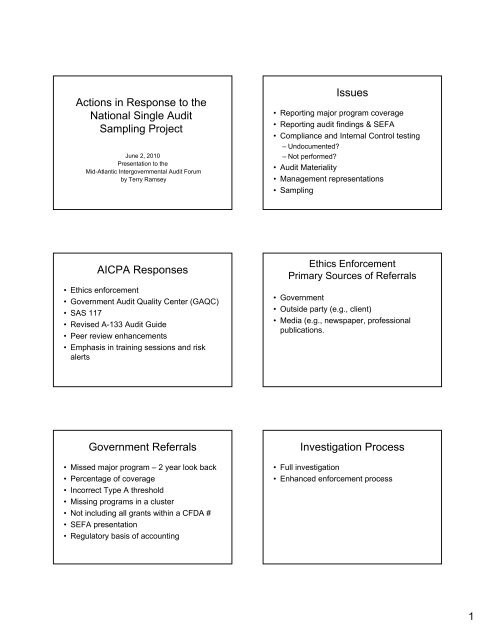

Actions in Response to the National Single Audit Sampling Project ...

Actions in Response to the National Single Audit Sampling Project ...

Actions in Response to the National Single Audit Sampling Project ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Actions</strong> <strong>in</strong> <strong>Response</strong> <strong>to</strong> <strong>the</strong><br />

<strong>National</strong> S<strong>in</strong>gle <strong>Audit</strong><br />

Sampl<strong>in</strong>g <strong>Project</strong><br />

June 2, 2010<br />

Presentation <strong>to</strong> <strong>the</strong><br />

Mid-Atlantic Intergovernmental <strong>Audit</strong> Forum<br />

by Terry Ramsey<br />

Issues<br />

• Report<strong>in</strong>g major program coverage<br />

• Report<strong>in</strong>g audit f<strong>in</strong>d<strong>in</strong>gs & SEFA<br />

• Compliance and Internal Control test<strong>in</strong>g<br />

– Undocumented<br />

– Not performed<br />

• <strong>Audit</strong> Materiality<br />

• Management representations<br />

•Sampl<strong>in</strong>g<br />

AICPA <strong>Response</strong>s<br />

• Ethics enforcement<br />

• Government <strong>Audit</strong> Quality Center (GAQC)<br />

• SAS 117<br />

• Revised A-133 <strong>Audit</strong> Guide<br />

• Peer review enhancements<br />

• Emphasis <strong>in</strong> tra<strong>in</strong><strong>in</strong>g sessions and risk<br />

alerts<br />

Ethics Enforcement<br />

Primary Sources of Referrals<br />

• Government<br />

• Outside party (e.g., client)<br />

• Media (e.g., newspaper, professional<br />

publications.<br />

Government Referrals<br />

• Missed major program – 2 year look back<br />

• Percentage of coverage<br />

• Incorrect Type A threshold<br />

• Miss<strong>in</strong>g programs <strong>in</strong> a cluster<br />

• Not <strong>in</strong>clud<strong>in</strong>g all grants with<strong>in</strong> a CFDA #<br />

• SEFA presentation<br />

• Regula<strong>to</strong>ry basis of account<strong>in</strong>g<br />

Investigation Process<br />

• Full <strong>in</strong>vestigation<br />

• Enhanced enforcement process<br />

1

Full Investigation<br />

• F<strong>in</strong>ancial statements<br />

• Work papers<br />

• Not restricted <strong>to</strong> referral compla<strong>in</strong>t<br />

• Time consum<strong>in</strong>g and done less frequently<br />

Enhanced Enforcement<br />

• Correspondence<br />

• F<strong>in</strong>ancial statements<br />

• Word<strong>in</strong>g papers on a limited basis<br />

• Not restricted <strong>to</strong> referral compliant<br />

• A-133/Yellow Book<br />

• SEFA Issues<br />

• Report<strong>in</strong>g Issues<br />

• Disclosure Issues<br />

• Account<strong>in</strong>g Issues<br />

F<strong>in</strong>d<strong>in</strong>gs<br />

Sanctions Available<br />

• No fur<strong>the</strong>r action or NFA with comments<br />

• Required Corrective Action<br />

–CPE<br />

– GAQC membership<br />

– Restrictions - Peer review & teach<strong>in</strong>g<br />

– Work product follow-up (immediate or<br />

subsequent<br />

– Pre-issuance reviews<br />

• Membership rights/publications<br />

RCA –Remediate 55%<br />

Trial Board or Settlement Agreement – Remediate & 12%<br />

discipl<strong>in</strong>e<br />

No fur<strong>the</strong>r action taken (violations not material or self 17%<br />

remediated)<br />

<strong>Audit</strong> submitted for review <strong>to</strong> comply with<br />

12%<br />

remediation imposed – complied with standards<br />

O<strong>the</strong>r 4%<br />

Total 100%<br />

2

GAQC<br />

• Firms<br />

– Designated partner<br />

– Peer review by ano<strong>the</strong>r GAQC firm<br />

• Cont<strong>in</strong>uous learn<strong>in</strong>g<br />

–Alerts<br />

– Newsletter<br />

– Conference calls<br />

– Web based events<br />

GAQC Resources<br />

• GAQC Web site (www.aicpa.org/GAQC)<br />

• Recovery Act Resource Center<br />

– GAQC Web site for audi<strong>to</strong>rs dedicated <strong>to</strong> Recovery Act matters<br />

– Archived GAQC member events<br />

• Recovery Act events<br />

• <strong>Audit</strong>ee call on prepar<strong>in</strong>g for a s<strong>in</strong>gle audit<br />

– L<strong>in</strong>ks <strong>to</strong> Recovery Act GAQC Alerts<br />

– L<strong>in</strong>ks <strong>to</strong> GAQC Recovery Act <strong>to</strong>ols<br />

– The Resource Center is open <strong>to</strong> general public<br />

– Encourage clients <strong>to</strong> visit<br />

• HUD <strong>in</strong>formation page<br />

GAQC Membership<br />

• Over 1,350 member firms represent<strong>in</strong>g 50<br />

states, Puer<strong>to</strong> Rico, and US Virg<strong>in</strong> Islands<br />

• AICPA Board approved State <strong>Audit</strong><br />

Organizations (SAO) as members – 15<br />

have jo<strong>in</strong>ed <strong>to</strong> date<br />

• RI, VA, ND, SD, NH, VT, UT, MI, OH, GA, LA, DE,<br />

FL, MN, TX<br />

SAS 117 – Compliance <strong>Audit</strong>s<br />

• Issued December 2009<br />

• Effective fiscal periods end<strong>in</strong>g on or after<br />

June 15, 2010.<br />

• Supersedes SAS 74<br />

• Uses new clarity format<br />

• Focused on address<strong>in</strong>g NSAS project<br />

recommendations<br />

• Elevates material from guide <strong>to</strong> standard<br />

Applicability of O<strong>the</strong>r SAS<br />

• Clarifies that all AU sections applicable<br />

unless specifically excluded (4-6)<br />

• Adapt and apply SAS <strong>in</strong> a compliance<br />

audit, e.g., by replac<strong>in</strong>g <strong>the</strong> word<br />

misstatement with <strong>the</strong> word<br />

noncompliance<br />

Terms<br />

• Applicable compliance requirements<br />

• Governmental audit requirement (GAR)<br />

3

<strong>Audit</strong> Objectives (10)<br />

• Obta<strong>in</strong> sufficient appropriate evidence<br />

• Form op<strong>in</strong>ion at level required by GAR<br />

• Identify audit report<strong>in</strong>g requirements<br />

specified <strong>in</strong> GAR that are supplementary<br />

<strong>to</strong> GAGAS.<br />

<strong>Audit</strong> Procedures<br />

• Risk assessment procedures, tests of controls,<br />

and analytical procedures alone are not<br />

sufficient <strong>to</strong> address a risk of material noncompliance<br />

(19)<br />

• The use of analytical procedures <strong>to</strong> ga<strong>the</strong>r<br />

substantive evidence is generally less effective<br />

<strong>in</strong> a compliance audit than a f<strong>in</strong>ancial statement<br />

audit (A23)<br />

• References A-133 requirement <strong>to</strong> test I/C even if<br />

such test<strong>in</strong>g would be <strong>in</strong>efficient (A25)<br />

Documentation<br />

• Risk assessment procedures (39 & A38)<br />

• Procedures performed <strong>to</strong> test I/C &<br />

compliance (40)<br />

• Materiality levels and how determ<strong>in</strong>ed (41)<br />

• How complied with GAR (42)<br />

Management Representations (23)<br />

• Required by standard<br />

• Elements specifically enumerated<br />

Material Noncompliance<br />

• Failure <strong>to</strong> follow or violation of compliance<br />

requirements that results <strong>in</strong> noncompliance<br />

that is:<br />

– Quantitatively or qualitatively material<br />

– Ei<strong>the</strong>r <strong>in</strong>dividually or when aggregated with<br />

o<strong>the</strong>r non-compliance<br />

<strong>Audit</strong> F<strong>in</strong>d<strong>in</strong>gs<br />

• Materiality evaluation (29)<br />

– Known questioned costs<br />

– Likely questioned costs<br />

– O<strong>the</strong>r material noncompliance that by its<br />

nature may not result <strong>in</strong> questioned costs<br />

• Likely QC def<strong>in</strong>ed (11)<br />

– Developed by extrapolat<strong>in</strong>g from audit<br />

evidence, e.g., project<strong>in</strong>g known QC <strong>to</strong><br />

population.<br />

4

Report<strong>in</strong>g of Major Programs<br />

• In 2008 FAC revised on-l<strong>in</strong>e submission<br />

screens <strong>to</strong> alert audi<strong>to</strong>rs of importance of<br />

identify<strong>in</strong>g major programs both <strong>in</strong> <strong>the</strong><br />

SEFA and <strong>the</strong> SF-SAC<br />

• Reference <strong>to</strong> separate schedule <strong>in</strong>clud<strong>in</strong>g<br />

major programs is a required report<strong>in</strong>g<br />

element (30.a)<br />

Reissuance of Compliance Report (43)<br />

• Explana<strong>to</strong>ry paragraph<br />

– Replac<strong>in</strong>g previously issued report<br />

– Reasons why reissued<br />

– Changes<br />

•Dat<strong>in</strong>g<br />

• Reissuance audi<strong>to</strong>r pepared document is<br />

considered reissuance of report, e.g.:<br />

– Schedule of F<strong>in</strong>d<strong>in</strong>gs and Question Costs.<br />

<strong>National</strong> Sampl<strong>in</strong>g <strong>Project</strong> Found<br />

• The number of items tested varied widely<br />

for audits of comparable entities (size,<br />

programs, risks, <strong>in</strong>ternal control<br />

assessments) <strong>in</strong>volv<strong>in</strong>g <strong>the</strong> same<br />

sampl<strong>in</strong>g parameters.<br />

• <strong>Audit</strong> test<strong>in</strong>g not documented.<br />

A-133 <strong>Audit</strong> Guide<br />

Chapter 11 - Sampl<strong>in</strong>g<br />

• Statistical and judgmental sample sizes should<br />

be comparable. (AU 350.23 – SAS 111 12/06))<br />

• Sample must <strong>in</strong>clude transactions from all major<br />

programs (11.42)<br />

– Preferable <strong>to</strong> select separate samples for each major<br />

program (11.43)<br />

• Evaluate dual purpose tests (I/C & Compliance)<br />

separately for f<strong>in</strong>d<strong>in</strong>gs (11.54)<br />

• Suggested m<strong>in</strong>imum sample sizes (11.59)<br />

M<strong>in</strong>imum samples for populations >250 –<br />

COMPLIANCE<br />

Desired Level of<br />

Assurance (Rema<strong>in</strong><strong>in</strong>g<br />

Risk of Material<br />

Noncompliance)<br />

Sample Sizes<br />

M<strong>in</strong>imum Sample Size<br />

High 60<br />

Moderate 40<br />

Low 25<br />

29<br />

Document<strong>in</strong>g sampl<strong>in</strong>g (11.134)<br />

• Control or compliance tested<br />

• Def<strong>in</strong>ition of population<br />

• Def<strong>in</strong>ition of deviation<br />

• Desired confidence level, <strong>to</strong>lerable<br />

deviation rate, and expected deviation rate<br />

• Sample size<br />

• Sample selection method<br />

5

Document<strong>in</strong>g sampl<strong>in</strong>g (11.134)<br />

• Selected items<br />

• Evaluation of sample<br />

– Number deviations<br />

– Qualitative fac<strong>to</strong>rs of <strong>the</strong> deviations<br />

– <strong>Project</strong>ed deviation rate<br />

– Effects on o<strong>the</strong>r audit procedures<br />

– Determ<strong>in</strong>ation of known and likely QC<br />

– Whe<strong>the</strong>r deviations result <strong>in</strong> op<strong>in</strong>ion modification or<br />

f<strong>in</strong>d<strong>in</strong>g & if not how audi<strong>to</strong>r considered sampl<strong>in</strong>g risk.<br />

• Overall conclusion<br />

SEFA<br />

• Clarify<strong>in</strong>g guidance added <strong>to</strong> 2008<br />

GAS/A133 Guide<br />

• SEFA Practice Aids (both for <strong>the</strong> audi<strong>to</strong>r<br />

and auditee) issued and available on <strong>the</strong><br />

GAQC Web site, under <strong>the</strong> Resources tab<br />

(under “Research Tools and Aids”) and also<br />

<strong>in</strong>corporated <strong>in</strong> <strong>the</strong> GAS/A133 Guide<br />

– <strong>Audit</strong> Program and Disclosure Checklist for Audi<strong>to</strong>rs<br />

– Document for auditees <strong>to</strong> accumulate important <strong>in</strong>formation on<br />

federal awards and a Disclosure Checklist for <strong>Audit</strong>ees<br />

Peer Review<br />

• In response <strong>to</strong> <strong>the</strong> PCIE Report <strong>the</strong> AICPA created <strong>the</strong><br />

Practice Moni<strong>to</strong>r<strong>in</strong>g Task Force.<br />

– Areas of Focus:<br />

• Establish consistent measures of A-133 deficiencies<br />

• Develop guidance and tra<strong>in</strong><strong>in</strong>g materials for peer reviewers<br />

• Interpretation 63-1a ensures A-133 engagement selection<br />

− Effective for peer reviews commenc<strong>in</strong>g on or after September 1, 2009<br />

• Peer review checklists modified <strong>to</strong> focus peer reviews of<br />

s<strong>in</strong>gle audits on areas known <strong>to</strong> be problematic<br />

6