NHBC NEW HOMES STATISTICS REVIEW Q1 2012 - NHBC Home

NHBC NEW HOMES STATISTICS REVIEW Q1 2012 - NHBC Home

NHBC NEW HOMES STATISTICS REVIEW Q1 2012 - NHBC Home

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>NHBC</strong> <strong>NEW</strong> <strong>HOMES</strong><br />

<strong>STATISTICS</strong> <strong>REVIEW</strong> <strong>Q1</strong> <strong>2012</strong><br />

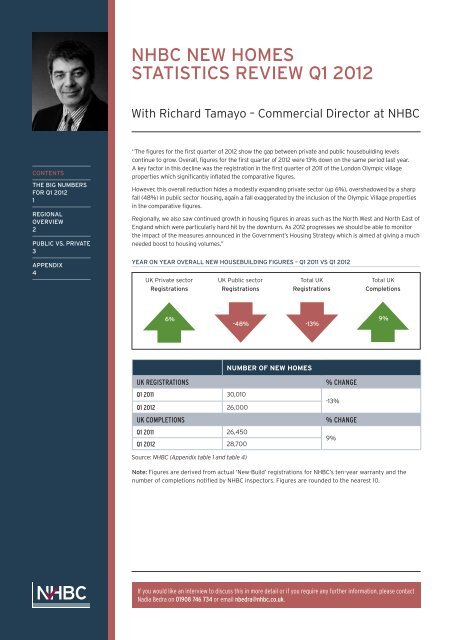

With Richard Tamayo – Commercial Director at <strong>NHBC</strong><br />

CONTENTS<br />

THE BIG NUMBERS<br />

FOR <strong>Q1</strong> <strong>2012</strong><br />

1<br />

REGIONAL<br />

OVERVIEW<br />

2<br />

PUBLIC VS. PRIVATE<br />

3<br />

APPENDIX<br />

4<br />

“The figures for the first quarter of <strong>2012</strong> show the gap between private and public housebuilding levels<br />

continue to grow. Overall, figures for the first quarter of <strong>2012</strong> were 13% down on the same period last year.<br />

A key factor in this decline was the registration in the first quarter of 2011 of the London Olympic village<br />

properties which significantly inflated the comparative figures.<br />

However, this overall reduction hides a modestly expanding private sector (up 6%), overshadowed by a sharp<br />

fall (48%) in public sector housing, again a fall exaggerated by the inclusion of the Olympic Village properties<br />

in the comparative figures.<br />

Regionally, we also saw continued growth in housing figures in areas such as the North West and North East of<br />

England which were particularly hard hit by the downturn. As <strong>2012</strong> progresses we should be able to monitor<br />

the impact of the measures announced in the Government’s Housing Strategy which is aimed at giving a much<br />

needed boost to housing volumes.”<br />

YEAR ON YEAR OVERALL <strong>NEW</strong> HOUSEBUILDING FIGURES – <strong>Q1</strong> 2011 VS <strong>Q1</strong> <strong>2012</strong><br />

UK Private sector<br />

Registrations<br />

UK Public sector<br />

Registrations<br />

Total UK<br />

Registrations<br />

Total UK<br />

Completions<br />

6%<br />

-48% -13%<br />

9%<br />

NUMBER OF <strong>NEW</strong> <strong>HOMES</strong><br />

UK REGISTRATIONS<br />

<strong>Q1</strong> 2011 30,010<br />

<strong>Q1</strong> <strong>2012</strong> 26,000<br />

UK COMPLETIONS<br />

<strong>Q1</strong> 2011 26,450<br />

<strong>Q1</strong> <strong>2012</strong> 28,700<br />

% CHANGE<br />

-13%<br />

% CHANGE<br />

9%<br />

Source: <strong>NHBC</strong> (Appendix table 1 and table 4)<br />

Note: Figures are derived from actual ‘New-Build’ registrations for <strong>NHBC</strong>’s ten-year warranty and the<br />

number of completions notified by <strong>NHBC</strong> inspectors. Figures are rounded to the nearest 10.<br />

If you would like an interview to discuss this in more detail or if you require any further information, please contact<br />

Nadia Bedra on 01908 746 734 or email nbedra@nhbc.co.uk.

page 2 of 10<br />

<strong>NHBC</strong> <strong>NEW</strong> <strong>HOMES</strong><br />

<strong>STATISTICS</strong> <strong>REVIEW</strong> <strong>Q1</strong> <strong>2012</strong><br />

Regional Overview<br />

Quarterly registrations for all sectors (% change <strong>Q1</strong> 2011 on <strong>Q1</strong> <strong>2012</strong>)<br />

DAVID LITTLE, <strong>NHBC</strong> DIRECTOR<br />

NORTHERN IRELAND<br />

“The registration figures for <strong>Q1</strong> show a small but<br />

welcome increase over the same period in 2011.<br />

They are hopefully an indication that we are seeing<br />

the end of the decline in the local housing market<br />

which started in 2007. The figures unsuprisingly<br />

show that most activity is concentrated in the<br />

Belfast commuter area, with an increase also in<br />

the North West.”<br />

PETER WATTON, <strong>NHBC</strong> DIRECTOR<br />

WALES<br />

21%<br />

“The market in Wales continues to be difficult with<br />

the availability of mortgages being the principle<br />

problem. In the first quarter of <strong>2012</strong> <strong>NHBC</strong> has<br />

seen registrations for 731 homes for sale and 147<br />

social homes; 4% down on last year. Many builders<br />

remain upbeat about sales and continue to<br />

open new developments in readiness for the<br />

Spring market.”<br />

38%<br />

-4%<br />

15%<br />

1%<br />

3%<br />

55%<br />

21%<br />

7%<br />

-17%<br />

MALCOLM MACLEOD, <strong>NHBC</strong> DIRECTOR<br />

SCOTLAND<br />

“Although the latest quarterly statistics portray<br />

a positive increase of nearly 40% in the number<br />

of homes registered with <strong>NHBC</strong> compared to the<br />

same quarter last year, these statistics have been<br />

influenced by the registration of the homes forming<br />

the Glasgow Commonwealth Games Athletes village<br />

which is currently under construction. When the<br />

latter homes are discounted the quarterly increase<br />

in registrations over the preceding year, although<br />

remaining positive, reduces to 2% and continues to<br />

run at 44% below its ten year average trend.”<br />

-47%<br />

-29%<br />

STEVE CATT, <strong>NHBC</strong> DIRECTOR<br />

ENGLAND<br />

“The London/South East regions<br />

continue to provide the strongest<br />

registration figures, contributing<br />

nearly 1/3 of all plot registrations<br />

in the UK during <strong>Q1</strong> <strong>2012</strong>.<br />

However, this dominance is not<br />

as strong as it was in the same<br />

period in 2011 and both regions<br />

show a significant decrease in<br />

registrations and ongoing site<br />

activity. Regions in the north of<br />

England have shown the<br />

strongest year on year quarterly<br />

increase, but from a very low<br />

base in 2011.”<br />

Source: <strong>NHBC</strong> (Appendix table 3)<br />

Note: The comparison is based on ‘New-Build’ registrations for <strong>NHBC</strong>’s ten-year warranty.<br />

PERCENTAGE OF UK HOUSE TYPES IN TOTAL REGISTRATIONS - ALL SECTORS<br />

Percentage<br />

50<br />

45<br />

40<br />

35<br />

30<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

17<br />

Detached houses<br />

22<br />

1 1<br />

Detached bungalows<br />

16<br />

Semi-detached houses<br />

20 21<br />

Terraced houses<br />

24<br />

1 1<br />

Attached bungalows<br />

45<br />

Flats and maisonettes<br />

33<br />

<strong>Q1</strong> <strong>2012</strong><br />

<strong>Q1</strong> 2011<br />

Source: <strong>NHBC</strong> (Appendix table 5)<br />

If you would like an interview to discuss this in more detail or if you require any further information, please contact Nadia Bedra on 01908 746 734 or email<br />

nbedra@nhbc.co.uk.

page 3 of 10<br />

<strong>NHBC</strong> <strong>NEW</strong> <strong>HOMES</strong><br />

<strong>STATISTICS</strong> <strong>REVIEW</strong> <strong>Q1</strong> <strong>2012</strong><br />

UK MEDIAN SELLING PRICE OF <strong>NEW</strong> <strong>HOMES</strong> – PRIVATE SECTOR ONLY<br />

Note: These figures are based on the purchaser’s solicitor<br />

confirming to <strong>NHBC</strong> the purchase price of a new home.<br />

Prices are given in £000,s<br />

195<br />

190<br />

185<br />

180<br />

175<br />

170<br />

165<br />

160<br />

155<br />

150<br />

185<br />

<strong>Q1</strong> 2008<br />

165<br />

<strong>Q1</strong> 2009<br />

180<br />

Source: <strong>NHBC</strong> (Appendix table 2)<br />

MEHBAN CHOWDERY, HEAD OF SOCIAL HOUSING AT <strong>NHBC</strong><br />

Generally speaking affordable housing completions<br />

have held steady compared to the same period last year.<br />

Although it was expected that affordable housing levels<br />

would drop due to the slower commencement of the<br />

National Affordable Housing Programme (NAHP) <strong>2012</strong>-1015,<br />

completions came through from those properties which<br />

were stalled from the previous NAHP (2008-2011).<br />

Despite registrations down compared to the start of last<br />

year due to a number of factors, with the fall exaggerated<br />

by the inclusion of the Olympic Village properties in last<br />

year’s figures, we remain confident that looking ahead and<br />

as the new NAHP extends, that social housing levels will<br />

remain consistent.<br />

20000<br />

15000<br />

10000<br />

5000<br />

0<br />

CHART 2: <strong>NHBC</strong> REGISTRATIONS AND COMPLETIONS<br />

35000 Registrations – private sector<br />

30000<br />

Registrations – public sector<br />

Completions – private sector<br />

25000<br />

Completions – public sector<br />

<strong>Q1</strong> 2008<br />

<strong>Q1</strong> 2009<br />

<strong>Q1</strong> 2010<br />

<strong>Q1</strong> 2011<br />

<strong>Q1</strong> <strong>2012</strong><br />

<strong>Q1</strong> 2010<br />

178<br />

<strong>Q1</strong> 2011<br />

190<br />

<strong>Q1</strong> <strong>2012</strong><br />

Number of homes<br />

Source: <strong>NHBC</strong> (Appendix table 4)<br />

If you would like an interview to discuss this in more detail or if you require any further information, please contact Nadia Bedra on 01908 746 734 or email<br />

nbedra@nhbc.co.uk.

page 4 of 10<br />

<strong>NHBC</strong> <strong>NEW</strong> <strong>HOMES</strong><br />

<strong>STATISTICS</strong> <strong>REVIEW</strong> <strong>Q1</strong> <strong>2012</strong><br />

Appendix<br />

TABLE 1: UK REGISTRATIONS AND COMPLETIONS ALL SECTORS<br />

NUMBER OF <strong>NEW</strong> <strong>HOMES</strong><br />

REGISTRATIONS<br />

<strong>Q1</strong> 2008 37,840<br />

<strong>Q1</strong> 2009 16,230<br />

<strong>Q1</strong> 2010 27,970<br />

<strong>Q1</strong> 2011 30,010<br />

<strong>Q1</strong> <strong>2012</strong> 26,000<br />

Jan <strong>2012</strong> 7,830<br />

Feb <strong>2012</strong> 8,510<br />

Mar <strong>2012</strong> 9,660<br />

COMPLETIONS<br />

<strong>Q1</strong> 2008 35,220<br />

<strong>Q1</strong> 2009 25,700<br />

<strong>Q1</strong> 2010 23,200<br />

<strong>Q1</strong> 2011 26,450<br />

<strong>Q1</strong> <strong>2012</strong> 28,700<br />

Jan <strong>2012</strong> 6,480<br />

Feb <strong>2012</strong> 8,850<br />

Mar <strong>2012</strong> 13,370<br />

NOTES<br />

1. <strong>NHBC</strong> statistics are derived almost exclusively from its registered builders, who construct around 80% of the new homes built in the UK.<br />

As such, they represent a unique source of detailed, up-to-date information on new home construction and the house-building industry.<br />

2. A <strong>NHBC</strong> registered builder is required to register a house with <strong>NHBC</strong> at least 21 days before building starts.<br />

3. A house registered with <strong>NHBC</strong> is deemed completed when the <strong>NHBC</strong> Building Inspector, who carried out key stage inspections during<br />

construction, considers that the house has been satisfactorily completed in respect of <strong>NHBC</strong>’s technical requirements.<br />

4. These figures are rounded numbers to the nearest 10.<br />

5. The number of ‘Registrations’ relate to homes registered, less a small percentage reduction to allow for likely cancellations. During an<br />

economic downturn the number of actual cancellations is likely to be higher.<br />

6. The above figures relate to ‘New-Build’ registrations for <strong>NHBC</strong>’s ten-year warranty in the UK, including the Isle of Man.<br />

7. ‘Completions’ relate to the number of homes ‘finalled’ by <strong>NHBC</strong>’s Building Inspectors and are reported in the month they are received<br />

and processed.<br />

If you would like an interview to discuss this in more detail or if you require any further information, please contact Nadia Bedra on 01908 746 734 or email<br />

nbedra@nhbc.co.uk.

page 5 of 10<br />

<strong>NHBC</strong> <strong>NEW</strong> <strong>HOMES</strong><br />

<strong>STATISTICS</strong> <strong>REVIEW</strong> <strong>Q1</strong> <strong>2012</strong><br />

Appendix<br />

TABLE 2: MEDIAN SELLING PRICE OF <strong>NEW</strong> HOUSES – PRIVATE SECTOR ONLY<br />

PRICES ARE GIVEN<br />

IN £000’S<br />

<strong>Q1</strong> 2008 <strong>Q1</strong> 2009 <strong>Q1</strong> 2010 <strong>Q1</strong> 2011 <strong>Q1</strong> <strong>2012</strong><br />

North East 163 137 150 140 153<br />

North West 145 123 140 145 160<br />

Yorkshire & The Humber 155 140 157 141 158<br />

West Midlands 160 145 150 150 150<br />

East Midlands 160 145 148 150 156<br />

Eastern 197 180 198 205 200<br />

South West 195 171 185 180 187<br />

Greater London 275 250 250 290 274<br />

South East 220 195 225 225 240<br />

England 187 166 183 180 192<br />

Scotland 185 161 185 183 198<br />

Wales 175 145 144 155 168<br />

Northern Ireland (incl. Isle of Man) 175 147 144 132 135<br />

United Kingdom (incl. Isle of Man) 185 165 180 178 190<br />

NOTES<br />

1. <strong>NHBC</strong> asks the purchaser’s solicitor to return a document confirming the purchase price of a house.<br />

2. For each update, the previous figures are re-calculated and this can result in some minor changes occuring.<br />

3. Houses includes flats, maisonettes and bungalows.<br />

If you would like an interview to discuss this in more detail or if you require any further information, please contact Nadia Bedra on 01908 746 734 or email<br />

nbedra@nhbc.co.uk.

page 6 of 10<br />

<strong>NHBC</strong> <strong>NEW</strong> <strong>HOMES</strong><br />

<strong>STATISTICS</strong> <strong>REVIEW</strong> <strong>Q1</strong> <strong>2012</strong><br />

Appendix (continued)<br />

TABLE 3: REGIONAL REGISTRATION FIGURES – ALL SECTORS<br />

<strong>Q1</strong> 2008 <strong>Q1</strong> 2009 <strong>Q1</strong> 2010 <strong>Q1</strong> 2011 <strong>Q1</strong> <strong>2012</strong><br />

North East 1,250 610 1,320 690 1,070<br />

North West 3,540 1,490 1,810 1,760 2,030<br />

Yorkshire & the Humber 2,570 1,030 1,900 1,190 1,440<br />

West Midlands 2,900 930 2,350 1,600 1,640<br />

East Midlands 3,240 1,220 2,320 1,780 1,900<br />

Eastern 4,160 2,570 3,500 3,450 2,440<br />

South West 3,090 1,750 3,070 2,940 2,960<br />

Greater London 4,430 1,300 3,100 8,580 4,530<br />

South East 6,350 2,500 4,710 4,760 3,930<br />

England 31,520 13,390 24,080 26,750 21,950<br />

Scotland 4,000 1,450 1,990 1,950 2,700<br />

Wales 1,430 730 1,120 920 880<br />

Northern Ireland (incl. Isle of Man) 890 670 790 390 470<br />

United Kingdom (incl. Isle of Man) 37,840 16,230 27,970 30,010 26,000<br />

Note: Please note these figures are rounded to the nearest 10.<br />

Northern Ireland Registration Figures by County – all sectors<br />

<strong>Q1</strong> 2008 <strong>Q1</strong> 2009 <strong>Q1</strong> 2010 <strong>Q1</strong> 2011 <strong>Q1</strong> <strong>2012</strong><br />

Antrim 142 143 228 120 150<br />

Armagh 132 35 56 18 16<br />

Down 255 358 273 154 138<br />

Fermanagh 60 31 43 34 8<br />

Londonderry 79 48 86 33 101<br />

Tyrone 68 50 64 32 18<br />

If you would like an interview to discuss this in more detail or if you require any further information, please contact Nadia Bedra on 01908 746 734 or email<br />

nbedra@nhbc.co.uk.

page 7 of 10<br />

<strong>NHBC</strong> <strong>NEW</strong> <strong>HOMES</strong><br />

<strong>STATISTICS</strong> <strong>REVIEW</strong> <strong>Q1</strong> <strong>2012</strong><br />

Appendix (continued)<br />

Scotland Registration Figures by Council – all sectors<br />

<strong>Q1</strong> 2008 <strong>Q1</strong> 2009 <strong>Q1</strong> 2010 <strong>Q1</strong> 2011 <strong>Q1</strong> <strong>2012</strong><br />

Aberdeenshire 518 286 174 212 194<br />

Angus 64 7 47 28 48<br />

Argyll & Bute 48 25 15 16 7<br />

City of Aberdeen 135 72 15 129 178<br />

City of Edinburgh 273 194 165 197 235<br />

City of Glasgow 387 29 314 109 841<br />

Clackmannan 6 3 14 7 2<br />

Dumfries & Galloway 30 39 81 7 17<br />

Dundee City 73 19 62 38 6<br />

East Ayrshire 43 8 13 82 67<br />

East Dumbartonshire 0 4 53 134 40<br />

East Lothian 43 32 47 22 38<br />

East Renfrewshire 35 2 17 31 40<br />

Falkirk 207 0 45 16 46<br />

Fife 314 58 210 161 118<br />

Highland 224 86 91 43 79<br />

Inverclyde 45 20 5 18 16<br />

Midlothian 102 1 38 45 124<br />

Moray 23 5 63 8 54<br />

North Ayrshire 62 1 16 67 11<br />

North Lanarkshire 308 95 90 169 97<br />

Orkney Islands 1 21 0 1 1<br />

Perthshire & Kinross 101 21 81 19 63<br />

Renfrewshire 134 8 50 47 58<br />

Scottish Borders 77 19 62 21 30<br />

Shetland Islands 11 1 5 0 0<br />

South Ayrshire 79 0 19 8 62<br />

South Lanarkshire 318 32 144 168 96<br />

Stirling 208 4 30 44 34<br />

West Dumbartonshire 37 0 2 34 54<br />

Western Isles 1 18 13 2 1<br />

West Lothian 97 336 6 65 42<br />

If you would like an interview to discuss this in more detail or if you require any further information, please contact Nadia Bedra on 01908 746 734 or email<br />

nbedra@nhbc.co.uk.

page 8 of 10<br />

<strong>NHBC</strong> <strong>NEW</strong> <strong>HOMES</strong><br />

<strong>STATISTICS</strong> <strong>REVIEW</strong> <strong>Q1</strong> <strong>2012</strong><br />

Appendix (continued)<br />

Welsh Registration Figures by Unitary Authority – all sectors<br />

<strong>Q1</strong> 2008 <strong>Q1</strong> 2009 <strong>Q1</strong> 2010 <strong>Q1</strong> 2011 <strong>Q1</strong> <strong>2012</strong><br />

Blaenau Gwent 35 85 4 1 0<br />

Bridgend 152 67 206 54 112<br />

Caerphilly 41 105 76 55 91<br />

Cardiff 170 117 176 64 76<br />

Carmarthenshire 49 20 70 55 19<br />

Ceredigion 6 2 11 15 0<br />

Conwy 67 6 12 30 48<br />

Denbighshire 4 6 2 54 20<br />

Flintshire 56 3 46 49 44<br />

Gwynedd 6 8 15 9 1<br />

Isle of Anglesey 33 5 7 12 34<br />

Merthyr Tydfil 0 0 26 2 11<br />

Monmouthshire 126 3 120 25 101<br />

Neath Port Talbot 25 23 60 42 17<br />

Newport 263 108 18 180 58<br />

Pembrokeshire 8 14 35 82 9<br />

Powys 89 31 29 8 16<br />

Rhondda Cynon Taff 52 20 85 46 33<br />

Swansea 194 40 70 101 54<br />

Torfaen 2 19 17 13 52<br />

Vale of Glamorgan 1 29 5 0 44<br />

Wrexham 46 18 30 21 38<br />

If you would like an interview to discuss this in more detail or if you require any further information, please contact Nadia Bedra on 01908 746 734 or email<br />

nbedra@nhbc.co.uk.

page 9 of 10<br />

<strong>NHBC</strong> <strong>NEW</strong> <strong>HOMES</strong><br />

<strong>STATISTICS</strong> <strong>REVIEW</strong> <strong>Q1</strong> <strong>2012</strong><br />

Appendix (continued)<br />

TABLE 4: UK PRIVATE AND PUBLIC SECTOR REGISTRATIONS AND COMPLETIONS<br />

PRIVATE SECTOR NUMBER<br />

PUBLIC SECTOR NUMBER<br />

REGISTRATIONS<br />

<strong>Q1</strong> 2008 29,140 8,700<br />

<strong>Q1</strong> 2009 8,610 7,620<br />

<strong>Q1</strong> 2010 18,410 9,560<br />

<strong>Q1</strong> 2011 19,090 10,920<br />

<strong>Q1</strong> <strong>2012</strong> 20,310 5,690<br />

COMPLETIONS<br />

<strong>Q1</strong> 2008 27,400 7,820<br />

<strong>Q1</strong> 2009 17,870 7,830<br />

<strong>Q1</strong> 2010 15,430 7,770<br />

<strong>Q1</strong> 2011 15,670 10,780<br />

<strong>Q1</strong> <strong>2012</strong> 17,010 11,690<br />

NOTES<br />

1. The above figures relate to ‘New-Build’ registrations for <strong>NHBC</strong>’s ten-year warranty in the UK.<br />

2. <strong>NHBC</strong> registration figures are obtained as follows: A builder is required to register a house with <strong>NHBC</strong> at least 21 days before building starts.<br />

3. <strong>NHBC</strong> registration figures reflect an intention to build, they may give an earlier indication of market trends.<br />

4. ‘Completions’ relate to the number of homes ‘finalled’ by <strong>NHBC</strong>’s Building Inspectors and are reported in the month they are received and processed.<br />

5. These figures are rounded.<br />

If you would like an interview to discuss this in more detail or if you require any further information, please contact Nadia Bedra on 01908 746 734 or email<br />

nbedra@nhbc.co.uk.

page 10 of 10<br />

<strong>NHBC</strong> <strong>NEW</strong> <strong>HOMES</strong><br />

<strong>STATISTICS</strong> <strong>REVIEW</strong> <strong>Q1</strong> <strong>2012</strong><br />

Appendix (continued)<br />

TABLE 5: PERCENTAGE OF HOUSE TYPES IN TOTAL REGISTRATIONS<br />

PRIVATE AND PUBLIC SECTOR – PERCENTAGE OF HOUSE TYPE IN TOTAL REGISTRATIONS<br />

COUNTRY YEAR DETACHED<br />

HOUSES<br />

DETACHED<br />

BUNGALOWS<br />

SEMI-DETACHED<br />

HOUSES<br />

TERRACED<br />

HOUSES<br />

ATTACHED<br />

BUNGALOWS<br />

England <strong>Q1</strong> 2008 13% 1% 14% 22% 1% 48%<br />

<strong>Q1</strong> 2009 13% 1% 17% 23% 2% 43%<br />

<strong>Q1</strong> 2010 14% 1% 20% 26% 1% 37%<br />

<strong>Q1</strong> 2011 14% 1% 15% 21% 0% 48%<br />

<strong>Q1</strong> <strong>2012</strong> 20% 1% 21% 23% 0% 35%<br />

Wales <strong>Q1</strong> 2008 16% 2% 17% 22% 1% 41%<br />

<strong>Q1</strong> 2009 9% 2% 17% 29% 4% 39%<br />

<strong>Q1</strong> 2010 27% 1% 28% 19% 1% 23%<br />

<strong>Q1</strong> 2011 42% 1% 25% 17% 0% 15%<br />

<strong>Q1</strong> <strong>2012</strong> 33% 1% 24% 25% 0% 17%<br />

Scotland <strong>Q1</strong> 2008 36% 2% 12% 9% 1% 40%<br />

<strong>Q1</strong> 2009 17% 2% 27% 10% 3% 41%<br />

<strong>Q1</strong> 2010 32% 3% 12% 18% 2% 34%<br />

<strong>Q1</strong> 2011 40% 2% 16% 16% 1% 25%<br />

<strong>Q1</strong> <strong>2012</strong> 33% 2% 13% 32% 1% 19%<br />

FLATS AND<br />

MAISONETTES<br />

Northern<br />

Ireland<br />

<strong>Q1</strong> 2008 32% 5% 26% 21% 0% 16%<br />

<strong>Q1</strong> 2009 21% 7% 17% 20% 2% 33%<br />

<strong>Q1</strong> 2010 22% 6% 28% 24% 0% 20%<br />

<strong>Q1</strong> 2011 40% 8% 22% 18% 0% 12%<br />

<strong>Q1</strong> <strong>2012</strong> 30% 3% 29% 23% 0% 15%<br />

United<br />

Kingdom<br />

<strong>Q1</strong> 2008 16% 1% 14% 21% 1% 46%<br />

<strong>Q1</strong> 2009 13% 1% 18% 22% 3% 42%<br />

<strong>Q1</strong> 2010 16% 1% 20% 25% 1% 36%<br />

<strong>Q1</strong> 2011 17% 1% 16% 21% 0% 45%<br />

<strong>Q1</strong> <strong>2012</strong> 22% 1% 20% 25% 1% 33%<br />

NOTES<br />

1. The above table shows the percentages of different types of homes registered by country.<br />

If you would like an interview to discuss this in more detail or if you require any further information, please contact Nadia Bedra on 01908 746 734 or email<br />

nbedra@nhbc.co.uk.<br />

<strong>NHBC</strong><br />

<strong>NHBC</strong> House, Davy Avenue, Knowlhill, Milton Keynes, Bucks MK5 8FP<br />

Tel: 0844 633 1000 Fax: 0844 633 0022 www.nhbc.co.uk<br />

F135 04/12