Statutory Issue Paper No62R - Reinsurance Focus

Statutory Issue Paper No62R - Reinsurance Focus

Statutory Issue Paper No62R - Reinsurance Focus

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

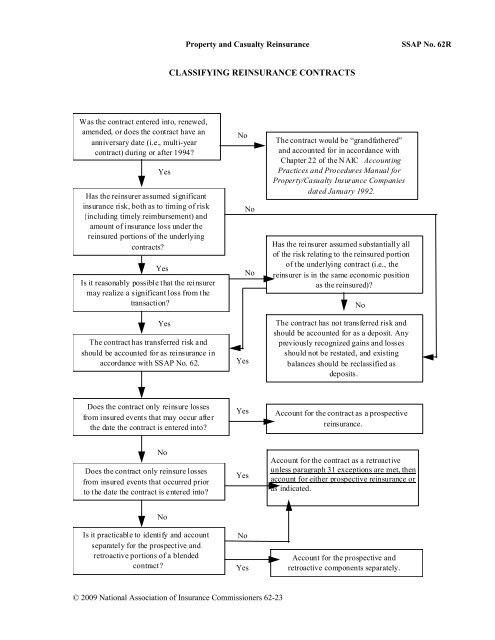

Property and Casualty <strong>Reinsurance</strong><br />

SSAP No. 62R<br />

CLASSIFYING REINSURANCE CONTRACTS<br />

Was the contract entered into, renewed,<br />

amended, or does the contract have an<br />

anniversary date (i.e., multi-year<br />

contract) during or after 1994?<br />

Yes<br />

Has the reinsurer assumed significant<br />

insurance risk, both as to timing of risk<br />

(including timely reimbursement) and<br />

amount of insurance loss under the<br />

reinsured portions of the underlying<br />

contracts?<br />

Yes<br />

Is it reasonably possible that the reinsurer<br />

may realize a significant loss from the<br />

transaction?<br />

Yes<br />

The contract has transferred risk and<br />

should be accounted for as reinsurance in<br />

accordance with SSAP No. 62.<br />

No<br />

No<br />

No<br />

Yes<br />

The contract would be “grandfathered”<br />

and accounted for in accordance with<br />

Chapter 22 of the NAIC Accounting<br />

Practices and Procedures Manual for<br />

Property/Casualty Insurance Companies<br />

dated January 1992.<br />

Has the reinsurer assumed substantially all<br />

of the risk relating to the reinsured portion<br />

of the underlying contract (i.e., the<br />

reinsurer is in the same economic position<br />

as the reinsured)?<br />

No<br />

The contract has not transferred risk and<br />

should be accounted for as a deposit. Any<br />

previously recognized gains and losses<br />

should not be restated, and existing<br />

balances should be reclassified as<br />

deposits.<br />

Does the contract only reinsure losses<br />

from insured events that may occur after<br />

the date the contract is entered into?<br />

Yes<br />

Account for the contract as a prospective<br />

reinsurance.<br />

No<br />

Does the contract only reinsure losses<br />

from insured events that occurred prior<br />

to the date the contract is entered into?<br />

Yes<br />

Account for the contract as a retroactive<br />

unless paragraph 31 exceptions are met, then<br />

account for either prospective reinsurance or<br />

as indicated.<br />

No<br />

Is it practicable to identify and account<br />

separately for the prospective and<br />

retroactive portions of a blended<br />

contract?<br />

No<br />

Yes<br />

Account for the prospective and<br />

retroactive components separately.<br />

© 2009 National Association of Insurance Commissioners 62-23

![202 Folio No 734 Neutral Citation Number: [2006] EWHC 1345 (QB ...](https://img.yumpu.com/50015000/1/184x260/202-folio-no-734-neutral-citation-number-2006-ewhc-1345-qb-.jpg?quality=85)