Statutory Issue Paper No62R - Reinsurance Focus

Statutory Issue Paper No62R - Reinsurance Focus

Statutory Issue Paper No62R - Reinsurance Focus

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

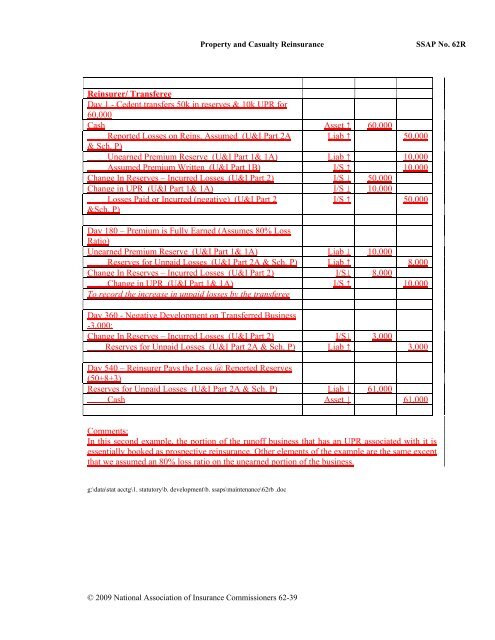

Property and Casualty <strong>Reinsurance</strong><br />

SSAP No. 62R<br />

Reinsurer/ Transferee<br />

Day 1 - Cedent transfers 50k in reserves & 10k UPR for<br />

60,000<br />

Cash Asset ↑ 60,000<br />

Reported Losses on Reins. Assumed (U&I Part 2A Liab ↑ 50,000<br />

& Sch. P)<br />

Unearned Premium Reserve (U&I Part 1& 1A) Liab ↑ 10,000<br />

Assumed Premium Written (U&I Part 1B) I/S ↑ 10,000<br />

Change In Reserves – Incurred Losses (U&I Part 2) I/S ↓ 50,000<br />

Change in UPR (U&I Part 1& 1A) I/S ↓ 10,000<br />

Losses Paid or Incurred (negative) (U&I Part 2<br />

&Sch. P)<br />

I/S ↑ 50,000<br />

Day 180 – Premium is Fully Earned (Assumes 80% Loss<br />

Ratio)<br />

Unearned Premium Reserve (U&I Part 1& 1A) Liab ↓ 10,000<br />

Reserves for Unpaid Losses (U&I Part 2A & Sch. P) Liab ↑ 8,000<br />

Change In Reserves – Incurred Losses (U&I Part 2) I/S↓ 8,000<br />

Change in UPR (U&I Part 1& 1A) I/S ↑ 10,000<br />

To record the increase in unpaid losses by the transferee<br />

Day 360 - Negative Development on Transferred Business<br />

-3,000:<br />

Change In Reserves – Incurred Losses (U&I Part 2) I/S↓ 3,000<br />

Reserves for Unpaid Losses (U&I Part 2A & Sch. P) Liab ↑ 3,000<br />

Day 540 – Reinsurer Pays the Loss @ Reported Reserves<br />

(50+8+3)<br />

Reserves for Unpaid Losses (U&I Part 2A & Sch. P) Liab ↓ 61,000<br />

Cash Asset ↓ 61,000<br />

Comments:<br />

In this second example, the portion of the runoff business that has an UPR associated with it is<br />

essentially booked as prospective reinsurance. Other elements of the example are the same except<br />

that we assumed an 80% loss ratio on the unearned portion of the business.<br />

g:\data\stat acctg\1. statutory\b. development\b. ssaps\maintenance\62rb .doc<br />

© 2009 National Association of Insurance Commissioners 62-39

![202 Folio No 734 Neutral Citation Number: [2006] EWHC 1345 (QB ...](https://img.yumpu.com/50015000/1/184x260/202-folio-no-734-neutral-citation-number-2006-ewhc-1345-qb-.jpg?quality=85)