comprehensive annual financial report - Orlando International Airport

comprehensive annual financial report - Orlando International Airport

comprehensive annual financial report - Orlando International Airport

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

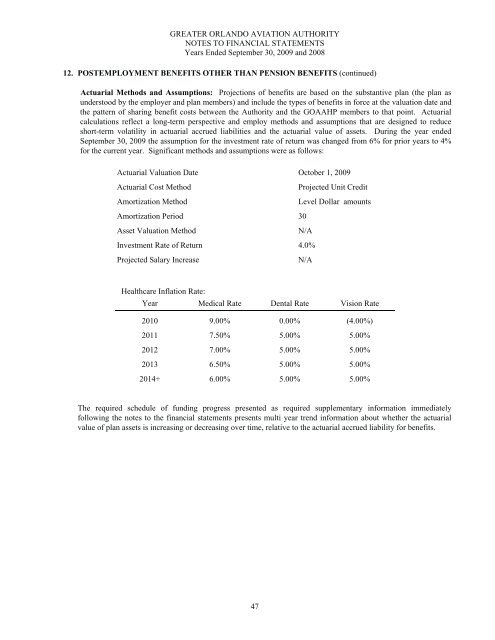

GREATER ORLANDO AVIATION AUTHORITY<br />

NOTES TO FINANCIAL STATEMENTS<br />

Years Ended September 30, 2009 and 2008<br />

12. POSTEMPLOYMENT BENEFITS OTHER THAN PENSION BENEFITS (continued)<br />

Actuarial Methods and Assumptions: Projections of benefits are based on the substantive plan (the plan as<br />

understood by the employer and plan members) and include the types of benefits in force at the valuation date and<br />

the pattern of sharing benefit costs between the Authority and the GOAAHP members to that point. Actuarial<br />

calculations reflect a long-term perspective and employ methods and assumptions that are designed to reduce<br />

short-term volatility in actuarial accrued liabilities and the actuarial value of assets. During the year ended<br />

September 30, 2009 the assumption for the investment rate of return was changed from 6% for prior years to 4%<br />

for the current year. Significant methods and assumptions were as follows:<br />

Actuarial Valuation Date October 1, 2009<br />

Actuarial Cost Method<br />

Amortization Method<br />

Projected Unit Credit<br />

Level Dollar amounts<br />

Amortization Period 30<br />

Asset Valuation Method<br />

N/A<br />

Investment Rate of Return 4.0%<br />

Projected Salary Increase<br />

N/A<br />

Healthcare Inflation Rate:<br />

Year Medical Rate Dental Rate Vision Rate<br />

2010 9.00% 0.00% (4.00%)<br />

2011 7.50% 5.00% 5.00%<br />

2012 7.00% 5.00% 5.00%<br />

2013 6.50% 5.00% 5.00%<br />

2014+ 6.00% 5.00% 5.00%<br />

The required schedule of funding progress presented as required supplementary information immediately<br />

following the notes to the <strong>financial</strong> statements presents multi year trend information about whether the actuarial<br />

value of plan assets is increasing or decreasing over time, relative to the actuarial accrued liability for benefits.<br />

47