Inventory count checklist

Inventory count checklist

Inventory count checklist

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

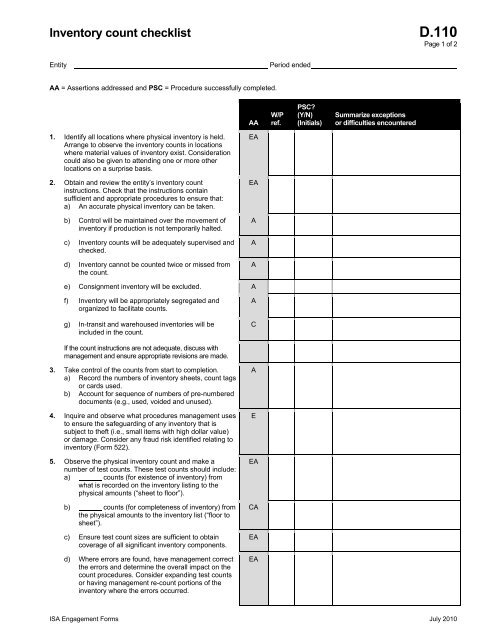

<strong>Inventory</strong> <strong>count</strong> <strong>checklist</strong> D.110<br />

Page 1 of 2<br />

Entity<br />

Period ended<br />

AA = Assertions addressed and PSC = Procedure successfully completed.<br />

AA<br />

W/P<br />

ref.<br />

PSC<br />

(Y/N)<br />

(Initials)<br />

Summarize exceptions<br />

or difficulties en<strong>count</strong>ered<br />

1. Identify all locations where physical inventory is held.<br />

Arrange to observe the inventory <strong>count</strong>s in locations<br />

where material values of inventory exist. Consideration<br />

could also be given to attending one or more other<br />

locations on a surprise basis.<br />

2. Obtain and review the entity’s inventory <strong>count</strong><br />

instructions. Check that the instructions contain<br />

sufficient and appropriate procedures to ensure that:<br />

a) An accurate physical inventory can be taken.<br />

b) Control will be maintained over the movement of<br />

inventory if production is not temporarily halted.<br />

c) <strong>Inventory</strong> <strong>count</strong>s will be adequately supervised and<br />

checked.<br />

d) <strong>Inventory</strong> cannot be <strong>count</strong>ed twice or missed from<br />

the <strong>count</strong>.<br />

EA<br />

EA<br />

A<br />

A<br />

A<br />

e) Consignment inventory will be excluded. A<br />

f) <strong>Inventory</strong> will be appropriately segregated and<br />

organized to facilitate <strong>count</strong>s.<br />

g) In-transit and warehoused inventories will be<br />

included in the <strong>count</strong>.<br />

A<br />

C<br />

If the <strong>count</strong> instructions are not adequate, discuss with<br />

management and ensure appropriate revisions are made.<br />

3. Take control of the <strong>count</strong>s from start to completion.<br />

a) Record the numbers of inventory sheets, <strong>count</strong> tags<br />

or cards used.<br />

b) Ac<strong>count</strong> for sequence of numbers of pre-numbered<br />

documents (e.g., used, voided and unused).<br />

4. Inquire and observe what procedures management uses<br />

to ensure the safeguarding of any inventory that is<br />

subject to theft (i.e., small items with high dollar value)<br />

or damage. Consider any fraud risk identified relating to<br />

inventory (Form 522).<br />

5. Observe the physical inventory <strong>count</strong> and make a<br />

number of test <strong>count</strong>s. These test <strong>count</strong>s should include:<br />

a) <strong>count</strong>s (for existence of inventory) from<br />

what is recorded on the inventory listing to the<br />

physical amounts (“sheet to floor”).<br />

b) <strong>count</strong>s (for completeness of inventory) from<br />

the physical amounts to the inventory list (“floor to<br />

sheet”).<br />

c) Ensure test <strong>count</strong> sizes are sufficient to obtain<br />

coverage of all significant inventory components.<br />

d) Where errors are found, have management correct<br />

the errors and determine the overall impact on the<br />

<strong>count</strong> procedures. Consider expanding test <strong>count</strong>s<br />

or having management re-<strong>count</strong> portions of the<br />

inventory where the errors occurred.<br />

A<br />

E<br />

EA<br />

CA<br />

EA<br />

EA<br />

ISA Engagement Forms July 2010

<strong>Inventory</strong> <strong>count</strong> <strong>checklist</strong> D.110<br />

Page 2 of 2<br />

AA<br />

W/P<br />

ref.<br />

PSC<br />

(Y/N)<br />

(Initials)<br />

Summarize exceptions<br />

or difficulties en<strong>count</strong>ered<br />

6. Agree the test <strong>count</strong>s to:<br />

a) Perpetual inventory records. EA<br />

b) Entity’s final inventory listing. CEA<br />

A<br />

Investigate discrepancies and, if necessary, ensure<br />

proper adjustments are made.<br />

7. Review management’s cut-off procedures, as at the<br />

<strong>count</strong> date, for both the physical inventory and<br />

ac<strong>count</strong>ing records and ensure they are adequate.<br />

8. Record details of relevant cut-off information (dates and<br />

particulars of most recent receiving reports, and most<br />

recent shipping memoranda) at the time of physical<br />

<strong>count</strong>.<br />

9. Inquire with a responsible staff member about inventory<br />

that is slow-moving or obsolete.<br />

10. Review the perpetual records for indications of slowmoving<br />

and obsolete stock.<br />

11. Tour the facility where inventory is being held and look<br />

for signs that items may be obsolete or slow-moving<br />

(i.e., damaged, dusty, etc.).<br />

12. Tour premises at close of <strong>count</strong> and ensure all items are<br />

<strong>count</strong>ed (i.e., tagged).<br />

13. Prepare memorandum on the results of the <strong>count</strong> and<br />

any matters to be followed up later in the audit.<br />

CA<br />

A<br />

V<br />

V<br />

V<br />

C<br />

A<br />

Prepared by Date Reviewed by Date<br />

ISA Engagement Forms July 2010