cv Ronald Huisman - Institut d'Economia de Barcelona

cv Ronald Huisman - Institut d'Economia de Barcelona

cv Ronald Huisman - Institut d'Economia de Barcelona

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

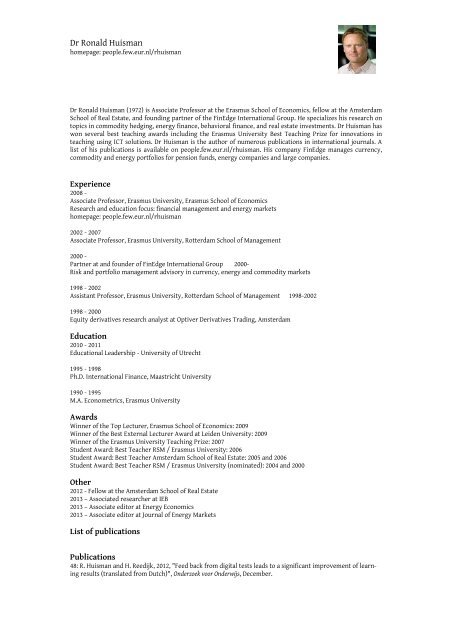

Dr <strong>Ronald</strong> <strong>Huisman</strong><br />

homepage: people.few.eur.nl/rhuisman<br />

Dr <strong>Ronald</strong> <strong>Huisman</strong> (1972) is Associate Professor at the Erasmus School of Economics, fellow at the Amsterdam<br />

School of Real Estate, and founding partner of the FinEdge International Group. He specializes his research on<br />

topics in commodity hedging, energy finance, behavioral finance, and real estate investments. Dr <strong>Huisman</strong> has<br />

won several best teaching awards including the Erasmus University Best Teaching Prize for innovations in<br />

teaching using ICT solutions. Dr <strong>Huisman</strong> is the author of numerous publications in international journals. A<br />

list of his publications is available on people.few.eur.nl/rhuisman. His company FinEdge manages currency,<br />

commodity and energy portfolios for pension funds, energy companies and large companies.<br />

Experience<br />

2008 -<br />

Associate Professor, Erasmus University, Erasmus School of Economics<br />

Research and education focus: financial management and energy markets<br />

homepage: people.few.eur.nl/rhuisman<br />

2002 - 2007<br />

Associate Professor, Erasmus University, Rotterdam School of Management<br />

2000 -<br />

Partner at and foun<strong>de</strong>r of FinEdge International Group 2000-<br />

Risk and portfolio management advisory in currency, energy and commodity markets<br />

1998 - 2002<br />

Assistant Professor, Erasmus University, Rotterdam School of Management 1998-2002<br />

1998 - 2000<br />

Equity <strong>de</strong>rivatives research analyst at Optiver Derivatives Trading, Amsterdam<br />

Education<br />

2010 - 2011<br />

Educational Lea<strong>de</strong>rship - University of Utrecht<br />

1995 - 1998<br />

Ph.D. International Finance, Maastricht University<br />

1990 - 1995<br />

M.A. Econometrics, Erasmus University<br />

Awards<br />

Winner of the Top Lecturer, Erasmus School of Economics: 2009<br />

Winner of the Best External Lecturer Award at Lei<strong>de</strong>n University: 2009<br />

Winner of the Erasmus University Teaching Prize: 2007<br />

Stu<strong>de</strong>nt Award: Best Teacher RSM / Erasmus University: 2006<br />

Stu<strong>de</strong>nt Award: Best Teacher Amsterdam School of Real Estate: 2005 and 2006<br />

Stu<strong>de</strong>nt Award: Best Teacher RSM / Erasmus University (nominated): 2004 and 2000<br />

Other<br />

2012 - Fellow at the Amsterdam School of Real Estate<br />

2013 – Associated researcher at IEB<br />

2013 – Associate editor at Energy Economics<br />

2013 – Associate editor at Journal of Energy Markets<br />

List of publications<br />

Publications<br />

48: R. <strong>Huisman</strong> and H. Reedijk, 2012, "Feed back from digital tests leads to a significant improvement of learning<br />

results (translated from Dutch)", On<strong>de</strong>rzoek voor On<strong>de</strong>rwijs, December.

CV <strong>Ronald</strong> <strong>Huisman</strong> page 2<br />

47: R. <strong>Huisman</strong>, 2012, "How the financial crisis changed clean-tech investment preferences", fsinsight.org, May<br />

9.<br />

46: R. <strong>Huisman</strong> and H.E. Reedijk, 2012, "Feed back from digital tests leads to a significant improvement of learning<br />

results (translated from Dutch)", econonieopinie.nl.<br />

45: D.M. Hofman and R. <strong>Huisman</strong>, 2012, "Did the Financial Crisis Lead to Changes in Private Equity Investor<br />

Preferences Regarding Renewable Energy Policies?", Energy Policy, 47, 111-116.<br />

44: R. <strong>Huisman</strong> and M. Kilic, 2012, "Electricity Futures Prices: Indirect Storability, Expectations, and Risk Premiums",<br />

Energy Economics, 34, 892-898.<br />

43: R. <strong>Huisman</strong> and M. Kilic, 2013, "A History of European Electricity Prices", Applied Economics, 45, 2683-2693.<br />

42: R. <strong>Huisman</strong>, N.L. van <strong>de</strong>r Sar, and R.C.J. Zwinkels, 2012, "A New Measurement Method of Investor Overconfi<strong>de</strong>nce",<br />

Economic Letters, 114, 69-71.<br />

41: R. <strong>Huisman</strong>, 2011, "Should Holland export electricity? (translated from Dutch)”, ESB, 64.<br />

40: R. <strong>Huisman</strong>, A. Katsman, and M. Kilic, 2011, "Storage reduces volatility of gas prices. (translated from<br />

Dutch)", Energie beurs bulletin, 15 (1), 8.<br />

39: R. <strong>Huisman</strong> and M. Kilic, 2011, "Extreme Changes in Prices of Electricity Futures", Insurance Markets and<br />

Companies: Analyses and Actuarial Computations, 2, 21-25.<br />

38: R. <strong>Huisman</strong>, A. Katsman, and M. Kilic, 2011, "The economic value of the Bergermeer gas storage facility.<br />

(translated from Dutch) ", economieopinie.nl.<br />

37: R. <strong>Huisman</strong> and R. Zwinkels, 2010, "Measuring risk perception. (translated from Dutch)", economieopinie.nl.<br />

36: R. <strong>Huisman</strong>, 2010, "The possibilities for financing sustainable heating projects in the Province of South<br />

Holland. (translated from Dutch)", report for the Province of South Holland.<br />

35: A. Bloys van Treslong and R. <strong>Huisman</strong>, 2010, "A Comment on: Storage and the Electricity Forward Premium",<br />

Energy Economics, 32 (2), 321-324.<br />

34: R. <strong>Huisman</strong>, 2009, An Introduction to Mo<strong>de</strong>ls for the Energy Market: The Thinking behind Econometric Techniques<br />

and Their Application, RISKbooks, ISBN 978-1906348229.<br />

33. R. <strong>Huisman</strong>, 2009, “Energy Trading, Emission Certificates and Risk Management”, in: A. Bausch and B.<br />

Schwenker, Handbook Utility Management, Springer Verlag, ISBN 9783540793489, 349-360.<br />

32. R. <strong>Huisman</strong>, R. Mahieu and F. Schlichter, 2009, "Electricity Portfolio Management: Optimal Peak / Off-Peak<br />

Allocations", Energy Economics, 31, 169-174.<br />

31. R. <strong>Huisman</strong>, 2008, The influence of temperature on spike probability in day-ahead power prices", Energy<br />

economics, 30, 2697-2704.<br />

30. R. <strong>Huisman</strong>, 2007, “ Currency Risk: Is it a Strategic Choice?”, IPE Netherlands, November, 14-16.<br />

29. R. <strong>Huisman</strong>, K. Koedijk and R. Pownall, 2007, “VaR-X: Fat Tails in Financial Risk Management”, In: J. Danielsson<br />

(editor), 2007, The Value-at-Risk Reference: Key Issues in the Implementation of Market Risk, Riskbooks.<br />

28. R. <strong>Huisman</strong>, R. Mahieu and C. Huurman, 2007, "Hourly electricity prices in day-ahead markets", Energy<br />

economics, 29, 240-248.<br />

27. R. <strong>Huisman</strong> and C. Huurman, 2007, “Being in Balance: More Efficiency Through Liberalization”, ICFAI Journal<br />

of Environmental Economics, 5 (1), 28-43.<br />

26. R. <strong>Huisman</strong> and R.J. Mahieu, 2005, “Currency Management adds Systematic Value”, Global Pensions, July, 27-<br />

28.

CV <strong>Ronald</strong> <strong>Huisman</strong> page 3<br />

25. R. <strong>Huisman</strong> and C. Huurman, 2004, “Liberalization makes the power market more efficient (translated from<br />

Dutch)”, ESB, 89, nr. 4445, 510-512.<br />

24. R. <strong>Huisman</strong> and R. Mahieu, 2003, "Regime jumps in electricity prices", Energy economics, 25, 425-434.<br />

23. R. <strong>Huisman</strong> and C. <strong>de</strong> Jong, 2003, “Option Pricing for Power Prices with Spikes”, Energy + Power Risk Management,<br />

February, 12-16.<br />

22. R. Campbell and R. <strong>Huisman</strong>, 2003, “Measuring Credit Spread Risk”, The Journal of Portfolio Management, 29, 4,<br />

121-127.<br />

21. R. <strong>Huisman</strong>, C.G. Koedijk, C. Kool, and F. Palm, 2002, “The Tail-Fatness of FX Returns Reconsi<strong>de</strong>red”, De<br />

Economist, 150, 3, 299-312.<br />

20. R. <strong>Huisman</strong>, F. Limburg, and R.J. Mahieu, 2002, “More efficient hedging of currency risk (translated from<br />

Dutch)”, ESB, 510-511.<br />

19. R. <strong>Huisman</strong>, C.G. Koedijk, C. Kool, and F. Palm, 2001, “Tail In<strong>de</strong>x Estimation in Small Samples”, Journal of<br />

Business and Economic Statistics, 19, 208-216.<br />

18. R. <strong>Huisman</strong> and R.J. Mahieu, 2001, “Regime Jumps in Power Prices”, Energy + Power Risk Management, September,<br />

32-35.<br />

17. R. Campbell, R. <strong>Huisman</strong>, and C.G. Koedijk, 2001, “Optimal Portfolio Selection in a Value at Risk Framework”,<br />

Journal of Banking and Finance, 25, 1789–1804.<br />

16. P. Eichholtz and R. <strong>Huisman</strong>, 2001, “The Cross-Section of Global Property Shares Returns”, in: S. Brown and C.<br />

Liu, A Global Perspective on Real Estate Cycles (The New York University Salomon Center Series on Financial Markets<br />

and <strong>Institut</strong>ions), 89–102.<br />

15. R. <strong>Huisman</strong>, C.G. Koedijk, and R. Pownall, 1999, “Dealing with Market Extremes”, Derivatives Week, June 28.<br />

14. M.D. Flood, R. <strong>Huisman</strong>, C.G. Koedijk, and R.J. Mahieu, 1999, “Quote Disclosure and Price Discovery in Multiple<br />

Dealer Financial Markets”, Review of Financial Studies, 12, 37-59.<br />

13. J. Annaert, R. <strong>Huisman</strong>, and J. Spronk (eds.), 1999, “Finance and Investments Part 22 (translated from<br />

Dutch)”, Haveka Publishers Alblasserdam.<br />

12. A. Herst, R. <strong>Huisman</strong>, and M. Spee, 1999, “Click funds (translated from Dutch)”, Economenblad.<br />

11. R. <strong>Huisman</strong> and M. Schweitzer, 1999, “Dutch Corporate Bonds in a Mixed Asset Portfolio”, VBA Journaal.<br />

10. R. <strong>Huisman</strong>, C.G. Koedijk, and R. Pownall, 1998, “VaR-x: Fat Tails in Financial Risk Management”, Journal of<br />

Risk, 1, 43–61.<br />

9. R. <strong>Huisman</strong> and C.G. Koedijk, 1998, “Financial Market Competition: The Effects of Transparency”, De Economist,<br />

146, 3, 463-473.<br />

8. R. <strong>Huisman</strong>, C.G. Koedijk, C. Kool, and F. Nissen, 1998, “Extreme Support for Uncovered Interest Parity”,<br />

Journal of International Money and Finance, 17, 211–228.<br />

7. P. Eichholtz, R. <strong>Huisman</strong>, C.G. Koedijk, and L. Schuin, 1998, “Continental Factors in International Real Estate<br />

Returns”, Real Estate Economics, 26, 3, 493–509.<br />

6. R. Corman and R. <strong>Huisman</strong>, 1998, “Soccer stocks: toto or a serious investment (translated from Dutch)”, ESB,<br />

680–682.<br />

5. R. <strong>Huisman</strong>, M. van Hel<strong>de</strong>n, and M. Schweitzer, 1998, “The fast growth of the Dutch corporate bonds market<br />

(translated from Dutch)”, ESB, 407-407.<br />

4. P. Eichholtz, R. <strong>Huisman</strong>, H. op ‘t Veld, and L. Schuin, 1998, “Internationale Diversificatie voor Vastgoed<br />

Beleggers”, Bedrijfskun<strong>de</strong>, 1, 72–77.

CV <strong>Ronald</strong> <strong>Huisman</strong> page 4<br />

3. R. <strong>Huisman</strong> and R. Verheul, 1998, “Technical Analysis in Holland (translated from Dutch)”, Ne<strong>de</strong>rBelgisch<br />

Magazine, 42–45.<br />

2. R. <strong>Huisman</strong> and R. Verheul, 1997, “Technical Analysis in Holland (translated from Dutch)”, ESB, 13-14.<br />

1. R. <strong>Huisman</strong>, 1996, “New Life for Safety First”, ESB, 493-493.