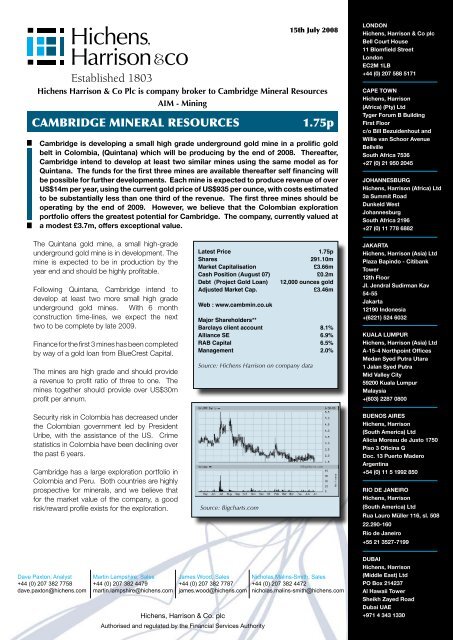

cambridge mineral resources 1.75p - Minesite

cambridge mineral resources 1.75p - Minesite

cambridge mineral resources 1.75p - Minesite

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

15th July 2008<br />

Hichens Harrison & Co Plc is company broker to Cambridge Mineral Resources<br />

AIM - Mining<br />

<strong>cambridge</strong> <strong>mineral</strong> <strong>resources</strong> <strong>1.75p</strong><br />

Cambridge is developing a small high grade underground gold mine in a prolific gold<br />

belt in Colombia, (Quintana) which will be producing by the end of 2008. Thereafter,<br />

Cambridge intend to develop at least two similar mines using the same model as for<br />

Quintana. The funds for the first three mines are available thereafter self financing will<br />

be possible for further developments. Each mine is expected to produce revenue of over<br />

US$14m per year, using the current gold price of US$935 per ounce, with costs estimated<br />

to be substantially less than one third of the revenue. The first three mines should be<br />

operating by the end of 2009. However, we believe that the Colombian exploration<br />

portfolio offers the greatest potential for Cambridge. The company, currently valued at<br />

a modest £3.7m, offers exceptional value.<br />

London<br />

Hichens, Harrison & Co plc<br />

Bell Court House<br />

11 Blomfield Street<br />

London<br />

EC2M 1LB<br />

+44 (0) 207 588 5171<br />

Cape Town<br />

Hichens, Harrison<br />

(Africa) (Pty) Ltd<br />

Tyger Forum B Building<br />

First Floor<br />

c/o Bill Bezuidenhout and<br />

Willie van Schoor Avenue<br />

Bellville<br />

South Africa 7536<br />

+27 (0) 21 950 2045<br />

Johannesburg<br />

Hichens, Harrison (Africa) Ltd<br />

3a Summit Road<br />

Dunkeld West<br />

Johannesburg<br />

South Africa 2196<br />

+27 (0) 11 778 6882<br />

The Quintana gold mine, a small high-grade<br />

underground gold mine is in development. The<br />

mine is expected to be in production by the<br />

year end and should be highly profitable.<br />

Following Quintana, Cambridge intend to<br />

develop at least two more small high grade<br />

underground gold mines. With 6 month<br />

construction time-lines, we expect the next<br />

two to be complete by late 2009.<br />

Finance for the first 3 mines has been completed<br />

by way of a gold loan from BlueCrest Capital.<br />

The mines are high grade and should provide<br />

a revenue to profit ratio of three to one. The<br />

mines together should provide over US$30m<br />

profit per annum.<br />

Security risk in Colombia has decreased under<br />

the Colombian government led by President<br />

Uribe, with the assistance of the US. Crime<br />

statistics in Colombia have been declining over<br />

the past 6 years.<br />

Cambridge has a large exploration portfolio in<br />

Colombia and Peru. Both countries are highly<br />

prospective for <strong>mineral</strong>s, and we believe that<br />

for the market value of the company, a good<br />

risk/reward profile exists for the exploration.<br />

Latest Price <strong>1.75p</strong><br />

Shares 291.10m<br />

Market Capitalisation<br />

£3.66m<br />

Cash Position (August 07)<br />

£0.2m<br />

Debt (Project Gold Loan) 12,000 ounces gold<br />

Adjusted Market Cap.<br />

£3.46m<br />

Web : www.cambmin.co.uk<br />

Major Shareholders**<br />

Barclays client account 8.1%<br />

Alliance SE 6.9%<br />

RAB Capital 6.5%<br />

Management 2.0%<br />

Source: Hichens Harrison on company data<br />

Source: Bigcharts.com<br />

Jakarta<br />

Hichens, Harrison (Asia) Ltd<br />

Plaza Bapindo - Citibank<br />

Tower<br />

12th Floor<br />

Jl. Jendral Sudirman Kav<br />

54-55<br />

Jakarta<br />

12190 Indonesia<br />

+(6221) 524 6032<br />

Kuala Lumpur<br />

Hichens, Harrison (Asia) Ltd<br />

A-15-4 Northpoint Offices<br />

Medan Syed Putra Utara<br />

1 Jalan Syed Putra<br />

Mid Valley City<br />

59200 Kuala Lumpur<br />

Malaysia<br />

+(603) 2287 0800<br />

BUENOS AIRES<br />

Hichens, Harrison<br />

(South America) Ltd<br />

Alicia Moreau de Justo 1750<br />

Piso 3 Oficina G<br />

Doc. 13 Puerto Madero<br />

Argentina<br />

+54 (0) 11 5 1992 850<br />

RIO DE JANEIRO<br />

Hichens, Harrison<br />

(South America) Ltd<br />

Rua Lauro Müller 116, sl. 508<br />

22.290-160<br />

Rio de Janeiro<br />

+55 21 3527-7199<br />

Dave Paxton, Analyst<br />

+44 (0) 207 382 7758<br />

dave.paxton@hichens.com<br />

Martin Lampshire, Sales<br />

+44 (0) 207 382 4479<br />

martin.lampshire@hichens.com<br />

James Wood, Sales<br />

+44 (0) 207 382 7787<br />

james.wood@hichens.com<br />

Hichens, Harrison & Co. plc<br />

Authorised and regulated by the Financial Services Authority<br />

Nicholas Malins-Smith, Sales<br />

+44 (0) 207 382 4472<br />

nicholas.malins-smith@hichens.com<br />

dubai<br />

Hichens, Harrison<br />

(Middle East) Ltd<br />

PO Box 214237<br />

Al Hawaii Tower<br />

Sheikh Zayed Road<br />

Dubai UAE<br />

+971 4 343 1330

Introduction<br />

Cambridge Mineral Resources (CMR) is developing a number of small underground<br />

gold mines, mining high-grade veins in Colombia. Construction of the first mine<br />

Quintina is underway and production is expected in the final quarter of this year.<br />

Once Quintina is in operation a second mine will be developed. Colombia has a<br />

history as a large gold producer. There are a large number of local small gold mines,<br />

mining high grade underground veins. Funding for these projects has been hand<br />

to mouth, and it is CMR’s business plan to acquire these projects, and to develop<br />

them to international standards. Because of the limited access, as underground<br />

mines they will always be relatively small, but the high grade will provide for profitable<br />

production.<br />

CMR was originally focused on Bulgaria, Spain and Serbia in Europe. However the<br />

company has recently changed focus to South America.<br />

Concurrently with the mine development, CMR is undertaking regional exploration<br />

over some 64,000he of permits . The Colombian region is very prospective and is the<br />

source of overall South American gold production. A complex arrangement of three<br />

subduction zones has caused multiple gold <strong>mineral</strong>izing events with several styles<br />

of gold <strong>mineral</strong>ization being recognised. Subduction zones are well known as the<br />

foundation of a majority of the large gold deposits worldwide.<br />

Colombia<br />

Since the election of pro-mining President Alvaro Uribe in 2002, Colombia has<br />

made huge strides tackling violence, improving security, and re-opening areas for<br />

exploration. Colombia, with the assistance of the United States, has taken an active<br />

stance in combating the drug cartels’ sponsored crime campaign. There remain<br />

some remote areas that are under the influence of the drug barons, but these are<br />

being slowly reduced. All crime statistics show a marked decline since 2002, and the<br />

country in general supports the crime busting exploits of the current government.<br />

The foreign investment in Colombia for 2007 was US$9 billion, compared to US$1.7<br />

billion in 2003. GDP growth for the same periods was 7.5% last year compared<br />

to 1.9% in 2003. Colombia is a major oil producer, and is a country with extensive<br />

<strong>mineral</strong> <strong>resources</strong>.<br />

Coal remains the backbone of Colombian mining, and coal majors like Carbones de<br />

Cerrejon Ltd (a BHP Billiton, Xstrata Coal and Anglo American consortium), and USbased<br />

Drummond Coal Inc have major expansion plans. Colombia is the 4th largest<br />

coal producer in the world. Cerro Matoso, a BHP company, produced over 70,000<br />

tonnes of nickel in concentrate in 2007. A number of recent major gold projects have<br />

been discovered. Anglogold Ashanti has reportedly a 13m ounce gold, La Colosha<br />

project in Cagamarca, in the Tolima region, and Greystar Resources the 8m ounce<br />

Angustura project in Norte de Santander. B2Gold has a JV with Anglogold Ashanti<br />

on the Gramalote (58m tonne at 1.14 g/t, 2.12m ozs) project in Antioquia region.<br />

Other major companies undertaking exploration in Colombia include Barrick Gold,<br />

Rio Tinto (which reportedly has dozens coal and polymetallic projects), Newmont<br />

Mining Corp, Antofagasta plc, and Vale.<br />

2 | www.hichens.com<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530

Colombian Exploration and<br />

Exploitation Permits<br />

The Colombian mining regulations, Act 685 were published in 2001. A <strong>mineral</strong><br />

permit is granted which initially encompasses exploration, but is extendable to<br />

exploitation. The permits are issued on a per hectare basis with a maximum size of<br />

10,000 hectares. An annual payment on a per hectare basis is payable in advance.<br />

The initial exploration permit is valid for 3 years but may be extended. All mining in<br />

Colombia, for small scale and larger operations, is under the same permit. Permits<br />

are freely transferable.<br />

The cost of an exploration permit is calculated from the minimum wage, currently<br />

461,000 pesos, per year. The cost is calculated on a sliding scale depending on<br />

the area. An area of less than 2,000 hectares costs 1 daily rate, up to 3 times the<br />

daily rate for greater than 5,000 hectares. The current rate on the smaller scale is<br />

approximately US$8.8 per hectare per year.<br />

Once in production, the permit stipulates the payment of a royalty of 3.8% of the<br />

sales revenue. The permit remains valid for the life of the mine.<br />

Regional Setting<br />

The Northern Andes of Colombia and Ecuador has a productive history of gold<br />

exploitation having produced the majority of the gold in the South American continent.<br />

The region is underlain by a wide geologic diversity, due to the highly active tectonic<br />

environment in which it formed. This has given rise to a wealth of hydrothermal and<br />

magmatic <strong>mineral</strong> occurrences (mainly gold, silver, copper, zinc, nickel and iron).<br />

Many areas of the Colombian Cordilleras have undergone extensive uplift and deep<br />

chemical and physical erosion due to the tropical high-rainfall conditions. This<br />

combination of processes has allowed a variety of <strong>mineral</strong>isation styles formed at<br />

depth to be exposed at the surface, and hence to be “discovered”. Additionally, the<br />

process of tropical weathering and erosion has created extensive gold concentrations<br />

within residual alluvial horizons, and has facilitated, from an historical through to<br />

modern artisanal perspective, the extraction and recovery of gold.<br />

The Andean Cordillera from which Chile, Peru and Ecuador source <strong>mineral</strong> wealth<br />

divides into three branches in Colombia, called the Eastern, Central and Western<br />

Cordilleras. An estimate of post-conquest Colombian gold production of over 80<br />

million ounces has been observed. Colombian gold production since 1985 has<br />

averaged in the region of 800,000 ounces per annum.<br />

About two-thirds of Colombian gold production comes from residual, colluvial or<br />

alluvial mines, and has been extracted via crude artisanal means utilising a minimum<br />

of expense or technology. Accordingly, the majority of present-day gold production<br />

comes from dozens of artisanal to semi-mechanised alluvial and hardrock mining<br />

camps mostly located throughout the Central and Western Cordilleras, and along the<br />

flanking intermontane and Pacific coastal valley systems. Conversely, approximately<br />

90% of Ecuadorian gold production comes from hard-rock sources. Principle<br />

producing areas include Nambija in the Cordilleral Real (southern extension of the<br />

Cordillera Central), and the Zaruma-Portovelo and Ponce Enríquez districts in the El<br />

Oro Metamorphic Belt. Interestingly, the majority of current producing areas in the<br />

Northern Andes exhibit colonial-era production histories and many enjoy multi-million<br />

ounce recorded gold production. Technically, few important “new” gold districts<br />

have been discovered for decades reflecting a lack of modern exploration activity.<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530 www.hichens.com | 3

The Figures below shows many of the notable hardrock and alluvial gold producing<br />

regions of historic through modern importance in the Northern Andes.<br />

Source: Cambridge Mineral Resources<br />

Planned Production Profile<br />

CMR is in the process of establishing a production presence in the country developing<br />

the first mine, Quintana, which should be in production by year end. Thereafter CMR<br />

expects to develop a second and third mine along using the Quintana model. At the<br />

same time CMRare undertaking project evaluation and early stage gold exploration.<br />

Quintana Gold mine<br />

The Quintana Project, which includes the Las Camelias property, is made up of 6 mining<br />

titles and one application and totals 7,667 ha. The Quintana Vein is a mesothermal<br />

quartz-sulphide gold vein dipping at 40 degrees to the east and averages just over<br />

1m true thickness in the mine. A 10 drillhole programme completed in 2007, proved<br />

the existence of the vein 300m down dip and returned higher grades than seen<br />

previously in the mine and also generally better true widths. Additional drilling is<br />

currently underway to seek to extend the resource base.<br />

Quintana has a JORC compliant resource statement which has defined 109,852<br />

tonnes at 24.58g/t gold, 19.85g/t silver (Measured, Indicated and Inferred) containing<br />

86,822ozs of gold. This resource is still open along strike and at depth below the<br />

deepest drill intersects.<br />

In June 2007 CMR completed a positive feasibility study based on a 50 t/d operation<br />

over 5.5 years and a gold price of US$600. The initial capital expenditure was<br />

estimated at US$ 4.54m, with an average cash operating cost of US$ 131/oz over<br />

the mine life.<br />

In January 2008, CMR completed the Project Finance, the BlueCrest loan, to allow<br />

commencement of the necessary plant and infrastructure construction at the project,<br />

with the aim of achieving gold production within approximately six months. Work<br />

commenced on site in February and is currently proceeding according to schedule.<br />

The Quintana Mine is expected to commence production in Q3 2008 at a rate of<br />

15,000 ozs of gold and 6,000 ozs of silver per annum.<br />

This is a relatively small mine, but with the expected grade should be very profitable.<br />

4 | www.hichens.com<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530

The mine was partially developed, and CMR has taken the existing structure, injected<br />

some modern equipment and practices and are expanding the mine.<br />

Quintana Gold-Mine Layout<br />

Source: Cambridge Mineral Resources<br />

The graphic above shows the intended mine layout. The haulage decline is being<br />

extended. At the time of our visit the decline was just beyond level 2. A further 75<br />

meters still to develop. he ore body has a measured, Indicated and inferred resource<br />

of 109,852 tonnes at a grade of 24.6 gms / tonne gold, and 19.9 gms / tonne silver.<br />

At the current gold and silver prices (US$915 / oz gold and US$17.5 / oz silver) the<br />

in-situ value is over US$700 per tonne.<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530 www.hichens.com | 5

Although the <strong>resources</strong> only provide for a 5 year mine life, additional ore is readily<br />

available, as can be seen from the previous mine plan layout. The ore body is a very<br />

distinctive quartz vein with very consistent dip and width. The average width of the<br />

ore body is 0.9 to 1.1 meters. This will allow for simple mining. The company expect<br />

the operating cost to be in the region of US$135 per tonne, excluding debt.<br />

Cross Section – showing the main decline, and projected development with drill hole<br />

data from down dip exploration.<br />

The mine is expected to be constructed within 6 months at a cost of less than<br />

US$6 million. Once complete and in production, CMR will instigate the second gold<br />

mine.<br />

Source: Cambridge Mineral Resources<br />

Although the mine is relatively small, it should generate revenue of over<br />

US$14m, at the current gold price (US$936 / ounce) with operating costs<br />

in the region of US$5m per year, generating an operating profit of US$9m<br />

per year. These figures alone show the potential of modern mining and<br />

processing techniques on these high-grade mines.<br />

2 shaft viewed from the 2nd elevation<br />

Source: Cambridge Mineral Resources<br />

6 | www.hichens.com<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530

Not only are the economics extremely interesting, but the time taken from initial<br />

negotiations to production compelling. For Quintana the initial mine site inspection<br />

was in November 2005 to the first gold pour before year end 2008. We believe the<br />

exploration/development portfolio has the potential to provide similar projects for the<br />

following mine, all to be developed in much the same way.<br />

CMR intend to use the Quintana model to finance and develop a second and third<br />

mine. Numerous potential targets are under investigation by CMR. The area has<br />

extensive small scale local operators, and CMR’s approach is to negotiate with the<br />

locals to acquire a second and third project.<br />

The initial mine would have initial development, by the local miner, and the mine<br />

would be permitted. The finance is available from the initial Blue Crest Loan.<br />

Subsequent Mines<br />

We are of the opinion that high grade underground mines will return as a<br />

profitable investment opportunity for gold investors. It was the low gold<br />

price that forced major gold companies to develop massive open pit mines,<br />

but as those mines are worked out, it will be the underground mines, and in<br />

a mining environment that encourages underground mining that will be the<br />

long term beneficiaries of the current strong gold market.<br />

Hichens Comment<br />

BlueCrest Loan<br />

BlueCrest Capital Management Ltd. are a hedge fund who have made available up<br />

to US$15m to CMR to finance mine development in Colombia. This is essentially<br />

sufficient to finance 3 new mines. Phase one provided a draw down of US$5.4m<br />

for the development of the Qintana Mine. Phase one will be repaid by way 10,450<br />

ounces troy gold payable over a schedule of 3 years starting in September 2008, of<br />

between 200 to 400 ounces per month. To date US$3.6m has been drawn down.<br />

Management expect the project to be completed within budget, but 6 to 8 weeks<br />

late due to legal delays at the start of the build.<br />

Phase 2 and 3 of approximately US$5 million each is available for the second and<br />

third mine at the option of CMR.<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530 www.hichens.com | 7

Source: Cambridge Mineral Resources<br />

Exploration<br />

CMR entered Colombia at the end of 2005 and holds its interests through its wholly<br />

owned subsidiary, Colgold Inc. During 2007 the Company acquired two further<br />

concessions within the world-class Frontino Gold Belt in the Antioquia Department<br />

of north-western Colombia.<br />

In total CMR now holds 52,745 ha, under concession or application in Colombia, of<br />

which 35,135 hectares is held for its potential to host copper and gold porphyries in<br />

the Cauca Department of south-west Colombia.<br />

CMR has 3 exploration blocks in the central cordillera. Projects are targeted on<br />

existing mines or extensions thereof. The quartz veins in the region are known to<br />

be very continuous, but difficult to expose on surface. The company are targeting<br />

existing small scale producers with an offer which includes international mine<br />

planning, finance and modern day equipment.<br />

CMR has a team of 7 geologists exploring over 3 exploration blocks comprising<br />

several permits each in the central cordillera. A number of large low grade gold<br />

deposits have been discovered in the Colombian cordilleras recently. However, the<br />

belt which extends into Equador in the south hosts one of the most exciting gold<br />

discoveries over the past two years, the Fruta del Norte deposit of Aurelian. CMR is<br />

targeting all styles of <strong>mineral</strong>ization from high-grade underground vein type mines to<br />

larger scale epithermal and porphyry-gold targets.<br />

8 | www.hichens.com<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530

Frontino Gold Belt<br />

CMR continued to focus on the Frontino Gold Belt in the Antioquia Province, as<br />

this area has historically produced approximately 45% of the country’s gold and<br />

continues to do so. This belt is one of the world’s greatest mesothermal gold fields,<br />

with estimated production of 8-9Mozs from the Segovia-Remedios region alone.<br />

Mineralization occurs within extensive vein structures typically exhibiting widths from<br />

a few centimetres to several metres but typically in the 1 to 2m range. These veins<br />

either are near vertical or dip at 30-45 degrees and are formed by ribbon-banded<br />

quartz with subordinate pyrite, sphalerite and galena containing free gold and have<br />

simple metallurgical profile with excellent recoveries. Veins have been traced along<br />

strike for several thousand metres and at distances of up to 1,800m down dip.<br />

CMR has 3 main projects within a 20km radius of Segovia-Remedios; Quintana,<br />

La Rosaleda and El Cinco. The eventual construction of a central processing plant<br />

offers a rapid method to enable multi-mine start-ups and CMR plans to develop this<br />

to a capacity of in excess of 100,000ozs per annum over the next 4 years.<br />

El Cinco<br />

CMR completed the negotiation of the Colina Negra Project, to give it majority interest<br />

in a contiguous block of 7,400ha (6 concessions and one application) around the El<br />

Cinco and Colina Negra mines.<br />

Work on site in 2007 included the successful completion of the Chingale exploration<br />

programme, as well as commencing exploration on the Colina Negra vein system and<br />

other <strong>mineral</strong>ized structures, and completing initial prospecting of the surrounding<br />

areas held by the company.<br />

At Colin Negra, the following results were obtained across the vein: 1.0m @ 114.31g/t<br />

gold, 1.0m @ 66.2g/t gold, 1.5m @ 35.2g/t gold, 1.0m @ 22.5g/t gold, 1.0m @<br />

10.4g/t gold and 1.57m @ 10.1g/t gold. Prospecting results from the surrounding<br />

areas indentified five areas for further exploration, with results including 19.68 g/t Au<br />

and 40 g/t Ag over 0.7m in quartz float and 5.76 g/t Au and 10.2 g/t Ag over 1m in<br />

an outcrop of the main vein nearby, as well as 1.79 g/t Au, 318.4 g/t Ag and 20.23<br />

g/t Au, 7 g/t Ag from old waste dump piles of now abandoned trial workings.<br />

La Rosaleda<br />

The La Rosaleda project is CMR’s third project in the Frontino Gold Belt and comprises<br />

566.2ha in three concessions and three applications, to the immediate south of the<br />

Frontino Gold Mines in the Segovia-Remedios area.<br />

Initial exploration on the project commenced in May 2007 with a surface-prospecting<br />

programme. To date over sixty old artisanal mine workings have been identified,<br />

which reflect the three main structural trends seen in the district. In addition two<br />

currently active artisanal mines are located just outside the area of the agreement,<br />

returning grades of 6.89g/t gold and 57.6g/t silver over 0.9m. It is planned to move<br />

one of the projects in the area to the drill ready stage by the end of 2008.<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530 www.hichens.com | 9

Corporate Activity<br />

Peruvian Exploration<br />

Peruvian Exploration<br />

CMR has recently completed a feasibility study on their Rasuhuilca deposit in Peru.<br />

Rasuhuilca is an underground gold/silver deposit in the high Andes. The altitude is at<br />

approximately 4,800 metres above sea level. The project was explored by Cominco<br />

in the mid 1980’s; who completed a significant amount of underground development<br />

to outline the <strong>mineral</strong>ized body. The underground workings were rehabilitated and<br />

several hundred metres of vertical development and stope preparation was completed<br />

by CMR in 2007-08.<br />

The overall Rasuhuilca Main and West Zones contain 321,100 tonnes @ 2.15 g/t<br />

Au, 185.2 g/t Ag (252g/t Ag Equivalent) at a 75 g/t Ag Equivalent Cutoff. Additional<br />

potential to expand these <strong>resources</strong> exists to the west within the Rasuhuilca North<br />

West and Rasuhuilca South areas around the 4941m Level.<br />

Within this Resource a Proven & Probable Reserve (JORC Standard) of 168,700<br />

tonnes @ 3.05 g/t Au, 216 g/t Ag (368 g/t Ag Equivalent) has been defined in the<br />

mining plan for the Main Zone. Only this reserve has been considered in the feasibility<br />

study which concludes that the Rasuhuilca mine can produce silver at a net cost of<br />

US$ 5.73 per troy ounce or on a full capital depreciated cost of US$ 7.79 per troy<br />

ounce.<br />

Development of the project is expected to require a capital spend of US$ 3.08 million<br />

over a five month period. CMR is presently seeking the finance to develop the<br />

mine.<br />

Spanish and Bulgarian<br />

Exploration properties<br />

CMR has a number of projects from their previous incarnation in Spain and Bulgaria.<br />

The Bulgarian properties are being joint ventured with Electrum Gold, a significant<br />

private US-based international gold exploration company. The Spanish projects are<br />

expected to form the basis of a new float in Canada shortly with CMR retaining a<br />

substantial interest.<br />

Fiscal Environment<br />

Colombia has a history of mining with numerous small scale miners, as well as a<br />

number of larger mining groups in the country. BHP’s Cerro Matoso is a major<br />

nickel producer. Currently Colombia has a 4% royalty on gold production and a<br />

36% corporate tax rate. Value Added Tax is set at 16%. Mine and exploration title<br />

database is freely available via the internet (www.ingeominas.gov.co). As discussed<br />

previously <strong>mineral</strong> exploration and exploitation titles are one and the same. A<br />

<strong>mineral</strong> exploration title can be extended, but would then either be reclassified as a<br />

exploitation title, or dropped.<br />

10 | www.hichens.com<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530

Peer Group Comparison<br />

We have included our peer group comparison of the London’s AiM market junior<br />

exploration companies for comparison. As we have suggested before, it is difficult<br />

to compare junior exploration companies. But factors such as the area of operation,<br />

for both security if title and geologic potential are important, but mostly the quality of<br />

the management.<br />

Source: Hichens Harrison on company data<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530 www.hichens.com | 11

A number of other junior exploration companies are also operating in Colombia,<br />

including Colombia Goldfields. Major discoveries of gold deposits have been<br />

made. The Colombian President leaked information on a 21m ounce gold deposit,<br />

Cagamarca in Tolema region, owned by Anglo Gold Ashanti. Greystar Resources,<br />

a Canadian and London listed company, with a market value of £92 million, is<br />

exploring the Angostura project which has an indicated resource of 7.9m ounces<br />

gold. Colombia Goldfields, listed in Canada, with a market value of £31 equivalent,<br />

has the Marmato gold project with 2.55m ounces gold. Colombia Goldfields have<br />

spent over US$30m on the project.<br />

B2Gold, a Canadian listed company with a market value of £70m equivalent is<br />

exploring for gold in Colombia, A Colombian alluvial gold miner, Mineros SA is listed<br />

on the Colombian exchange with a value of £96m equivalent is exploring a copper /<br />

molybdenum deposit in the south.<br />

Comparing CMR to equivalent gold producers also provides us with a compelling<br />

valuation. Serabi, a London listed South American gold producer producing at a rate<br />

of 34,000 ounces per year has a value of £26 million.<br />

Conclusion<br />

We believe the current market valuation of CMR of less than £4million, does not<br />

reflect the true potential of the company. The gold mining operations, although on<br />

the smaller side, will be highly profitable. Using the company’s estimate of 15,000<br />

ounces per year, the company will generate revenue of US$14m per year (using a<br />

gold price of US$935/ounce) with costs expected to be one third of that number. The<br />

mines are small underground mines, but close to the surface and simple to operate.<br />

It is an old adage in the mining industry, that the three most important factors in<br />

underground mining are grade, grade and grade. The reality is their delivered grade is<br />

the single most important factor in mine profitability. The delivered grade at Quintana<br />

should be high, a high grade in a 1m width vein, which will result in high profitability.<br />

The Quintana model will be easy to replicate – there are a number of potential targets<br />

in the area. Quintana and the next two mines are financed via the BlueCrest loan. So<br />

we believe the company’s interim target of 3 new producing high-grade gold mines in<br />

Colombia by the end of next year is very achievable. If that transpires, the company<br />

will have revenue of over US$40m per year, using the current gold price, and should<br />

be very profitable.<br />

For us however, the real potential value does not lie in the production units, but<br />

in CMR’s exploration potential. Colombia is a <strong>mineral</strong> rich country, with a limited<br />

amount of large scale exploration. Junior exploration projects have been limited due<br />

to the country risk. But we believe this is in the process of being reduced and we<br />

see CMR as having the first mover advantage. Exploration is at an early stage but<br />

the potential is massive. Given the company’s experience and the fact that they are<br />

established in the country, with a number of high potential exploration targets, we<br />

believe the current valuation is way too low.<br />

CMR share price is discounted because of their history of exploration in Europe.<br />

Those projects are in the process of being vended out to third parties, and CMR<br />

intend to focus on the new area of the North of South America. We believe the<br />

exploration portfolio alone exceeds the current market value. The small, potentially<br />

highly profitable gold mines are in the mix at zero value.<br />

12 | www.hichens.com<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530

NOTES<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530 www.hichens.com | 13

NOTES<br />

14 | www.hichens.com<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530

A marketing communication under FSA Rules, this document has not been prepared in accordance with<br />

legal requirements designed to promote the independence of investment research and is not subject to any<br />

prohibition on dealing ahead of the dissemination of investment research.<br />

This research cannot be classified as objective under Hichens Harrison & Co plc research policy.<br />

This report is issued by Hichens, Harrison & Co Plc (“Hichens”) in the UK, which is authorised and regulated<br />

by the Financial Services Authority in connection with its UK distribution. Hichens is a member of the<br />

London Stock Exchange.<br />

The following Research Disclaimer appears on all printed research produced by Hichens. Additional<br />

information with respect to any security referred to herein may be made available on request. The material in<br />

this report is for the general information of clients of Hichens only. It does not take into account the particular<br />

investment objectives, financial situation or needs of individual clients. Before acting upon or relying on any<br />

advice or recommendations in this material, clients should consider first whether it is suitable for their<br />

particular circumstances and secondly seek further specific professional advice. This material should not<br />

be construed in any circumstances whatsoever as an offer to sell or solicitation of any offer to buy any<br />

security or other financial instrument, nor shall it, or the fact of its distribution, form the basis of, or be relied<br />

upon in connection with, any contract relating to such action or any other matter. The material in this report<br />

is based on information that we consider reliable and accurate from time to time, but we do not warrant<br />

or represent (expressly or impliedly) that it is accurate, complete, not misleading or as to its fitness for the<br />

purpose intended and it should not be relied upon as such. Any Opinion expressed constitute opinions as<br />

of the date appearing on this material only. We endeavour to update the material in this report on a timely<br />

basis, but regulatory compliance or other reasons may prevent us from doing so. Hichens salespeople,<br />

traders and other professionals may from time to time (a) have long or short positions in, act as principal in<br />

and buy or sell securities, warrants, futures, options, derivatives or other financial instruments referred to in<br />

this material; and (b) provide oral or written market commentary or trading strategies to our clients and our<br />

proprietary trading desks that reflect opinions that are contrary to the opinions expressed in this research.<br />

Our asset management area, our proprietary trading desks and investing businesses may make investment<br />

decisions that are inconsistent with the recommendations or views expressed in this research. This report<br />

is issued in conjunction with Hichens Research Policy which is summarized on Hichens website at http://<br />

www.hichens.com/Research-Policy and is available from the Compliance Officer at Hichens.<br />

Specific disclosures required under Conduct of Business Rule 7.17 are set out in this report and general<br />

disclosures may be accessed via (http://www.hichens.com/Market-Abuse-Directive). Unless otherwise<br />

stated, share prices are as at the close of business on the date of the research note. Neither the whole nor<br />

any part of this report may be duplicated in any form or by any means. Neither should any of this material<br />

be redistributed or disclosed to anyone without the prior consent of Hichens. Hichens accepts no liability<br />

whatsoever for any direct, indirect or consequential loss or damage of any kind arising out of the use of<br />

or reliance upon all or any of this material howsoever arising. The services, securities and investments<br />

discussed in this report may not be available to nor suitable for all investors. Investors should make their<br />

own investment decisions based upon their own financial objectives and financial <strong>resources</strong> and it should<br />

be noted that investment involves risk, including the risk of capital loss. Past performance of investments is<br />

no guide to future performance. You may not get back the amount of capital you invest. There is an extra<br />

risk of losing money when shares are bought in some smaller companies. For shares listed on AIM, any<br />

person should be aware that because the rules for AIM are less demanding than those of the Official List<br />

of the London Stock Exchange, the risks are higher. Any income projections and yields are estimated and<br />

are included for indication only. Further, any valuations given in this brochure may not accurately reflect the<br />

values at which investments may actually be bought or sold and no allowance has been made for taxation.<br />

If you have any queries about your tax position, you must seek separate professional advice.<br />

[Hichens is an agency broker and therefore does not deal as principal in the securities mentioned herein].<br />

This research note is confidential and is being supplied to you for information purposes only. They may<br />

not (directly or indirectly) be reproduced, further distributed to any person or published, in whole or in part,<br />

for any purpose whatsoever. Neither this document, nor any copy of it, may be taken or transmitted into<br />

the United States, Canada, Australia, Ireland, South Africa or Japan or into any jurisdiction where it would<br />

be unlawful to do so. Any failure to comply with this restriction may constitute a violation of relevant local<br />

securities laws. If you have received this document in error please telephone Martin Lampshire on +44 (0)<br />

20 7382 4479.<br />

Risk warnings are provided for your information and protection. We strongly encourage you to read them<br />

and to contact us if you have any questions about the features or risks of any investment or service.<br />

Telephone calls may be recorded.<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530 www.hichens.com | 15

Hichens, Harrison Equity Research Team<br />

jeremy.chantry@hichens.com<br />

Head of Research<br />

Jeremy Chantry 020 7382 7791<br />

jeremy.chantry@hichens.com<br />

rhulf@hulfhamilton.com<br />

Energy<br />

Jeremy Chantry 020 7382 7791<br />

Richard Hulf (Consultant) 07960 332 603 / 01923 831 754<br />

nick.hawken@hichens.com<br />

magnus.mathewson@hichens.com<br />

Financial Services<br />

Nick Hawken 020 7382 4454<br />

Magnus Mathewson 020 7382 4459<br />

dave.paxton@hichens.com<br />

Mining<br />

Dave Paxton 020 7382 7758<br />

jeremy.chantry@hichens.com<br />

Healthcare and Education<br />

Jeremy Chantry 020 7382 7791<br />

robyn.harte-bunting@hichens.com<br />

Technology<br />

Robyn Harte-Bunting 020 7382 4452<br />

victoria.chernykh@hichens.com<br />

jeremy.chantry@hichens.com<br />

Smaller Companies<br />

Victoria Chernykh 020 7382 4663<br />

Jeremy Chantry 020 7382 7791<br />

sean.lunn@hichens.com<br />

Daily UK, South African and Global and Morning Meeting Note<br />

Sean Lunn 27 (0) 21 950 2711<br />

Economics<br />

Capital Research<br />

kajal.patel@hichens.com<br />

Desktop Publishing<br />

Kajal Patel 020 7382 4466<br />

16 | www.hichens.com<br />

Hichens, Harrison & Co. plc • Bell Court House, 11 Blomfield Street, London EC2M 1LB • Tel: +44 (0)207 382 4451 • Registered in England no 2368530