br />

A retelling of GM’s story probably isn’t necessary.<br />

It was nearly impossible <strong>for</strong> anyone with access<br />

to a television or radio to not follow the company’s<br />

descent into bankruptcy. From there, a new GM<br />

emerged, owned primarily by the US Treasury, with<br />

the United Auto Workers union, the Canadian government<br />

and GM bondholders together assuming the<br />

40% balance.<br />

As GM returns to health, its story is still hard to<br />

avoid. From the 25% jump in sales <strong>for</strong> GM’s four<br />

strongest brands (Chevy, Buick, GMC and Cadillac),<br />

announced in August, to the sticker price of GM’s<br />

newest hybrid line, the Volt, taxpayers are kept wellin<strong>for</strong>med<br />

as to the status of their investment. Even<br />

the back-and-<strong>for</strong>th talk of a possible IPO seems to<br />

be in real time – the UAW said paperwork would be<br />

filed with the automaker’s upcoming earnings statement,<br />

while CEO Ed Whitacre in August mitigated<br />

expectations, telling the Wall Street Journal succinctly<br />

“We’re not there yet.”<br />

The part of the story that doesn’t necessarily reach<br />

the masses is the way in which GM’s turnaround is<br />

like every other distressed situation.<br />

Koch, <strong>for</strong> instance, cites four indicators of corporate<br />

decline that are present in nearly every distressed<br />

situation. He points to weakening revenue or profit<br />

margin; poor industry dynamics; either too much<br />

debt or inadequate capital; and insufficient in<strong>for</strong>mation<br />

systems.<br />

GM, of course, operated in an industry facing intense<br />

global competition, which wasn’t saddled with<br />

the labor and healthcare costs that weigh down the<br />

Detroit automakers. Rising raw material costs also cut<br />

into GM’s profits, while rising gasoline prices made<br />

certain lines of its automobiles irrelevant almost overnight.<br />

The result was a roughly 30% decline in domestic<br />

car sales. Incentives to lure in consumers chipped<br />

away at the company’s margin, and by the time GM<br />

declared bankruptcy, its cash burn was roughly $1 billion<br />

a month. In the company’s last quarterly filing<br />

26 MERGERS & ACQUISITIONS <strong>September</strong> <strong>2010</strong>