download (PDF, 6MB) - Uganda Coffee Federation

download (PDF, 6MB) - Uganda Coffee Federation

download (PDF, 6MB) - Uganda Coffee Federation

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

year book 2011/12<br />

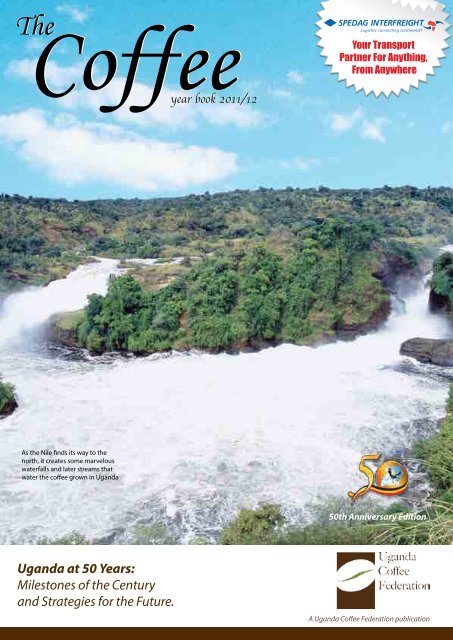

As the Nile finds its way to the<br />

north, it creates some marvelous<br />

waterfalls and later streams that<br />

water the coffee grown in <strong>Uganda</strong><br />

50th Anniversary Edition<br />

<strong>Uganda</strong> at 50 Years:<br />

Milestones of the Century<br />

and Strategies for the Future.<br />

50th Anniversary Edition<br />

A <strong>Uganda</strong> <strong>Coffee</strong> <strong>Federation</strong> publication 1

2 50th Anniversary Edition

50th Anniversary Edition<br />

3

As the Nile finds its way to the north, it creates some<br />

marvelous waterfalls and later streams that help<br />

nourish and water the coffee grown in <strong>Uganda</strong><br />

50th Anniversary Edition<br />

A <strong>Uganda</strong> <strong>Coffee</strong> <strong>Federation</strong> publication<br />

year book 2011/12<br />

<strong>Uganda</strong> at 50 Years:<br />

Milestones of the Century<br />

and Strategies for the Future.<br />

Editorial Team<br />

Editor:<br />

Associate Editor:<br />

Assistant editors:<br />

Betty Namwagala<br />

0414 343 692/8<br />

E: ucf@ugandacoffeetrade.com<br />

Robert Waggwa Nsibirwa<br />

Samson Emong<br />

Helen Mirembe<br />

Design &Layout:<br />

Ideas Advertising<br />

+256 312 109 544<br />

E: info@ideasug.net<br />

Publishers:<br />

<strong>Uganda</strong> <strong>Coffee</strong> <strong>Federation</strong><br />

2nd Floor, <strong>Coffee</strong> House<br />

Plot 35 Jinja Road<br />

Tel: +256 414 343 692/77<br />

E: ucf@ugandacoffeetrade.com<br />

www.ugandacoffeetrade.com<br />

4 50th Anniversary Edition

50th Anniversary Edition<br />

5

Inside<br />

7. President’s Statement<br />

10. UCDA MD’s Statement<br />

11. Executive Director’s Statement<br />

12. <strong>Coffee</strong>: A Commodity that has stood the times<br />

19. <strong>Coffee</strong>’s Contribution To <strong>Uganda</strong>’s Economic Development Since<br />

Independence<br />

26. aBi Trust and <strong>Coffee</strong> Value Chain Development in <strong>Uganda</strong><br />

30. Milestones of the Century in Trade and<br />

Marketing <strong>Coffee</strong> in <strong>Uganda</strong> and Strategies for the next Century<br />

36 Climate Change From A Farming Perspective<br />

41. Third <strong>Uganda</strong> <strong>Coffee</strong> Day<br />

47. Direction Of The <strong>Uganda</strong> <strong>Coffee</strong> Industry From The Farmer’s Perspective<br />

51. Technical overview of environmental impact of land application of<br />

pulping effluent from wet coffee<br />

processing.<br />

56. Production And Processing Problems Of Arabica <strong>Coffee</strong> Farmers In<br />

Eastern <strong>Uganda</strong><br />

66. Apendexes<br />

72. What is UCTF<br />

73. Ucf Member Benefits<br />

74. Ucf Member Profile<br />

78. Advertiser’s Index<br />

6 50th Anniversary Edition

President’s Statement<br />

David Barry<br />

UCF President<br />

<strong>Uganda</strong> exported just over 2.7m bags of coffee during the<br />

coffee year 2011-12 split 70% robusta and 30% arabica<br />

by volume. This was down about 400k bags from the<br />

previous year. Direct export earnings came to a total of $393m of<br />

which Arabica coffees contributed 43%. Volumes produced and<br />

exported were disappointing as most of us had envisaged total<br />

exports a little over the 3.0m bags mark but it seems various<br />

weather factors were adequately negative to severely impact the<br />

size of the Robusta component of the crops.<br />

There were many positive efforts made in the industry by <strong>Uganda</strong><br />

<strong>Coffee</strong> Development Authority and the private sector assisted by<br />

the Government of <strong>Uganda</strong>, Non-Governmental Organisations<br />

and Donors. These multiple efforts combined with relatively<br />

decent prices seem to have rekindled small holder and medium<br />

sized farmer’s enthusiasm for coffee growing. The UCDA report<br />

indicated that about 17million shade and coffee tree seedlings<br />

were planted during the year which is highly significant.<br />

About half of the 44 registered exporters in the country each<br />

exported more than 1% of total country exports with the top 10<br />

exporters responsible for around 80% of exports.<br />

<strong>Uganda</strong> coffee was directly exported to 37 countries outside of<br />

the enlarged EU which accounted for 67.5% of the total. Sudan<br />

remains a key destination for <strong>Uganda</strong> coffees taking over 400,000<br />

bags during the year whilst the USA absorbed about 100,000 bags.<br />

<strong>Uganda</strong> is following the international trend to certify more of<br />

its coffee. <strong>Coffee</strong> exporters and farmer organisations expanded<br />

their sustainable projects. Mr. Robert Waggwa Nsibirwa of the<br />

African <strong>Coffee</strong> Academy who was elected the chairman of the<br />

4C association has brought to the table the issue of low coffee<br />

productivity, a topic largely overlooked by the certification<br />

standards but understood by everyone actually working with<br />

smallholder farmers.<br />

One of the key features of the international market last<br />

year was the pronounced blend, changing from Arabicas to<br />

Robustas which took place in many markets.<br />

250.00<br />

COFFEE FUTURES MARKETS PRICES (Oct 11 - Sep 12)<br />

One of the key features of the international market last year was<br />

the pronounced blend, changing from Arabicas to Robustas<br />

which took place in many markets. Price has been one of the<br />

key drivers of this development as it is increasingly clear that<br />

economically hard-pressed consumers have not stopped drinking<br />

coffee but have rather switched to cheaper blends. The resulting<br />

fall in Arabica prices and differentials has been tough on <strong>Uganda</strong>n<br />

Arabica farmers and dealers but the adjustments have been made<br />

and the business model remains intact and profitable.<br />

US CTS / LB<br />

200.00<br />

150.00<br />

100.00<br />

50.00<br />

-<br />

ROBUSTA - LIFFE ARABICA - ICE ARBITRAGE<br />

Most of the people we speak to seem optimistic about the prospects<br />

for coffee production in <strong>Uganda</strong> and it seems increasingly evident<br />

that the focus on coffee over the last few years is starting to pay<br />

dividends. We are optimistic about volumes in the coming coffee<br />

year; and with decent enough prices and satisfactory weather<br />

we can look forward to both improving volumes and excellent<br />

qualities across the range of coffees produced.<br />

50th Anniversary Edition<br />

7

8 50th Anniversary Edition

Structured<br />

commodity trade<br />

Are you a trader or exporter of products<br />

produced or processed in <strong>Uganda</strong>? Stanbic<br />

Bank provides tailor made trade finance<br />

solutions to meet your specific needs.<br />

Richard Wangwe<br />

Head, Agriculture <strong>Uganda</strong><br />

We offer structured trade and commodity finance:<br />

Warehouse Receipt Financing<br />

To facilitate procurement and bulking of commodities<br />

for export or sold locally.<br />

Pre and Post Season Agricultural Commodity<br />

Financing Facility<br />

Facility to finance the purchase, processing,<br />

packaging and exportation of commodities for<br />

international export.<br />

Collateral Managed Agricultural Commodity<br />

Warehousing Facility<br />

Collateral managed facility to finance the import<br />

of cereals and grains, that will be released against<br />

payment by the client for the purpose of milling and<br />

subsequent distribution to local markets.<br />

Trade Finance <strong>Coffee</strong> Procurement Facility<br />

For procurement of processed coffee produced by<br />

local farmers, for on-sale to international buyers.<br />

Trade Finance Export Facility<br />

To finance the purchase of coffee produced in the<br />

current season by pre-financing firm fixed price,<br />

fixed quantity off take contracts entered into with<br />

international buyers. Stanbic Bank advances financing<br />

to buy coffee from buying companies for export.<br />

The above can either be self liquidating<br />

collateral managed or financed against fixed<br />

assets<br />

Our Structured commodity trade finance solutions<br />

ensure faster payments from international buyers in<br />

addition to providing customized financial solutions to<br />

meet your cash flows needs.<br />

Contacts us at:<br />

Stanbic Bank - Agriculture Financing<br />

9 th Floor, Short Tower, 17 Hannington Road, Crested Towers Building.<br />

P O Box 7131 Kampala. Tel +256 417 154 000/446/210<br />

Stanbic Bank <strong>Uganda</strong> Limited A financial institution regulated by Bank of <strong>Uganda</strong> License Number A1. 013<br />

50th Anniversary Edition<br />

9

UCDA MD’s Statement<br />

Henry Ngabirano<br />

MANAGING DIRECTOR, UCDA<br />

I<br />

wish to congratulate all the coffee stakeholders upon completion<br />

of the 2011/12 coffee year. The year was characterized by reduced<br />

coffee volumes compared to 2010/2011 due to weather related<br />

factors, pests and diseases and price fluctuations. As a result, coffee<br />

exports for the year were down by 13.4% and 12.5 % in volume and<br />

value respectively.<br />

<strong>Coffee</strong> continues to play a vital role in <strong>Uganda</strong>’s economy contributing<br />

to about 20-30% of the foreign exchange earnings and employing<br />

over 3.5 million households. Due to its importance the Government<br />

of <strong>Uganda</strong> has always taken coffee as a priority export crop and it has<br />

featured in its many programs such as: Prosperity for All Programme<br />

(PFA); National Export Strategy (NES); Plan for Modernization of<br />

Agriculture (PMA) and National Agricultural Advisory Services<br />

(NAADS), among others.<br />

In order to increase production, the Government through UCDA, has<br />

increased the momentum in coffee replanting and rehabilitation<br />

programme, through mass production of <strong>Coffee</strong> Wilt Disease Resistant<br />

planting materials using tissue culture and this is aimed at increasing<br />

coffee production and productivity. Support has also been given to<br />

the coffee scientists to do more research given that many challenges<br />

are foreseen as a result of climate change. With this, it is envisaged that<br />

by 2015 coffee exports will have increased to 4.5 million bags from the<br />

current annual average of 3 million bags.<br />

The International <strong>Coffee</strong> Organization (ICO) predicts that, coffee<br />

production for the coming year will increase at an estimated volume<br />

of 144.1 million bags an increase of 7.2% compared to 134.4 million<br />

bags in 2011/12. Global coffee consumption is increasing steadily at<br />

2.4% per annum. There is a growing demand for sustainable coffees<br />

in consuming countries and therefore this is an opportunity that we<br />

need to exploit.<br />

Value addition at all levels of the coffee value chain is being promoted<br />

through wet processing in both Arabica and Robusta coffees, a practice<br />

that has improved on the quality and incomes of the farmers. UCDA<br />

will continue to ensure that quality standards are adhered through<br />

enforcement of <strong>Coffee</strong> Regulations. His Excellence the President has<br />

come out strongly to emphasize the importance of maintaining high<br />

quality <strong>Uganda</strong>n <strong>Coffee</strong> while the Police and Local Authorities have<br />

allied with UCDA to enforce it.<br />

In order to increase production, the Government<br />

through UCDA, has increased the momentum in<br />

coffee replanting and rehabilitation programme,<br />

through mass production of <strong>Coffee</strong> Wilt Disease<br />

Resistant planting materials using tissue culture and<br />

this is aimed at increasing coffee production and<br />

productivity<br />

On behalf of UCDA Board, Management and Staff I wish to thank all<br />

coffee stakeholders who are doing a tremendous work in adding value<br />

to coffee. Special thanks go to all those exporters and development<br />

partners who have taken the initiative of helping farmers in terms<br />

of inputs, trainings and financial assistance. This has tremendously<br />

improved on production and quality of coffee. UCDA will always<br />

partner with you as we strive to make <strong>Uganda</strong> a distinguished<br />

producer of high value coffee. To all the participants in the 10th African<br />

Fine <strong>Coffee</strong>s Conference and Exhibition, I wish you good deliberations<br />

and a pleasant stay.<br />

10 50th Anniversary Edition

ED’s Statement<br />

Betty Namwagala<br />

Executive Director - UCF<br />

At the time of liberalisation of the <strong>Uganda</strong> coffee industry<br />

and the enacting of the UCDA Statute in 1991, it was only<br />

the <strong>Coffee</strong> Marketing Board and the Cooperative Societies<br />

that were eligible to export coffee. When liberalisation took effect,<br />

the private coffee exporters faced tremendous challenges but<br />

had no forum for addressing them and therefore decided to form<br />

an Association that would provide a voice for them and thus the<br />

<strong>Uganda</strong> <strong>Coffee</strong> Exporters Association (UCEA) was born.<br />

However, in 1996 the <strong>Coffee</strong> Exporters realised that they could not<br />

operate in isolation, and therefore the Association resolved to bring<br />

other players on board and these included the farmers, processors,<br />

traders, exporters, logistic companies, insurance companies and<br />

banks. Although the regulatory mandate was maintained by the<br />

Government, the expansion of Membership gave the Association an<br />

edge to take charge of their affairs including efficiency, profitability<br />

and investments. As a result, the expansion rendered the Association<br />

non representative; and therefore the emergence of <strong>Uganda</strong> <strong>Coffee</strong><br />

Trade <strong>Federation</strong> that was emerged and was incorporated in 1996.<br />

The <strong>Federation</strong> developed various systems and instruments aimed at<br />

assisting the coffee traders to work in a professional manner in their<br />

transactions and efficiently respond to the market forces both locally<br />

and globally. UCTF made a landmark in the policy arena through<br />

advocacy that removed many constraints in the coffee business,<br />

contributed to capacity building and helped to build a critical mass<br />

in the industry.<br />

The <strong>Federation</strong> developed various systems and<br />

instruments aimed at assisting the coffee traders<br />

to work in a professional manner in their transactions<br />

and efficiently respond to the market<br />

forces both locally and globally.<br />

Leaving the Comfort Zone-Time for Change<br />

While there has been some landmarks registered, there has also been<br />

growing pressure from some circles within the coffee value chain<br />

demanding for change. Hence at the 2nd <strong>Uganda</strong> <strong>Coffee</strong> Day of<br />

6th October 2011 where the <strong>Coffee</strong> Fraternity was well represented<br />

and under the Nakanyonyi Declaration of 2011, the <strong>Coffee</strong> industry<br />

decided to that it was time for the <strong>Uganda</strong> <strong>Coffee</strong> ‘Trade’ <strong>Federation</strong><br />

to shed off the “Trade” and become <strong>Uganda</strong> <strong>Coffee</strong> <strong>Federation</strong>.<br />

Overall the change was a noble call to better reflect the broad<br />

membership of stakeholders in the coffee industry yet by and large<br />

the <strong>Federation</strong> has continued to serve not only its members but<br />

the entire sub-sector through organising platforms for knowledge<br />

sharing, networking and building business relationships; training,<br />

and promotion among others.<br />

Some of the factors that led to this include but not limited to:<br />

• Both backward and forward integration of members along<br />

the value chain;<br />

• Feeling of exclusion by some members that are not directly<br />

involved in coffee trade;<br />

• Need to appeal to new audience and grow membership.<br />

The future of the <strong>Federation</strong> involves consolidating the past<br />

achievements while scanning the environment for potential<br />

challenges and opportunities at all levels of the coffee value chain<br />

to ensure a thriving and sustainable coffee industry in <strong>Uganda</strong>. The<br />

<strong>Federation</strong> will also continue to offer value for money services so<br />

that members remain competitive in the global coffee industry.<br />

50th Anniversary Edition<br />

11

12 50th Anniversary Edition

“<strong>Coffee</strong>: A Commodity that has stood the times.”<br />

By Frederick S.M. Kawuma,<br />

Secretary General, Inter-African <strong>Coffee</strong> Organisation (IACO).<br />

Introduction<br />

<strong>Coffee</strong> has<br />

its origins<br />

in Africa.<br />

Ethiopia is the<br />

birthplace of<br />

Arabica coffee,<br />

while <strong>Uganda</strong> is<br />

the birthplace of<br />

Robusta coffee. It<br />

is remarkable that<br />

from the humble<br />

beginnings in<br />

Eastern Africa,<br />

the cultivation of<br />

coffee has spread around the globe,<br />

between the Tropic of Cancer and<br />

the Tropic of Capricorn. Nonetheless,<br />

Ethiopia and <strong>Uganda</strong> have an enormous<br />

genetic resource pool, with so many<br />

different coffee varieties some of which<br />

still grow wild, and which provide a<br />

sizeable bank of genetic material for<br />

the coffee researchers in their breeding<br />

programmes, whether for productivity<br />

enhancement, disease resistance or<br />

weather tolerant purposes. While<br />

disease outbreaks have threatened<br />

coffee at different times, and a host of<br />

pests have attacked it, and there had<br />

been fears that the crop could easily be<br />

wiped out, it has remained resilient.<br />

Indeed coffee has weathered many<br />

challenges over the years, but its<br />

production has continued to grow, as<br />

has its consumption. <strong>Coffee</strong> is a tropical<br />

crop, and does well in growing regions<br />

that have moderate sunshine and rain,<br />

steady temperatures, for Arabica around<br />

20ºC and Robusta around 25 ºC. <strong>Coffee</strong><br />

will not appreciate extremes of weather<br />

such as cold winters or extremely hot<br />

temperatures. In addition, to do well, coffee also requires<br />

rich, porous soil, and in return the tree will yield very<br />

good beans. <strong>Coffee</strong> is the economic mainstay for dozens<br />

of countries and employs over 25 million people, most<br />

of who live in rural communities. <strong>Coffee</strong> stands out<br />

among natural commodities, with a reputation of being<br />

the second most traded commodity after oil. <strong>Coffee</strong> has<br />

maintained its important position through the decades.<br />

Arabica coffee is ideally grown at higher altitudes that<br />

Robusta, and tends to be mild in its taste compared to<br />

Robusta which mainly grows in lowland areas and under<br />

harsher conditions. There are exceptions however, where<br />

Arabica coffee is grown at altitudes below 1000 metres<br />

above sea level such as in Costa Rica, and where Robusta<br />

is grown at altitudes above 1000 meters above sea level in<br />

<strong>Uganda</strong>. In fact, the latter explains why <strong>Uganda</strong>’s Robusta<br />

is unique in taste and flavour compared to many other<br />

Robustas. Generally, Arabica coffee trees produce much<br />

bigger beans, which also have higher intrinsic quality and<br />

have lower caffeine. Robusta beans are generally smaller,<br />

and the taste is a bit harsh, and with slightly more caffeine<br />

than Arabica. There are so many coffee varieties some of<br />

which are used for research purposes, and by crossing the<br />

new species with other known coffees, researchers have<br />

been exploring the introduction of two new features to<br />

commercially cultivated coffee plants – coffee beans<br />

without caffeine and coffee trees that are self pollinating.<br />

However, the many varieties are not commercially viable,<br />

leaving only Arabica and Robusta, which in 2009/10<br />

accounted for 93.4 million bags worth US$15.4, of which<br />

about 70% is Arabica and 30% is Robusta.<br />

Why is <strong>Coffee</strong> Important?<br />

The coffee beverage is a popular drink the world over. The<br />

proliferation of cafes in North America and Europe has<br />

especially helped to popularise the drink. Big brand names<br />

such as Starbucks have influenced a coffee consumption<br />

culture the same way MacDonalds set the trend for fast<br />

foods. The caffeine in coffee beans is reputed to be the key<br />

attraction, but even with decaffeinated coffee the aroma<br />

itself is a great attraction.<br />

The views presented in this article are those of the author and not of the Inter-African <strong>Coffee</strong> Organisation (IACO) nor of its<br />

Member states.<br />

50th Anniversary Edition<br />

13

There are intrinsic qualities in coffee that<br />

make it a unique beverage, and it fulfils<br />

the desires of many from romantic to<br />

stamina for concentrated study, the latter<br />

helping students to keep alert especially<br />

in periods of preparing for examinations.<br />

An interview with a coffee drinker or<br />

enthusiast will definitely give you a<br />

variety of reasons for the love for coffee.<br />

And they are all valid!<br />

African coffee producers have a relatively<br />

high dependence on revenues from<br />

coffee exports, and coffee is a commodity<br />

that is responsible for the employment<br />

and livelihood of about a significant<br />

proportion of the population. Over the<br />

last two decades, several African nations<br />

have implemented far-reaching policies<br />

of reform and liberalisation in their<br />

economies and in the coffee industry<br />

in particular. Sub-Saharan economies<br />

are agrarian in nature and have to make<br />

swift progress towards industrialisation<br />

in order to reduce their dependence<br />

on agriculture for both employment<br />

and foreign exchange earnings. While<br />

a number of African countries have<br />

reported successful oil exploration,<br />

and positive mineral prospects exist in<br />

others, agriculture has to be given special<br />

attention in order to ensure food security.<br />

While some of the producers have been<br />

hard-wearing, unfortunately due to a<br />

variety of reasons some of the other<br />

coffee producing countries in Africa have<br />

had significant decline in production. Civil<br />

strife, inefficient marketing and poorly<br />

supported production systems have all contributed to<br />

the decline, in different proportions. The lack of support<br />

whether in research, extension or access to finance, have<br />

had devastating effects on the coffee industry. In most<br />

cases, coffee is primarily grown by smallholders, and<br />

thus plays a vital role in rural employment and income<br />

assurance. With its decline in some of the cases, the<br />

effects on the population and rural economies have been<br />

far reaching. Unfortunately the decline has been great<br />

in Africa, losing almost 50% of its previous market share,<br />

over the last two decades. Other producing regions have<br />

taken advantage of the global market opportunities, as<br />

seen in the increase in global exports from 80 million bags<br />

in 1990/91 to 103 million bags in 2010/11. During that<br />

period, Africa’s coffee exports declined from 18.6 million<br />

bags to 10.6 million bags. Thus, in a growing market Africa<br />

has lost market share. While the commodity itself has<br />

withstood tough times, and in spite recessions demand<br />

has grown, Africa now faces the challenge of regaining its<br />

position in the global market place.<br />

According to the International <strong>Coffee</strong> Organisation (ICO),<br />

in 2010 the total coffee sector employment was estimated<br />

at about 26 million people in 52 producing countries.<br />

World coffee trade statistics and information given by the<br />

ICO also shows that for many countries, coffee exports are<br />

not only a vital contributor to foreign exchange earnings<br />

but also account for a significant proportion of tax income<br />

and gross domestic product.<br />

Over the last two decades, several<br />

African nations have implemented<br />

far-reaching policies of reform and<br />

liberalisation in their economies and<br />

in the coffee industry in particular.<br />

14 50th Anniversary Edition

For several countries the average share<br />

of coffee exports in total export earnings<br />

exceeded 10 percent in the period 2000–<br />

2010, although the importance of coffee<br />

for many countries is diminishing over<br />

time as their economies diversify. The<br />

African countries that recorded significant<br />

dependence on coffee earnings were<br />

led by Burundi whose average share of<br />

coffee exports in total export earnings was<br />

reported as 59%. Ethiopia was at 33%,<br />

Rwanda at 27% and <strong>Uganda</strong> at 18%.<br />

The Imminent Threat<br />

The media keeps providing new<br />

information and statistics on environmental<br />

degradation, global warming, and so on. All<br />

these have a serious bearing on the coffee<br />

industry because production may be even<br />

more endangered in some regions. Studies<br />

have indicated that coffee consumption is<br />

increasing at a rate of 2-3 percent a year, but<br />

other facts relating to production systems<br />

show that coffee supply in the long-term<br />

may be threatened by environmentallydamaging<br />

farming methods. It is also<br />

feared that farmers could switch to other<br />

crops or abandoning their land completely.<br />

This has already happened in Kenya, where<br />

coffee production has progressively shrunk<br />

as some coffee farms have been turned<br />

into real estate developments, while in<br />

some cases horticultural farming has been<br />

found more lucrative, and coffee trees have<br />

been replaced with other higher-income<br />

crops. Nevertheless, there have been those<br />

who have persisted and some of these<br />

continue to obtain rewarding prices at the<br />

coffee auction. It is not only in Africa where<br />

production has declined, as the same<br />

trend has been seen in Colombia where<br />

almost two thirds of the original volume of<br />

production has been shed!<br />

In different African countries, several studies<br />

have been undertaken over the years, in the<br />

agricultural sector, identifying certain crops<br />

as possessing great potential in terms of<br />

boosting the rural economy, and uplifting<br />

the welfare of the producers. For instance,<br />

in <strong>Uganda</strong> farmers were encouraged to rear<br />

silk-worms, grow vanilla, and some food<br />

crops which would have been able to obtain<br />

better prices than those for coffee, but value<br />

chain constraints made it impossible to<br />

realise the farmers’ dreams. Subsequently,<br />

those who had abandoned coffee came<br />

back to the fold. However, they should not be taken for<br />

granted as they can easily move their investment into<br />

other higher income generating ventures, if they present<br />

themselves, and coffee lets them down. It is therefore<br />

imperative that in each country a system of support for<br />

the coffee sector is established, through private sector<br />

networks and initiatives to adequately address the value<br />

chain bottlenecks that may exist. If this is supported by a<br />

policy framework that enhances efficiency and promotes<br />

business transactions, there are many positive ripple<br />

effects that will be experienced.<br />

Where will the Hope come from?<br />

Whereas production has declined in Africa, Brazil and<br />

Vietnam have significantly increased their production,<br />

while the production in India too has been resilient.<br />

In Africa, Ethiopia has taken the lead to ramp up<br />

its production and others indicate that they will be<br />

revamping their coffee sectors. If this becomes a reality,<br />

it will give hope to the consumers who are worried that<br />

their beloved beverage might become a dream.<br />

Uniform flowering and ripening of coffee is almost non existent in<br />

<strong>Uganda</strong> and most especially Robusta growing areas. .<br />

The media keeps providing new information<br />

and statistics on environmental degradation,<br />

global warming, and so on. All these have a<br />

serious bearing on the coffee industry because<br />

production may be even more endangered in<br />

some regions.<br />

50th Anniversary Edition<br />

15

Ethiopia, the natural home of the Arabica tree, is Africa’s<br />

top Arabica exporter and leads the continent in domestic<br />

consumption.<br />

The strategy of the Ethiopian government to support<br />

the replacement of old trees and replanting new areas is<br />

paying dividends as annual production and export figures<br />

increase. <strong>Coffee</strong> is very significant in the lives of about 12<br />

million Ethiopians who make their living from it, and this<br />

has serious macro-economic ramifications. With Ethiopia<br />

setting such a good pace, there are many lessons for other<br />

African producing countries. Other countries, especially<br />

<strong>Uganda</strong>, have attempted to follow Ethiopia’s example, but<br />

are still a long way off. Ethiopia and Kenya have the greatest<br />

number of coffee researchers, and this also reflects on<br />

the progress that has been made in the introduction of<br />

new planting materials, albeit Kenya has its own special<br />

problems that have inhibited coffee’s expansion. In the<br />

case of Côte d’Ivoire, once Africa’s leading coffee producer,<br />

civil strife decimated their crop but the sector is on its way<br />

to recovery, and has very good promise.<br />

The African <strong>Coffee</strong> Research Network is promising a<br />

coordinated effort in addressing the research constraints<br />

in Africa so as to provide the direction that the industry<br />

can take to emulate Brazil and Vietnam in increasing<br />

productivity, while also ensuring that high quality coffee<br />

is produced. One of the efforts that are needed is to<br />

build the capacity of the coffee research institutions in<br />

Africa, boosting the scientists, and providing the needed<br />

resources, in order to address the concerns of the industry<br />

with cutting edge research and innovations that will bring<br />

Africa back into the league of global coffee leadership,<br />

especially in quality terms. Through various collaborative<br />

efforts, African coffee producing countries will be able to<br />

share technologies, have exchange visits to share in best<br />

practices, promote policy reviews and appropriate actions<br />

to revamp the coffee sector and seek joint technical<br />

cooperation.<br />

African coffee producing countries suffer the fate of being<br />

exporters of raw commodities, and where attempts are<br />

made for value addition there are a number of tariff and<br />

non-tariff barriers that that restrict access of processed<br />

coffee products on the market in Organisation for Economic<br />

Co-operation and Development (OECD) countries. As long<br />

as African producers export unprocessed green coffee, it<br />

is subject to the vagaries of extreme price fluctuations on<br />

the commodity exchanges. If a good proportion of the<br />

exports were in the form of finished products ready for<br />

consumption, earnings would be more stable and would<br />

be substantially more than is the case with raw products.<br />

There are however, opportunities for developing the<br />

market within the African coffee consuming countries,<br />

where benefits of the Regional Economic Communities<br />

could be explored.<br />

While the coffee market continues to be characterised<br />

by strong demand from industrialised countries, African<br />

producers have been largely unable to take advantage of<br />

this market opportunity. For instance, the United States is<br />

the biggest importer of coffee – accounting for more than<br />

26 million 60-kilo bags in the calendar year 2011, according<br />

to the International <strong>Coffee</strong> Organisation (ICO). In terms<br />

of expenditure on coffee, the US spends approximately<br />

US$8.62 billion on coffee (imports) in the same year. The<br />

ICO figures also show that Germany imported 20.9 million<br />

bags in 2011, worth about US$5.9 billion. Europe is the<br />

most important destination of African coffee, accounting<br />

for over 90% of African coffee exports, all in the form<br />

of green coffee.1 The contrast is that while a 250-gram<br />

pack of coffee will cost about US$5 on the shelves in the<br />

consuming countries (about US$20 per kg), the African<br />

exporter may receive a price of US$1.50 per kg, and due<br />

to the tariff and non-tariff barriers is unable to access the<br />

market for the finished product. When all the value added<br />

to the product is in a developed country, the producing<br />

country fails to benefit from all the multiplier effects of<br />

processing at origin. But this could be addressed through<br />

targeting the African market for coffee – including the<br />

North African countries, the Republic of South Africa and<br />

the Middle East market.<br />

1 According to Statistics from FAO, the majority of coffee imports<br />

into the OECD countries from the producers occur in the form of green,<br />

unprocessed coffee -- 98% of American imports and 94% of European<br />

imports are raw, unroasted beans.<br />

16 50th Anniversary Edition

Thus a proportion could be<br />

exported as finished product; some<br />

could still go as green coffee, and<br />

also as premium or certified coffees.<br />

It is noted that in most African<br />

countries there has been an<br />

emphasis on export volume where<br />

the pre-occupation has been<br />

with how to increase production.<br />

However, there has been a lack of<br />

investment in quality improvement,<br />

and coupled with poor planning<br />

and execution of any existing<br />

improvement agenda, and thus<br />

there has been prevalent low<br />

quality and declining productivity<br />

per hectare.<br />

Another unfortunate trend has<br />

been the prevalence of most<br />

African coffee exports ending up<br />

as commercial coffees, in the mass-market for<br />

coffee in Europe. In spite of the declining trend in<br />

some African countries, there have been emerging<br />

innovations as seen in the new investments in<br />

estate production, in some parts by the new middle<br />

class while in others by foreign investors, which has<br />

altogether shown that coffee in Africa is resilient,<br />

and will stand the test of time.<br />

Conclusion<br />

According to Hubert Weber, the global head of coffee<br />

at Mondelez International Inc., the coffee industry<br />

risks running short of beans in coming years, if<br />

sustainable farming methods are not promoted.<br />

Mondelez is a company that was carved out of Kraft<br />

Foods Inc in 2012, and this may have been done so<br />

as to specifically focus on getting the right coffee<br />

for the future, in anticipation of the market needs<br />

and tastes. In fact, in 2013, Mendelez is targeting<br />

to source 65% of their coffee from sustainable<br />

production systems. It is certainly setting a good<br />

pace for other players in the industry, and producers<br />

are looking forward to receiving rewards for the<br />

effort in their investments in sustainable farms.<br />

As investment in estates picks up, and farmer<br />

groups sell their coffee either as a cooperative or<br />

farmers association, there are opportunities in the<br />

market that can be grasped, of single origin coffees.<br />

African coffee producers can take advantage of<br />

this opportunity, whether it is for green or roasted<br />

coffee. What is marketed as single-origin coffee<br />

is coffee that is grown within a single known<br />

geographical origin, which could be a single farm, or a an<br />

agglomeration of coffee grown within a given locality or<br />

even from a single country, with unique characteristics.<br />

When coffee is marketed as single-origin, the name<br />

of the coffee is then usually the place it was grown to<br />

whatever degree available, such as Yirgacheffe, Sidamo,<br />

Nyeri, Bugisu, Kilimanjaro, Mzuzu, etc. Single-origins are<br />

viewed by some as a way to get a specific taste, and some<br />

independent coffee shops have found that this gives them<br />

a way to add value over large chains. Estate coffees are<br />

a specific type of single-origin coffee. They are generally<br />

grown on a single farm, such as Mringa Estate in Tanzania,<br />

Mzima Estate in Kenya, which might range in size from<br />

a few acres to large plantations occupying many square<br />

miles, or a collection of farms which all process their<br />

coffee at the same mill, such as the Kaweri in Mubende,<br />

<strong>Uganda</strong> or Munali farm in Zambia. Sometimes, micro-lot<br />

coffees are another type of specific single-origin coffee<br />

from a single field on a farm, a small range of altitude, and<br />

specific day of harvest, and the Nairobi <strong>Coffee</strong> Exchange<br />

sells many lots of this type.<br />

Indeed, I dare say, coffee has stood the test of time as<br />

a commodity that is so dear to both its producers and<br />

consumers. Some have done a lot more than others in<br />

investing in research, production and even marketing,<br />

while others have done less. Some far too less than<br />

others! The test for the future is to see who will have<br />

taken more seriously their verbal or written commitments<br />

or even political promises, beyond mere rhetoric, and<br />

demonstrated that they care for the producers of this<br />

valued commodity. The consumers will be delighted to<br />

know that something is being done, hopefully more that<br />

they expected, to ensure that they will continue to enjoy<br />

the pleasure that comes from a lovely cup of coffee.<br />

50th Anniversary Edition<br />

17

UGACOF Limited, Bweyogerere, Kiira<br />

P.O. Box 7355, Kampala – <strong>Uganda</strong><br />

Fax: +256 312 250020,<br />

Tel: +256 414 286288 / 126<br />

E-mail: reception@ugacof.com<br />

Web: www.ugacof.com<br />

18 50th Anniversary Edition

MINISTRY OF AGRICULTURE, ANIMAL<br />

INDUSTRIES AND FISHERIES<br />

COFFEE’S CONTRIBUTION TO UGANDA’S ECONOMIC<br />

DEVELOPMENT SINCE INDEPENDENCE<br />

By James Kizito-MayanjaPrincipal Information Officer, UCDA<br />

2 History of <strong>Coffee</strong> Production in<br />

<strong>Uganda</strong><br />

<strong>Uganda</strong> grows two types of coffee: Robusta and Arabica<br />

in the ratio of 4:1. Whereas Robusta was originally grown<br />

around Lake Victoria, Arabica, it is believed, originated<br />

from Malawi, hence its original name, Nyasaland. By 1914<br />

European and Asian farmers had established 135 coffee<br />

plantations, occupying 58,000 acres of land. However,<br />

the crop was abandoned when prices fell in the 1920s.<br />

<strong>Coffee</strong> production was left to African smallholders,<br />

though at first the acreage was insignificant, by 1931, only<br />

17,000 acres were under cultivation. The <strong>Coffee</strong> Board<br />

was set up in 1929, later becoming the <strong>Coffee</strong> Industry<br />

Board (1943) and then <strong>Coffee</strong> Marketing Board (1959).<br />

1 Introduction<br />

<strong>Coffee</strong> continues to play a pivotal role in the<br />

<strong>Uganda</strong>n economy contributing immensely<br />

to the export earnings to the tune of US$ 449<br />

million and US$ 393 million in <strong>Coffee</strong> Years 2010/11<br />

and 2011/12 respectively. It provides a livelihood to<br />

about 1.32 million households out of the 3.95 million<br />

agricultural households. Government has given coffee<br />

priority in the Ministry of Agriculture, Animal Industry<br />

and Fisheries’ Development Strategy and Investment<br />

Plan (DSIP) as well as the National Export Strategy-NES<br />

(2008-2012) and its corresponding Gender Dimension<br />

of the NES. All these interventions are in line with the<br />

overarching National Development Plan-(NDP (2010/11-<br />

2014/15) envisaged transforming the <strong>Uganda</strong>n economy<br />

from a peasant economy to an industrialized modern one<br />

with a vibrant private sector.<br />

The colonial government, eager to see the development<br />

of cash crop economy, divided the country into agroecological<br />

zones, each specializing in a specific crop:<br />

tobacco in Acholi (Kitgum and Gulu), cotton in West Nile<br />

and coffee in the Central region. In the 1950s extension<br />

workers promoted a coffee-planting programme that<br />

saw coffee production reach 2 million 60kg bags by<br />

the early 1960s and more than 3 million by 1969/1970.<br />

Civil wars during the 1970s affected coffee production<br />

that reduced to about 2 million bags. These were also<br />

exacerbated by the war in Luweero Triangle, a major<br />

coffee region from 1981-1986 (see graph 1).<br />

<strong>Coffee</strong> continues to play a pivotal role<br />

in the <strong>Uganda</strong>n economy contributing<br />

immensely to the export earnings to<br />

the tune of US$ 449 million and US$<br />

393 million in <strong>Coffee</strong> Years 2010/11 and<br />

2011/12 respectively.<br />

50th Anniversary Edition<br />

19

3. Achievements in the <strong>Coffee</strong> Sector<br />

since Independence<br />

i. Cooperative Movement: started in 1913. The<br />

Cooperative movement was very powerful with very<br />

strong cooperative societies and unions: Bugisu<br />

Cooperative Union, Sebei Cooperative Union, West<br />

and East Mengo Cooperative Unions, Wamala<br />

Cooperative Union, Masaka Cooperative Union,<br />

Banyankole Kweterana Cooperative Union, Okoro<br />

Cooperative Union, Busoga Co-operative Union with<br />

coffee as a major commodity marketed. Currently,<br />

it is only Bugisu Cooperative Union and Banyankole<br />

Kweterana Cooperative Union which are still<br />

functional although Masaka Cooperative Union is also<br />

ii.<br />

Chart 1: <strong>Uganda</strong>'s <strong>Coffee</strong> Exports and Value Since Independence<br />

Millions<br />

600<br />

500<br />

400<br />

300<br />

200<br />

100<br />

0<br />

1964/65<br />

1969/70<br />

1974/75<br />

Source: UCDA Database<br />

1979/80<br />

1984/85<br />

rebranding currently;<br />

In 1955, a Price Assistance Fund (PAF) was set up to<br />

cushion farmers against volatility in global coffee<br />

prices. This encouraged farmers to plant more coffee;<br />

iii. <strong>Uganda</strong> Cooperative Alliance was established<br />

in1961 to oversee the operations of the unions and<br />

cooperative societies under them with the ultimate<br />

aim of empowering farmers and their cooperatives to<br />

market their produce profitably and sustainably;<br />

iv. <strong>Coffee</strong> farmers’ welfare changed considerably.<br />

Farmers who sold coffee started constructing iron<br />

sheets roofed and tiled houses especially in Buganda<br />

region, bought motorcycles (Mwanyi Zabala)<br />

, acquisition of more land and marrying more wives!!!<br />

v. There was a Cooperative credit scheme in 1961 (FAO)<br />

administered by Co-operative Department of the<br />

Ministry of Co-operatives and Marketing;<br />

vi. <strong>Uganda</strong> ratified the International <strong>Coffee</strong> Agreement in<br />

1962;<br />

vii. Progressive Farmers Loan Scheme that provided<br />

credit to progressive farmers abandoned in 1964<br />

viii. <strong>Uganda</strong> Census of Agriculture was conducted in<br />

1963/65 and reported that 42% of the farmers in<br />

<strong>Uganda</strong> grew Robusta coffee;<br />

ix. <strong>Coffee</strong> Marketing Board was established in 1959 with<br />

a monopoly control over coffee exports, internal<br />

marketing, quality control, collection of coffee tax<br />

1989/90<br />

<strong>Coffee</strong> Years<br />

Quantity (Million 60 Kilo Bags)<br />

1995/96<br />

1999/00<br />

2004/05<br />

Value in US $ Million<br />

2011/12<br />

5<br />

4<br />

3<br />

2<br />

1<br />

0<br />

Millions<br />

and promoting coffee consumption domestically and<br />

abroad. It was also responsible for implementing the<br />

ICO quota system;<br />

x. The two main functions of CMB were to export coffee<br />

and also to institute a minimum price for coffee<br />

producers at the beginning of each cropping season,<br />

setting marketing margins for private buyers. A<br />

central processing unit was constructed in 1967 with<br />

a capacity of 120 MT/hour;<br />

xi. Government’s diversification plan developed in<br />

1966/67-1970/71;<br />

xii. <strong>Coffee</strong> Rehabilitation Project (CRP) funded by<br />

European Economic Community (EEC) in 1982<br />

aimed at reversing the declining coffee volumes by<br />

improving extension service delivery-pruning for<br />

both Robusta and Arabica and spraying in Arabica<br />

growing regions, coffee nurseries and acquisition of<br />

farm inputs, enhanced processing capacity of hullers<br />

and rehabilitation of agricultural training institutions;<br />

xiii. Farming Systems Support Programme (FSSP), a sequel<br />

of CRP which started in 1991 in 13 districts out of 25<br />

growing coffee then and focused on the coffee farming<br />

system as a whole. FSSP had 2 components: research<br />

and extension. This intervention was envisaged<br />

increasing yield per unit tree/area, improved quality<br />

and release of some land to other crops. FSSP also<br />

had a deliberate strategy of replacing the old nonproductive<br />

trees with the genetically pure and<br />

improved clones propagated by rooted cuttings;<br />

xiv. In 1990, government liberalized the coffee industry as<br />

part of the IMF Social Adjustment programs (SAPs) that<br />

emphasised privatization, liberalization and abolition<br />

of monopoly of marketing boards, CMB inclusive;<br />

xv. Partial release of 7 <strong>Coffee</strong> Wilt Disease Resistant lines<br />

by NARO;<br />

xvi. Replanting Programme under Strategic Export<br />

Programme-Poverty Action Fund (2001-2004);<br />

xvii. Continuous breeding for resistance to pests,<br />

diseases and drought in Robusta and Arabica areas;<br />

xviii. Establishment of Farm Field Schools to disseminate<br />

technologies to farmers;<br />

xix. Establishment of a private tissue culture laboratory<br />

at AGT Buloba to complement the government<br />

laboratory at Kawanda Agricultural Research Institute<br />

(KARI);<br />

xx. Formation of associations in the coffee value chain-<br />

National Union of <strong>Coffee</strong> Agribusinesses and farm<br />

Enterprises (NUCAFE), <strong>Uganda</strong> <strong>Coffee</strong> Farmers Alliance<br />

(UCFA), <strong>Uganda</strong> <strong>Coffee</strong> <strong>Federation</strong> (UCF) to cater for<br />

specific constituents.<br />

xxi. <strong>Coffee</strong> farmers have continued to obtain<br />

about 70% of the export (FOB) price. Farmers’<br />

earnings from coffee rose from UGX. 105 billion<br />

in 2002 to UGX. 777 billion in 2012.<br />

20 50th Anniversary Edition

4. Vision, Mission and, Mandate of<br />

UCDA<br />

UCDA was established in 1991 to develop, regulate and<br />

promote the coffee industry in a liberalized environment.<br />

UCDA’s vision is ‘Making <strong>Uganda</strong> a distinguished producer<br />

of high value coffee’. Its mission is ‘to promote and develop<br />

the coffee industry through provision of clean planting<br />

materials, support to research, quality assurance and<br />

provision of timely market information to stakeholders<br />

and any other matters therein’. It is governed by an industry<br />

based Board of Directors comprising representatives of<br />

farmers, processors, exporters; and one member from<br />

each of the key line ministries - Agriculture, Animal<br />

Industry and Fisheries; Trade, Industry and Cooperatives;<br />

and Finance, Planning and Economic Development. The<br />

Board provides strategic direction of UCDA and also<br />

evaluates Management’s performance of the planned<br />

interventions.<br />

Good governance including corporate social responsibility<br />

(CSR), neutrality, transparency, professionalism, integrity,<br />

accountability to stakeholders and respect for the<br />

environment are values UCDA cherishes passionately.<br />

UCDA has three technical departments and one<br />

service department. The technical ones are: Quality<br />

and Regulatory Services; Production and Strategy and<br />

Business Development and the other, the Finance and<br />

Administration. UCDA is a focal point for all international<br />

coffee matters.<br />

4.1 Objectives<br />

The statutory objectives of the Authority are to:-<br />

1. Promote, improve and monitor marketing of coffee to<br />

optimize foreign exchange and farmers’ earnings;<br />

2. Guarantee that the quality of coffee exports meets<br />

international standards;<br />

3. Develop and promote the coffee and other<br />

related industries through research and extension<br />

arrangements;<br />

4. Promote the marketing of coffee as a value added<br />

product;<br />

5. Promote domestic consumption of <strong>Uganda</strong> coffee;<br />

6. Harmonize activities of coffee sub-sector associations<br />

in line with industry objectives; and<br />

7. Formulate policies related to the coffee industry.<br />

In order to contribute to the President’s Manifesto 2011-<br />

2016, UCDA has undertaken specific programmes to<br />

address production and productivity; marketing and<br />

value addition as well as ensuring an enabling policy and<br />

institutional environment to increase its efficiency and<br />

effectiveness in service delivery.<br />

Among these are: formulation of a draft national coffee<br />

policy, the draft national coffee strategy and revision of the<br />

coffee regulations 1994 to address the rapidly changing<br />

dynamics of the coffee industry both domestically and<br />

globally.<br />

5. Current Projects, policies and<br />

Programmes being undertaken by<br />

UCDA<br />

Projects<br />

• Northern <strong>Uganda</strong> <strong>Coffee</strong> Project;<br />

• Netherlands Trust Fund <strong>Coffee</strong> Project with assistance<br />

from the International Trade Centre;<br />

• Development of Robusta Protocols with assistance<br />

from the <strong>Coffee</strong> Quality Institute, USA;<br />

• Organic <strong>Coffee</strong> Project in South-Western <strong>Uganda</strong><br />

(Kisoro);<br />

• Quality Improvement project with USAID aBi-Trust.<br />

Policies<br />

• Draft National <strong>Coffee</strong> Policy<br />

• Draft National Agricultural Policy<br />

• National Organic Agriculture Policy<br />

• National Trade Policy<br />

Programmes<br />

1. <strong>Coffee</strong> Production Campaign<br />

Under this campaign, exportable production is<br />

envisaged to reach 4.5 m 60-Kilo bags by 2015. This<br />

is hinged on four thematic areas: Research, Extension,<br />

Inputs and credit and Farmer Organisations. District<br />

<strong>Coffee</strong> Platforms and Steering Committees have been<br />

set up oversee the <strong>Coffee</strong> Action Plans.<br />

a. Research<br />

Under research, multiplication of the 7 lines resistant<br />

to coffee wilt disease (CWD) is being undertaken with<br />

propagation through vegetative means (cuttings<br />

and tissue culture). We are currently at the hardening<br />

stage of the coffee seedlings raised from the tissue<br />

culture laboratory at AGT Buloba. Nursery operators<br />

with adequate facilities will be selected to undertake<br />

this important stage in the multiplication after which<br />

the seedlings will be distributed to the farmers.<br />

Breeding for diseases and pests as well as drought<br />

resistance continues to be conducted at <strong>Coffee</strong><br />

Research Institute (COREC) at Kituuza.<br />

50th Anniversary Edition<br />

21

The demand driven approach using the community based<br />

nurseries ensures that farmers raise their seedlings which<br />

are shared out among themselves and a surplus sold.<br />

UCDA provides seed, polypots and technical advice<br />

One of the Community Based Nurseries<br />

Farmers who have adopted the new technologies have<br />

increased their yield per tree from a low of 0.5 kg to<br />

around 7 kg of clean coffee (Kase). Farmers are receiving<br />

a gross income of Shs. 8.64mln per hectare per year for<br />

Robusta and Sh.9.6 ml per year for Arabica.<br />

Through farmer competitions in which application of<br />

agro-inputs is assessed among other parameters, best<br />

farmers have been rewarded with prizes such as spray<br />

pumps, fertilizers, pruning saws, secateurs, solar panels.<br />

This has led to improved husbandry practices.<br />

b. Extension & Technological Transfer<br />

UCDA has continued to implement a Community<br />

Based Nursery (CBN) approach to meet the growing<br />

demand for clean planting materials under the<br />

replanting programme. In this programme farmer<br />

groups receive certified coffee seed and technical<br />

guidance. A total of 1,244 CBNs have been established<br />

with a capacity of generating 20 million seedlings per<br />

year. Local leaders, NAADS and development partners<br />

have been very supportive in this area.<br />

Demo sites in most sub-counties to serve as Farmer<br />

Field Schools (FFS) have been set up at sub county<br />

level through which productivity enhancement<br />

technologies from research centres are passed on to<br />

farmers. This has led to increased productivity and<br />

production.<br />

UCDA continues to offer extension services along<br />

with NAADS, District Agricultural Offices and local<br />

authorities. The leaders do mobilize the farmers,<br />

with special emphasis on special interest groups<br />

– the youth, disabled and women groups. UCDA<br />

has distributed seedlings to these groups as well as<br />

providing technical assistance.<br />

C. Inputs and Credit<br />

In partnership with <strong>Uganda</strong> National Agro-inputs Dealers’<br />

Association (UNADA), over 900 agro-inputs dealers were<br />

trained in proper agro-inputs use. Joint programmes<br />

by district coffee platform ensure that farmers are also<br />

trained in proper use of agro-inputs. The target is to have<br />

at least one agro-inputs dealer in each sub county in the<br />

coffee growing districts.<br />

On availability of credit, a number of farmer associations<br />

have set up savings and credit schemes for ease access to<br />

agro-inputs by members. For examples: Nsangi <strong>Coffee</strong><br />

Farmers Savings and Credit Association; and Paidha<br />

<strong>Coffee</strong> Farmers Association in Wakiso and Nebbi Districts,<br />

respectively.<br />

22 50th Anniversary Edition

a. Farmer Organizations<br />

Collaborating with the National<br />

Union of <strong>Coffee</strong> Agribusinesses<br />

and Farm Enterprises (NUCAFE),<br />

<strong>Uganda</strong> <strong>Coffee</strong> Farmers Alliance<br />

(UCFA), <strong>Uganda</strong> <strong>Coffee</strong> <strong>Federation</strong><br />

(UCF) and other stakeholders,<br />

coffee farmers continue to be<br />

mobilized into viable economic<br />

units. This has invariably eased<br />

provision of extension and<br />

financial services to industry<br />

players, leading to improved<br />

quality and bulk marketing. To<br />

date, 155 farmer association and<br />

1,170 producer organizations<br />

have been established and legally<br />

registered under NUCAFE and<br />

UCFA respectively benefitting<br />

over 200,000 farmers.<br />

Good post harvest handling practices guarantee<br />

quality and better income<br />

2. Sustainable <strong>Coffee</strong> Initiatives<br />

UCDA, in partnership with the private sector, is<br />

seizing the opportunity of the growing demand for<br />

Sustainable <strong>Coffee</strong>s. In the national coffee strategy,<br />

UCDA targets farmers to produce 25% of coffee as<br />

sustainable coffee by 2015. Over 50,000 farmers<br />

have been registered with UCDA to produce coffee<br />

in the various sustainable and specialty initiatives:<br />

Organic, Common Code for <strong>Coffee</strong> Communities<br />

(4Cs), Fair trade, Utz Certified and Rain Forest<br />

Alliance (RFA). Some exporting companies such<br />

as Kyagalanyi <strong>Coffee</strong> Ltd., Ibero (U) Ltd., Kawacom<br />

(U) Ltd, Good African <strong>Coffee</strong>, Gumutindo, and<br />

Kaweri <strong>Coffee</strong> Plantation are working directly with<br />

these farmer groups. Farmers in the Mt. Gorilla<br />

area (Kisoro), selling direct to Urth Caffe, USA<br />

received cattle; pulpers, water tanks, drying trays<br />

and tarpaulins to improve quality. These coffees<br />

attract a price of around $ 300 per tonne over the<br />

conventional market.<br />

3. <strong>Coffee</strong> Production in Northern<br />

<strong>Uganda</strong><br />

A Special Intervention Programme for commercial<br />

coffee production in the districts of Acholi and<br />

Lango was developed. Close to 400 farmers in<br />

23 sub-counties have planted around 500,000<br />

coffee trees, intercropped with bananas to ensure<br />

household food security. UCDA gives farmers<br />

coffee seedlings, banana suckers and shade tree<br />

seedlings.<br />

Robusta dry cherries<br />

(Kiboko)<br />

FAQ – Kase<br />

Farmers adding value and shifting from selling dry<br />

cherries to selling Fair Average Quality (Kase)<br />

4. Quality Improvement and Value addition<br />

Value addition at farm-gate is being undertaken through<br />

promotion of wet processing in Arabica and Robusta<br />

coffees, a practice that has greatly improved quality and<br />

returns to farmers.<br />

To promote domestic coffee consumption, UCDA has<br />

partnered with the private sector to come up with<br />

<strong>Uganda</strong>n coffee brands that occupy shelf-space in major<br />

supermarkets in the city and towns. The favourable<br />

investment climate prevailing in the country has indeed<br />

attracted investment in Cafes, Restaurants and Hotels<br />

where out-of-home coffees are served.<br />

UCDA, in partnership with the private<br />

sector, is seizing the opportunity of the<br />

growing demand for Sustainable <strong>Coffee</strong>s.<br />

In the national coffee strategy, UCDA<br />

targets farmers to produce 25% of coffee<br />

as sustainable coffee by 2015.<br />

50th Anniversary Edition<br />

23

A variety of choice of <strong>Uganda</strong>n coffee brands<br />

5. Provision of timely market information<br />

This is done on daily, monthly and annual basis<br />

reflecting the performance of the domestic and<br />

global coffee markets through the website (www.<br />

ugandacoffee.org), radio programmes and mobile<br />

phones (SMS-7197).<br />

6. Enforcement of <strong>Coffee</strong> Regulations<br />

This is being done in collaboration with other<br />

stakeholders such as the Police and Local authorities.<br />

To ensure that coffee exported meets international<br />

standards, all coffee lots undergo quality inspection<br />

and certification.<br />

7. Development of Robusta Protocols<br />

To enhance <strong>Uganda</strong>’s Robusta as a unique origin,<br />

protocols have been developed for Robusta to<br />

compete favourably in the Specialty segments of the<br />

market. This will boost <strong>Uganda</strong>’s export revenue and<br />

more importantly, farmers’incomes.<br />

Conclusion<br />

Overall the importance of coffee to the <strong>Uganda</strong>n<br />

economy cannot be over-estimated and its priority in<br />

all Government’s policies and interventions is clear. Its<br />

strategic position as a poverty reduction enterprise<br />

contributes significantly towards not only to the first<br />

UNDP’s millennium development goal but also the third,<br />

seventh and eighth goals which deal with gender equality<br />

and women empowerment; environmental sustainability;<br />

and overseas development assistance respectively. From<br />

the above outlook, UCDA programmes are geared towards<br />

value addition along the coffee value chain to make it<br />

more competitive both nationally and internationally.<br />

It also acknowledges different stakeholders including<br />

development partners whose interventions in different<br />

areas along the coffee value chain with appreciable<br />

investments in the coffee industry in <strong>Uganda</strong>.<br />

Physical Address<br />

<strong>Uganda</strong> <strong>Coffee</strong> Development Authority<br />

<strong>Coffee</strong> House, Plot 35 Jinja Road<br />

P.O. Box 7267, Kampala<br />

General Line Tel: 256-414-256940/233073<br />

256-031-2260470<br />

Fax: 256-414-232912/414256994<br />

Website: www.ugandacoffee.org<br />

24 50th Anniversary Edition

Plot 2219/2377, Bweyogerere, P.O.Box 14625, Kampala,<strong>Uganda</strong><br />

Tel. +256 (0) 312 202425/6, Fax. +256 (0) 414 285684<br />

www.armajarotrading.com<br />

50th Anniversary Edition<br />

25

Word from the MD Ugacof<br />

I<br />

am extremely honored to be part of this edition of<br />

the coffee year book. It’s an honor in a sense that<br />

throughout the industry I find this publication very<br />

insightful and informative. Congratulations to the<br />

editorial !<br />

I bring you warm greetings and Happy New Year<br />

wishes from Ugacof directors, members of staff and<br />

our business partners. it’s the combined efforts of<br />

this strong team at UCF that our company continues to play an important role in the industry.<br />

The just concluded year was exciting and challenging in many respects, but I will restrict my<br />

observations to just two prominent exciting developments as we collectively ponder in an effort<br />

to overcome the challenges. The first and fore most was relative stability of the prices in the local<br />

market which directly benefits the first tier stakeholder (The farmer). It’s a common consensus that<br />

when a farmer has a smile it translates to the industry performance.<br />

The second observation is the energized efforts to embrace the research. It was refreshing at the<br />

previous coffee day at Kituza research centre to hear the impassioned vigor of players about this vital<br />

aspect of ensuring crop sustainability.<br />

We at Ugacof continue to walk our vision and mission which are geared at working with foot soldier<br />

(<strong>Uganda</strong>n coffee farmer) on the small farm and to ensure we keep holding the mantle high up as<br />

East Africa’s model in the coffee trade. We are currently working with over 10,000 farmers in our<br />

Kinoni, Masaka and Iganga areas. We are in the final stages to engage more farmers in the districts of<br />

Kamuli,Buikwe and Kayunga.<br />

Ugacof is a trend setter in improving processing technology. We have invested in new processing<br />

machines and Robusta washing stations in different parts of the country. We are confident that such<br />

efforts will raise the bar and set the trends in attaining high quality <strong>Coffee</strong> in the region. I need to<br />

add our gratitude to the UCDA and other stakeholders in the sector for consolidating efforts towards<br />

quantity and quality improvement.<br />

Ugacof predicts a brighter future for <strong>Uganda</strong>’s coffee sector and we are very much committed in<br />

maintaining both our presence and partnerships for a better coffee sector and <strong>Uganda</strong> . Enjoy the<br />

new season.<br />

Kailash Natani.<br />

26 50th Anniversary Edition

aBi Trust and <strong>Coffee</strong> Value Chain<br />

Development in <strong>Uganda</strong><br />

The aBi Trust strategy supports market driven<br />

enterprises using a value chain approach<br />

for specific commodity groups. Through a<br />

value chain analysis, opportunities, constraints<br />

and actors are identified to improve efficiency,<br />

effectiveness and competitiveness through<br />

technical and financial support.<br />

aBi Trust develops the <strong>Coffee</strong> value chain at three<br />

specific levels namely Global focus, National focus,<br />

and Partners (specific interventions through<br />

partners).<br />

Globally, aBi Trust in collaboration with <strong>Uganda</strong><br />

<strong>Coffee</strong> Development Authority (UCDA) supports<br />

the development, differentiation and validation of<br />

protocols for speciality coffee. Since <strong>Uganda</strong> is the<br />

birthplace of Fine Robusta coffee, our support to<br />

the <strong>Coffee</strong> Quality Institute (CQI) in collaboration<br />

with UCDA has developed and validated grading<br />

and cupping protocols. Robusta coffee can now<br />

be traded as a speciality coffee (Fine Robusta).<br />

The Trust facilitates the enabling environment at<br />

the National level through support to different<br />

institutions and fora; through Café Africa, the<br />

National <strong>Coffee</strong> Steering Committee (NCSC) is<br />

supported to address and devise strategies for the<br />

coffee sector development.<br />

In collaboration with the Ministry of Agriculture,<br />

Animal Industry and Fisheries (MAAIF) and UCDA<br />

taking lead, a National <strong>Coffee</strong> Policy has been<br />

developed. Support has been extended to the<br />

<strong>Uganda</strong> <strong>Coffee</strong> <strong>Federation</strong> (UCF) to develop its<br />

strategy; <strong>Uganda</strong> National Bureau of Standards<br />

(UNBS) through collaboration with UCDA is<br />

developing the code of practice to pursue OTA<br />

challenges. Developing and validating cupping<br />

and grading protocols and profiling of <strong>Uganda</strong>’s<br />

coffee is underway.<br />

The current <strong>Coffee</strong> extension material is under<br />

review to suit the changing trends in collaboration<br />

with UCDA. Funds have been committed on<br />

the National Enquiry Point (NEP) and Centre of<br />

Excellence (CoE) as our areas of focus.<br />

50th Anniversary Edition<br />

27

National Organic Movement of <strong>Uganda</strong><br />

(NOGAMU) was supported in collaboration<br />

with HIVOS to develop Production Manuals<br />

for Organic Robusta and Arabica growing<br />

systems in <strong>Uganda</strong>.<br />

aBi Trust through Implementing Partners<br />

(IPs) supports several interventions which<br />

will result in increased incomes and<br />

employment.<br />

The IPs are usually Farmers Organisations<br />

(FOs), Enterprises (including small,<br />

medium and large) and Business<br />

Development Services (BDS) providers.<br />

The Trust facilitates market access mainly<br />

through certifications for sustainability<br />

(4C, UTZ, RFA and Organic among others)<br />

and speciality coffees including Q and R<br />

fine coffees.<br />

Over 10 central washing stations<br />

mainly eco-pulpers and several hulling<br />

facilities have been supported under<br />

value addition. Addressing productivity<br />

enhancement, Good Agricultural Practices<br />

are promoted through support to farmer<br />

field demonstrations, and nurseries for<br />

clean planting materials. In collaboration<br />

with UCDA, 18 nurseries have been<br />

supported to multiply the CWD-r material<br />

and through IPs directly to make planting<br />

material affordable and accessible.<br />

The main focus is establishing mother<br />

gardens and nurseries for both Elite and<br />

Clonal coffee seedlings. Through a costshare<br />

grant with Royal Plant Nurseries,<br />

the Trust is facilitating tissue culture<br />

technology and weaning/hardening. At<br />

the nurseries aBi is promoting shade tree<br />

seedlings production under our Green<br />

Growth initiative because Climate Change<br />

is negatively impacting coffee production.<br />

Post-harvest technologies that include drying sheets,<br />

poly tunnels, GrainPro® products and washing stations<br />

for Arabica and Robusta are being promoted among<br />

farmers.<br />

In <strong>Uganda</strong>, collateral requirements pose a challenge<br />

for the agricultural sector participants who try to<br />

source funding for the different activities along the<br />

value chain. aBi established board guarantees to<br />

help address the issue of lack of collateral and to help<br />

deepen financial services through loan guarantee<br />

schemes and lines of credit.<br />

These services are undertaken by financial institutions<br />

that have at least a 3% loan portfolio with agribusiness<br />

and a rural outreach network, among other<br />

requirements. Enterprises including those along the<br />

coffee value chain can access services from these<br />

banks.<br />

Through financial services, many rural financial<br />

institutions like Opportunity <strong>Uganda</strong>, CRDB,<br />

HOFOKAM, and several SACCOs have received support<br />

from the Trust to reach farmers.<br />

At the producer level, Village Savings and Loan<br />

Associations (VSLAs) are supported to harness<br />

financial discipline and cohesion among groups which<br />

make adoption of other interventions easier.<br />

Gender for Growth (G4G) uses the household<br />

approach through Farming as a Family Business<br />

(FaaFB) to improve the livelihoods of farmers. Many<br />

families have improved their incomes through vision<br />

setting and joint planning.<br />

Over 10 central washing<br />

stations mainly eco-pulpers<br />

and several hulling facilities<br />

have been supported under<br />

value addition. Addressing<br />

productivity enhancement, Good<br />

Agricultural Practices are promoted<br />

through support to farmer field<br />

demonstrations, and nurseries for<br />

clean planting materials.<br />

28 50th Anniversary Edition

Kawacom, the <strong>Uganda</strong>n subsidiary of the ECOM<br />

Group, was founded in 1996 and has been at the<br />

forefront of <strong>Uganda</strong>’s coffee export trade for 17<br />