ERC Case No. 2002-18 - Energy Regulatory Commission

ERC Case No. 2002-18 - Energy Regulatory Commission

ERC Case No. 2002-18 - Energy Regulatory Commission

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

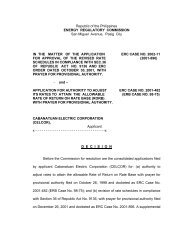

Republic of the Philippines<br />

ENERGY REGULATORY COMMISSION<br />

San Miguel Avenue, Pasig City<br />

IN THE MATTER OF THE APPLICATION<br />

FOR AUTHORITY TO REVISE/UNBUNDLE<br />

RATES IN ACCORDANCE WITH SECTION<br />

36 OF R.A. 9136, AND FOR APPROVAL OF<br />

APPRAISAL OF PROPERTIES, WITH<br />

PRAYER FOR PROVISIONAL AUTHORITY.<br />

<strong>ERC</strong> CASE NOS. <strong>2002</strong>-<strong>18</strong><br />

and <strong>2002</strong>-143<br />

MANSONS CORPORATION (MANSONS)<br />

Applicant.<br />

x-----------------------------------------------------x<br />

D E C I S I O N<br />

Before the <strong>Commission</strong> for resolution is the application filed on January 16,<br />

<strong>2002</strong> by applicant Mansons Corporation (MANSONS) for authority to<br />

revise/unbundle its rates in accordance with Section 36 of Republic Act <strong>No</strong>. 9136<br />

(R.A. 9136) with prayer for provisional authority. Subsequently, on March 4, <strong>2002</strong>,<br />

MANSONS filed an “Amended Application”.<br />

Having found the application sufficient in form and substance with the<br />

required fees having been paid, an Order and a <strong>No</strong>tice of Public Hearing were<br />

issued both dated April 10, <strong>2002</strong> setting the same for initial hearing on June 11,<br />

<strong>2002</strong>.

Page 2 of 35<br />

In the same Order, MANSONS was directed to publish at its own expense,<br />

the <strong>No</strong>tice of Public Hearing twice for two (2) successive weeks in two (2)<br />

newspapers of nationwide circulation in the country, the last date of publication to<br />

be made not later than two (2) weeks before the scheduled date of initial hearing.<br />

Copies of the application, the Order and the <strong>No</strong>tice of Public Hearing were<br />

furnished the Office of the Solicitor General (OSG), the <strong>Commission</strong> on Audit<br />

(COA) and the Committees on <strong>Energy</strong> of both Houses of Congress and were<br />

requested to have their respective duly authorized representatives present at the<br />

initial hearing.<br />

Likewise, copies of the Order and the <strong>No</strong>tice of Public Hearing were<br />

furnished the Offices of the Municipal Mayors of Floridablanca and Guagua, both<br />

in the Province of Pampanga, for the appropriate posting thereof on their<br />

respective bulletin boards.<br />

During the June 11, <strong>2002</strong> initial hearing of this case, applicant and Atty.<br />

Joel Jimenez of the Office of the Solicitor General appeared. Applicant presented<br />

its proofs of compliance with the <strong>Commission</strong>’s publication and posting of notice<br />

requirements and had these marked as Exhibits “A” to “C”, inclusive. Thereafter,<br />

it moved for a resetting of the case to have its financial statements re-audited to<br />

conform to the requirements of the <strong>Commission</strong>. Atty. Jimenez did not object.<br />

At the September 10, <strong>2002</strong> hearing, applicant presented its witnesses,<br />

Engr. Reynaldo Gimongala, applicant’s Head, Engineering Department and Mr.<br />

Ricardo Limbauan, applicant’s External Auditor, for direct examinations. Engr.<br />

Gimongala testified on the manner by which the applicant prepared its revised<br />

rate application including the different schedules using the unbundling process.

Page 3 of 35<br />

Mr. Limbauan testified on the re-audit made on applicant’s financial statements.<br />

In the course thereof, documents were presented and marked as Exhibits “D” to<br />

“DD”, inclusive.<br />

The <strong>Commission</strong> propounded clarificatory questions on the witnesses. In<br />

the course thereof, applicant was directed to submit the several explanations on<br />

matters asked.<br />

At the continuation of the hearing on <strong>No</strong>vember 15, <strong>2002</strong>, applicant<br />

presented its last witness, Engr. Roberto Mendoza, Assistant Vice President for<br />

Machinery and Technical Specialties of Asian Appraisal, Inc., for direct<br />

examination. He testified on the methodologies used in arriving at the sound<br />

value appraisal of applicant’s properties. In course thereof, documents were<br />

presented and marked as Exhibits “EE” to “FF-2”, inclusive. Thereafter the<br />

<strong>Commission</strong> propounded clarificatory questions. Applicant then moved that it be<br />

given ten (10) days from said date of hearing to submit its formal offer of exhibits<br />

which the <strong>Commission</strong> granted.<br />

On <strong>No</strong>vember 19, <strong>2002</strong>, applicant filed its formal offer of exhibits which was<br />

admitted for the purposes for which they were being offered.<br />

On <strong>No</strong>vember 28, <strong>2002</strong>, applicant was directed to submit its Assets<br />

Additions and Retirements from 1993 to 1998 and amend its formal offer of<br />

exhibits.<br />

I. MANSONS PROPOSAL<br />

MANSONS proposed to adopt and applies for approval the following rate<br />

schedule which embody the unbundling of its rates in accordance with the sectors

Page 4 of 35<br />

or functions identified in Section 5 of RA 9136. These rates were developed on<br />

the basis of the data and calculations as contained in the schedules prescribed in<br />

the Uniform Rate Filing Requirements (UFR) as per <strong>ERC</strong> Order dated October 30,<br />

2001, as follows:<br />

TABLE 1<br />

RATE SCHEDULE<br />

Residential Service<br />

Commercial<br />

Street Lights<br />

Industrial 1<br />

Industrial 2<br />

MANSONS classified its existing Industrial customers into two (2)<br />

categories based on load schedule, such as: Industrial 1, which shall be applied<br />

to regular industrial customers; and Industrial 2, which shall be applied to large<br />

industrial customer.<br />

Further, MANSONS incorporated the Government Building customers in<br />

the Residential class, while Hospital customer was included in Industrial 1 class.<br />

MANSONS took into consideration that Government Building and Residential<br />

class, Hospital and Industrial 1 class rate level are almost the same, respectively.<br />

I.A.<br />

Revenue Requirement<br />

MANSONS calculated its Total Revenue Requirement based on test year<br />

2000 using the Return on Rate Base (RORB) methodology. The application<br />

contains assets valued both at historical costs and appraised value. MANSONS’<br />

calculation used the appraised or sound value of assets, as underlying basis for<br />

the formulation and design of the Revised Rate Schedules. The submitted

Page 5 of 35<br />

historical cost of assets, as required in the UFR, was solely for informational<br />

purposes, and not as basis for ratemaking.<br />

On the basis of the submitted schedule (Schedule B), the proposed Total<br />

Revenue Requirement amounted to PhP 82,8<strong>18</strong>,978, which was calculated by<br />

adding the total cost of service and the total return on rate base (computed at 12%<br />

of the rate base). Details as follows:<br />

TABLE 2<br />

Amount<br />

Account Name<br />

(PhP)<br />

Fuel 0<br />

Purchased Power 63,039,806<br />

Payroll 4,924,542<br />

Operation & Maint.enance 6,068,284<br />

Depreciation & Amortization 4,358,090<br />

Income Taxes 0<br />

Other Expense 0<br />

Return On Rate Base 4,428,257<br />

Revenue Requirement 82,8<strong>18</strong>,978<br />

Less: Other Revenue Items 0<br />

Total Revenue Requirement 82,8<strong>18</strong>,978<br />

I.A.1.<br />

Operating Revenue<br />

MANSONS reported a total operating revenue of PhP 65,326,040,<br />

computed as follows:<br />

TABLE 3<br />

Total Revenue<br />

Customer Type<br />

(PhP)<br />

Residential 47,429,048<br />

Commercial 7,848,835<br />

Streetlights 1,701,975<br />

Industrial 1 6,162,131<br />

Industrial 2 2,<strong>18</strong>4,051<br />

Total 65,326,040<br />

I.B.<br />

Rate Base<br />

MANSONS proposed that Schedule B (Restated Value of assets) be used

Page 6 of 35<br />

as basis in the determination of its rate base. Thus, MANSONS utilized the<br />

appraised value of assets as of September 1, 1998 as reported by an<br />

independent appraiser, Asian Appraisal Co., Inc. (AACI) in the rate base<br />

determination. An adjustment was made by MANSONS to reflect additions,<br />

retirements for the period September 2, 1998 to December 31, 2000. The<br />

proposed rate base is as follows:<br />

TABLE 4<br />

Amount<br />

(PhP)<br />

Distribution Plant 64,360,260<br />

General Plant 652,600<br />

Total Plant In Service 65,012,860<br />

Distribution Plant 40,138,830<br />

General Plant 127,160<br />

Total Accum. Depr. 40,265,990<br />

Net Plant In Service 24,746,870<br />

Cash Working Capital 12,155,270<br />

Total Rate Base 36,902,140<br />

I.B.1. Plant in Service<br />

In support of its unbundled rate application, MANSONS submitted for<br />

approval to the <strong>Commission</strong> a report of AACI with respect to the sound value of its<br />

properties existing as of September 1, 1998. Based on the said report,<br />

MANSONS’ assets were appraised based on cost level as of September 1998 at<br />

the prevailing Peso-to-Dollar exchange rate of PhP 43.923 to US$1.00 with total<br />

cost of reproduction, new of PhP 64,263,600 and sound value of PhP 28,355,700,<br />

to wit:<br />

TABLE 5<br />

Particulars<br />

Cost of Reproduction,<br />

New<br />

Sound Value<br />

Electrical Distribution System PhP 63,686,000 PhP 27,821,000<br />

Transportation Equipment 415,000 415,000<br />

Furniture & Office Equipment 162,600 119,700<br />

TOTAL PhP 64,263,600 PhP 28,355,700

Page 7 of 35<br />

I.C.<br />

Weighted Average Cost of Capital (WACC)<br />

MANSONS proposed a Weighted Average Cost of Capital of 12.00% or<br />

equivalent to a return of PhP 4,428,257, computed as follows:<br />

TABLE 6<br />

Component<br />

Amount<br />

As Of<br />

12/31/2000<br />

Component<br />

As % of Total<br />

Component<br />

Cost Of<br />

Capital<br />

Weighted<br />

Cost Of<br />

Capital<br />

Common Equity PhP 30,544,246 100% 12.00% 12.00%<br />

Total PhP 30,544,246 100% 12.00%<br />

Rate Base PhP 36,902,140<br />

Return On Rate Base PhP 4,428,257<br />

I.E.<br />

Rate Design<br />

MANSONS’ proposed rate structure consisted of charges for the following<br />

specific functions: a) Generation/Transmission, b) Distribution, c) Supply, and<br />

d) Metering.<br />

I.E.1.<br />

Generation Charge<br />

In calculating the Generation and Transmission Charge, MANSONS<br />

submitted for approval the following formula:<br />

Generation Charge without Demand Meter:<br />

A 1<br />

------------------- x -------<br />

B-(C+C1+C2) 1-FT<br />

Where:<br />

A= Cost of power for the previous month (exclusive of prompt payment<br />

discounts) less amount recovered from pilferage.<br />

B= kWh purchased for the previous month<br />

C= System loss equivalent to 15% (in kWh)<br />

C1= 1% Company Used (in kWh) or actual whichever is lower<br />

C2= kWh Lifeline consumption for the previous month<br />

FT= Local and National Franchise Tax (2.5%)<br />

Generation Charge with Demand Meter:<br />

A 1<br />

------------------- x -------<br />

B-(C+C1+C2) 1-FT

Page 8 of 35<br />

Where:<br />

A= Cost of power for the previous month (exclusive of Demand charge and prompt<br />

payment discounts and other discounts) less amount recovered from pilferage.<br />

B= kWh purchased for the previous month<br />

C= System loss equivalent to 15% (in kWh)<br />

C1=1% Company Used (in kWh) or actual whichever is lower<br />

C2= kWh Lifeline consumption for the previous month<br />

FT= Local and National Franchise Tax (2.5%)<br />

I.E.2.<br />

Transmission Charge<br />

MANSONS likewise proposed a formula designed to calculate the<br />

Transmission Charge:<br />

A 1<br />

------------------- x -------<br />

B-(C+C1+C2) 1-FT<br />

Where:<br />

A= Cost of transmission for the previous month (exclusive of prompt payment<br />

discounts and other discounts) less amount recovered from pilferage.<br />

B= kWh purchased for the previous month<br />

C= System loss equivalent to 15% (in kWh)<br />

C1=1% Company Used (in kWh) or actual whichever is lower<br />

C2= kWh Lifeline consumption for the previous month<br />

FT= Local and National Franchise Tax (2.5%)<br />

I.E.3.<br />

System Loss<br />

MANSONS proposed a 15% system loss cap to be the recoverable rate for<br />

its system loss through the proposed Generation and Transmission Charge<br />

Formula. Since its franchise area covers mostly agricultural lands, MANSONS<br />

proposed the following technical and non-technical losses per customer class, to<br />

wit:<br />

TABLE 7<br />

Proposed Cap for technical loss:<br />

Customer Class Proposed Ave. Cap/Mo. (%)<br />

Commercial 2<br />

Residential 3<br />

Industrial 1<br />

Street Lights 2<br />

TOTAL 8

Page 9 of 35<br />

TABLE 8<br />

Proposed Cap for non-technical loss:<br />

Customer Class Proposed Ave. Cap/Mo. (%)<br />

Commercial 2<br />

Residential 3<br />

Industrial 0.5<br />

Street Lights 1<br />

Others 0.5<br />

TOTAL 7.0<br />

I.E.4.<br />

Distribution Charge<br />

MANSONS proposed a peso per kilowatt-hour for distribution charge<br />

applicable to all customer classes.<br />

I.E.5.<br />

Supply and Metering Charges<br />

MANSONS proposed a peso per kilowatt-hour for both metering and supply<br />

function applicable to all customer classes.<br />

I.F.<br />

Inter-Class Cross Subsidy<br />

The total revenue requirement for each customer class was compared to<br />

normalized existing rates, which resulted to the following inter-class cross subsidy<br />

calculation:<br />

TABLE 9<br />

Rates per<br />

Revenue<br />

Requirement<br />

Cross<br />

Subsidy<br />

Customer<br />

Class<br />

Actual<br />

Average Rate<br />

Average<br />

Increase<br />

Total<br />

Residential 4.9522 0.5823 5.5345 5.7329 (0.1984)<br />

Commercial 5.0978 0.5823 5.6801 5.0868 0.5933<br />

Streetlights 3.9816 0.5823 4.5639 4.8947 (0.3308)<br />

Industrial 1 5.2125 0.5823 5.7948 5.1429 0.65<strong>18</strong><br />

Industrial 2 5.0917 0.5823 5.6739 5.3073 0.3667<br />

Total 4.9921 0.5823 5.5744 5.5744

Page 10 of 35<br />

I.G.<br />

Lifeline Rate<br />

MANSONS proposed a rate of PhP 1.7865 per kWh for its lifeline<br />

customers computed based on its proposed Distribution Charges. MANSONS’<br />

basis for determining the consumption level for its lifeline customers is as follows:<br />

TABLE 10<br />

Quantiy Type of Load Watts<br />

1 Incandescent Bulb 40<br />

1 20 Watts Fluorescent Lamp 32<br />

1 Convenience Outlet 13<br />

Total 85<br />

With regard to the recovery of loss in revenue due to lifeline rate,<br />

MANSONS proposed the following:<br />

1. Any loss in revenue due to lifeline rate will be recovered thru its<br />

proposed Generation Charge Formula.<br />

2. If the <strong>Commission</strong> will not consider the said formula, any loss in<br />

revenue will be recovered by charging all customers by peso per<br />

kilowatt-hour for lifeline loss, computed as follows:<br />

TABLE 11<br />

Computed Residential Rate PhP 5.7329<br />

Less: Proposed Lifeline Rate Subsidy PhP 1.7865<br />

Total PhP 3.9464<br />

Multiply: kWh sold by lifeline customer/yr. 88,680<br />

Revenue loss PhP 349,967<br />

Divide: Total kWh sold 13,277,204<br />

Less: kWh sold by lifeline customer 88,680<br />

13,<strong>18</strong>8,524<br />

Recovery for lifeline loss:<br />

Revenue Loss 349,967<br />

KWh 13,<strong>18</strong>8,524<br />

= PhP 0.0265/kWh<br />

I.G.<br />

Other Charges/<strong>No</strong>n-Recurring Rates<br />

MANSONS’ proposed the following Other Charges and/or non-recurring

Page 11 of 35<br />

charges, to wit:<br />

TABLE 12<br />

Other Charges<br />

Amount (PhP)<br />

Reconnection at Service Drop 20.00<br />

Reconnection due to withdrawal of meter 20.00<br />

Transfer of meter location 20.00<br />

Replacement of meter 20.00<br />

New Connection – Single Phase Meter 20.00<br />

New Connection – Three Phase Meter 75.00<br />

Relocation of Secondary Pole<br />

Actual cost of labor<br />

Bump damaged pole due to accident<br />

Actual cost of labor<br />

Calibration of watt hour meter (as requested by 20.00<br />

consumer)<br />

Installation/Dismantling of transformer (private Actual cost of labor<br />

construction)<br />

Calibration of Industrial/Commercial Meter<br />

(Polyphase)<br />

Based on <strong>ERC</strong><br />

calibration rates<br />

Reconnection, transfer of line and meter 25.00<br />

Installation of transformer<br />

50.00/kVa<br />

Interruption Charge 2,500.00<br />

Based on <strong>ERC</strong><br />

Calibration of Polyphase Industrial/Commercial calibration rates<br />

Calibration Fee residential customer meter 20.00<br />

II.<br />

COMMISSION DISCUSSIONS AND CONCLUSIONS:<br />

In reaching the conclusion herein, the <strong>Commission</strong> took into consideration<br />

the documents as well as the comments and issues presented by the applicant,<br />

intervenor, and other interested parties who submitted their respective positions<br />

on the instant application.<br />

II.A.<br />

Determination of the Total Revenue Requirement<br />

II.A.1.<br />

Test Year<br />

The <strong>Commission</strong> finds MANSONS proposal to use the test year 2000 in its<br />

unbundled rate application acceptable since it is consistent with Rule 15 Section 6<br />

(c) of the Implementing Rules and Regulations (IRR) of R. A. 9136. Therefore,<br />

the discussions and conclusions that follow are based on Schedule B, “Revalued<br />

Cost by Function” (Cost of Service by Function-Historical Test Year).

Page 12 of 35<br />

II.A.2.<br />

Generation and Transmission Costs<br />

Generation Cost<br />

The <strong>Commission</strong> updated the generation cost based on the most recent<br />

approved NPC rate, i.e., <strong>ERC</strong> <strong>Case</strong> <strong>No</strong>. 2003-291 (In the Matter of the Application<br />

for the Approval of the Revised Unbundled Generation Tariffs, National Power<br />

Corporation (NPC) and Power Sector Assets and Liabilities Management<br />

(PSALM) – Applicants) Order dated September 29, 2003.<br />

<strong>No</strong>tably, the<br />

<strong>Commission</strong> approved the adoption of the Incremental Currency Exchange Rate<br />

Adjustment (ICERA) in <strong>ERC</strong> <strong>Case</strong> <strong>No</strong>. 2003-498, Order dated December 4, 2003<br />

(NPC and PSALM – applicants). The <strong>Commission</strong> directed NPC and PSALM to<br />

refund to its customers the Deferred Accounting Adjustment (DAA) and FOREX<br />

Correction for Luzon amounting to PhP (0.0065) per kWh within a period of six<br />

months starting December 2003 to May 2004.<br />

The total purchased power cost, as presented in the amended application<br />

amounting to PhP 63,039,806 was adjusted to reflect the following:<br />

a) The <strong>Commission</strong> decided to retain the system loss cap prescribed<br />

under Rule IX Section 1 of the Implementing Rules and Regulation of<br />

Republic Act <strong>No</strong>. 7832 pending the conduct of a comprehensive study<br />

on the matter. Hence, the <strong>Commission</strong> used the maximum allowable<br />

cap for system loss at 9.5% instead of the 15% proposed herein by<br />

MANSONS and actual company use of 0.9542% for the year 2000.<br />

(See further discussion on Section II.J.3).

Page 13 of 35<br />

b) The <strong>Commission</strong> also used annualization in calculating the kilowatt-hour<br />

purchase power cost. This is calculated as the sum of the products of<br />

the average kilowatt-hour consumption for each rate class and the yearend<br />

number of customers for each rate class; and<br />

c) Since power rates are to be applied prospectively, the <strong>Commission</strong> also<br />

updated the purchased power costs to the most recent levels available.<br />

Based on December 2003 data submitted by MANSONS to the<br />

<strong>Commission</strong>, MANSONS buys 100% of its power requirements from NPC. As<br />

such, the generation cost as computed by the <strong>Commission</strong> reflects the cost of<br />

electric power bought from NPC as of supply month December 2003. The<br />

resulting total adjusted purchased power cost amounting to PhP 54,750,234 for<br />

the test year 2000 was computed as follows:<br />

TABLE 13<br />

Purchased power cost submitted by MANSONS<br />

(inclusive of transmission component) PhP 63,039,806<br />

Adjustment due to update of purchased power<br />

costs 4,424,479<br />

Total PhP 67,464,285<br />

Less: Excess system loss 12,714,051<br />

Total Purchased Power Cost included in<br />

Revenue Requirement PhP 54,750,234<br />

Transmission Cost<br />

The <strong>Commission</strong>’s Decision in <strong>ERC</strong> <strong>Case</strong> <strong>No</strong>. 2001-901 dated June 26,<br />

<strong>2002</strong> and Order dated September 20, <strong>2002</strong> set the transmission charges for the<br />

TRANSCO without any provision for an automatic adjustment thereof. Since the<br />

transmission rates to be paid by MANSONS are fixed, it is the decision of the<br />

<strong>Commission</strong> to likewise fix the unbundled transmission rates to be billed to endusers.<br />

The transmission charges approved for billing by MANSONS have been

Page 14 of 35<br />

calculated based on the approved TRANSCO rates, which include cross subsidy<br />

elements to be phased out over a three-year period.<br />

System Loss<br />

A separate charge to account for allowable system loss shall likewise be<br />

provided. The <strong>Commission</strong> decided to retain the system loss cap prescribed<br />

under Rule IX Section 1 of the I.R.R. of R.A. 7832 pending the conduct of a<br />

comprehensive study on the matter. Hence, the <strong>Commission</strong> used the maximum<br />

allowable cap for system loss at 9.5% or actual, whichever is lower.<br />

Based on the new generation and transmission charges, as well as the<br />

allowable system loss, the <strong>Commission</strong> has determined MANSONS unbundled<br />

generation, transmission and recoverable system loss as follows:<br />

TABLE 14<br />

Generation Charge PhP 34,067,359<br />

Transmission Charge 12,802,791<br />

Recoverable System Loss 7,880,084<br />

Total PhP 54,750,234<br />

MANSONS approved generation charge shall remain fixed until changes in<br />

NPC’s generation rate are approved and authorized by the <strong>Commission</strong> pursuant<br />

to its Order dated February 24, 2003, <strong>ERC</strong> <strong>Case</strong> <strong>No</strong>. 2003-44 (GRAM) and <strong>ERC</strong><br />

<strong>Case</strong> <strong>No</strong>. 2003-498 (ICERA), Order dated December 4, 2003. In view thereof, the<br />

<strong>Commission</strong> does not foresee the need for MANSONS to continue to implement<br />

its Purchased Power Adjustment (PPA) clause.<br />

Towards this end, the<br />

<strong>Commission</strong> hereby directs MANSONS to discontinue the implementation of its<br />

PPA clause upon the effectivity of the herein approved unbundled rates.

Page 15 of 35<br />

II.A.3. Operation and Maintenance (Less Power Cost & Payroll)<br />

The general criteria in the evaluation of expenses to be allowed for<br />

recovery are: (1) that the expense is a requisite of, or necessary in the operation<br />

of the utility; (2) it is recurring; and (3) it redounds to the benefit of the utility’s<br />

customers (Public Service <strong>Commission</strong> [PSC] Decision in <strong>Case</strong>s <strong>No</strong>s. 85889,<br />

85890 and 89893). The <strong>Commission</strong> enjoins MANSONS to incur only “prudent<br />

and reasonable costs” for inclusion in the determination of retail rates. While a<br />

distribution utility enjoys the benefit of passing its costs of purchased power and<br />

other reasonable costs to the consumer, it is obligated as a public utility to ensure<br />

that its costs of operations including payroll are kept at a minimum. The<br />

distribution utility must bear in mind that as a service-oriented company, its<br />

mandate is to advocate and transact judiciously for and in behalf of its consumers.<br />

“Reasonable costs” refers to the costs of those goods and services which,<br />

while may not be the lowest in price, need to be incurred with consideration of<br />

quality, efficiency, reliability and security, which are characteristics of the service<br />

delivered by the distribution utility. “Prudent costs” demand that the utility ensures<br />

that its purchases of goods and services are at their minimum, without sacrificing<br />

the foregoing characteristics. When making a purchase or executing a contract, a<br />

utility cannot simply rely on its right to pass on its costs to its consumers. As<br />

such, the <strong>Commission</strong>, in fulfillment of the policy of the EPIRA to establish a<br />

regime of free and fair competition and full public accountability to achieve greater<br />

operational and economic efficiency, enjoins MANSONS to institute and report to<br />

the <strong>Commission</strong> their respective policies and procedures for cost-cutting and the<br />

transparent and competitive procurement of goods and services.

Page 16 of 35<br />

MANSONS customers have a right to receive safe, reliable, and adequate<br />

service at a reasonable rate. To this end, MANSONS should view a petition for an<br />

increase in rates to be the last recourse. In future filings, MANSONS should be<br />

reminded that it has the burden of proving that all reasonable and appropriate cost<br />

cutting measures have been taken before resorting to a petition to increase rates.<br />

Operations and Maintenance account was adjusted to PhP 4,752,499 after<br />

considering adjustment of PhP 1,315,785, computed as follows:<br />

TABLE 15<br />

O & M per MANSONS PhP 6,068,284<br />

Adjustments:<br />

Expenses excluded for ratemaking purposes PhP (321,461)<br />

Franchise Tax (separate item) (994,324) (1,315,785)<br />

Adjusted O & M PhP 4,752,499<br />

Adjustments<br />

The <strong>Commission</strong> finds some expenses to be unnecessary in the provision<br />

of MANSONS electric service and therefore excluded the same for ratemaking<br />

purposes, as follows:<br />

TABLE 16<br />

Particulars<br />

Amount<br />

Donations PhP 115,326<br />

Interest Expense 206,135<br />

Total Expenses excluded for<br />

ratemaking purposes PhP 321,461<br />

Franchise tax shall appear as a separate line item on the customers’ bills<br />

as percentage of the total monthly electricity charges. Given this rate design, it is<br />

appropriate to remove the amount of PhP 994,324 associated with franchise taxes<br />

from the revenue requirement as this is just a pass through item.<br />

For future rate cases, MANSONS will continue to be required to make full<br />

disclosures of all it’s O & M expenses in order for the <strong>Commission</strong> to determine

Page 17 of 35<br />

the prudence of its expenditures. Unless otherwise justified by MANSONS,<br />

expenses found to be unreasonably incurred shall not be allowed by the<br />

<strong>Commission</strong> as part of its recoverable costs to be passed on to MANSONS endusers.<br />

II.A.4.<br />

Depreciation and Amortization<br />

MANSONS is required to set up a depreciation fund each year<br />

corresponding to the whole amount of depreciation that it has recorded on its<br />

books. The setting up of this fund should be done on a monthly basis<br />

corresponding to the monthly depreciation. MANSONS will be required to strictly<br />

account for the expenditures out of this fund which should be used solely for<br />

investment in electric plant. The utility is free to withdraw funds from this account<br />

at any time but all withdrawals should be reported to the <strong>Commission</strong> within thirty<br />

(30) days specifying the use of the funds. This report should be consolidated with<br />

the monthly reportorial requirement (M-001 & M-002).<br />

II.D. Rate Base<br />

II.D.1. Net Plant in Service<br />

The <strong>Commission</strong> has determined MANSONS’ net plant in service as of<br />

December 31, 2000 considered in this case as follows:<br />

TABLE 17<br />

Plant, Property & Equipment<br />

Sound Value<br />

Assets as of September 1, 1998 per Appraisal Report PhP 28,355,700<br />

Add (Deduct) Adjustment :<br />

Addition/(Retirement) from Sept. 2, 1998-Dec.2000 749,260<br />

Depreciation Expense from Sept. 2,1998-Dec. 2000 (4,358,090)<br />

Adjusted Net Plant in Service as of Dec. 31, 2000 PhP 24,746,870<br />

The <strong>Commission</strong> considered appraisal of assets conducted by AACI of<br />

MANSONS properties and equipment existing as of September 1, 1998 with a

Page <strong>18</strong> of 35<br />

total value of PhP 64,263,600 as cost of reproduction, new and PhP 28,355,700<br />

as sound value, as shown in Table 5 of this Decision.<br />

II.D.2.<br />

Allowance for Cash Working Capital<br />

Working capital is money a business must have available to meet payroll<br />

and expenses until customers have paid for the service or product. Utilities are<br />

usually allowed, as part of their rate base, an amount for working capital to cover<br />

expenses during the time it takes for the customers to use the service, be billed<br />

for it and collect payments.<br />

MANSONS has included an amount equal to two (2) months cash<br />

operating and maintenance expenses including purchased power costs as the<br />

allowance for cash working capital.<br />

The cash working capital allowance included in the rate base should<br />

approximate the actual cash requirements of MANSONS based on the estimated<br />

net lag in its cash flow. In order to refine the application of the formula used in<br />

past rate proceedings, a more detailed review of the actual lag in cash flow<br />

associated with the payments for purchased power and the inflow of cash from<br />

MANSONS customers was undertaken. With respect to the outflow of cash<br />

associated with the payments for purchased power, it was determined that the<br />

time from the provision of service to the outflow of funds can be calculated as<br />

follows:<br />

15 days One-half of the billing cycle<br />

5 days Meter reading and bill preparations<br />

30 days Approximate time before payment is due<br />

50 days Total

Page 19 of 35<br />

Therefore, MANSONS has an average of approximately fifty (50) days from<br />

the time service is provided until payment is due. With respect to the collection of<br />

funds from its customers, it was determined that the time lag from the provision of<br />

service to the inflow of funds can be calculated as follows:<br />

15 days One-half of the billing cycle<br />

10 days Meter reading, bill preparation<br />

10 days Required time to collect the customer’s bill<br />

without disconnection<br />

5 days Processing time<br />

40 days Total<br />

Therefore, MANSONS waits for an average of approximately forty (40)<br />

days before it receives payment for the services provided.<br />

Based on MANSONS current billing and collection practices, there appear<br />

to be no cash working capital requirement associated with purchased power. The<br />

only potential finance costs associated with purchased power would be costs<br />

caused by customers who do not pay their bills in accordance with MANSONS<br />

collection policies. MANSONS customers who do pay on time should not be<br />

penalized because other customers failed to comply with MANSONS payment<br />

schedule. If additional finance costs are incurred because of late payment of bills,<br />

these costs should be recovered in the form of penalties for late payment.<br />

Therefore, the formula for the calculation of the cash working capital allowance is<br />

modified by excluding purchased power costs.<br />

The adjusted Cash Working Capital allowed by the <strong>Commission</strong> was<br />

computed as follows:

Page 20 of 35<br />

TABLE <strong>18</strong><br />

Adjusted O & M PhP 68,785,365<br />

Taxes & <strong>No</strong>n-cash items<br />

Taxes Other than Income Tax<br />

106,685<br />

Depreciation<br />

4,358,090<br />

Purchased power cost<br />

54,750,234<br />

Total Taxes & <strong>No</strong>n-Cash Items PhP 59,215,009<br />

Total O&M , net of Cash & <strong>No</strong>n-Cash Item PhP 9,570,356<br />

Cash Working Capital – O&M (2 mos.) PhP 1,595,059<br />

Adjusted Power Cost PhP 54,750,234<br />

Cash Working Capital – Power Cost (0) 0<br />

Total Cash Working Capital PhP 1,595,059<br />

II.D.3.<br />

Summary of Rate Base<br />

The following compares the rate base submitted by MANSONS with that<br />

approved by <strong>ERC</strong>.<br />

TABLE 19<br />

Per MANSONS Per <strong>ERC</strong><br />

Net Plant In Service PhP 24,746,870 PhP 24,746,870<br />

Cash Working Capital 12,155,270 1,595,059<br />

Total Rate Base PhP 36,902,140 PhP 26,341,929<br />

II.E.<br />

Rate of Return<br />

The current form of rate regulation practiced for the privately owned electric<br />

utilities is a cost based method known as the rate of return on rate base (RORB)<br />

methodology. Power rates are set to recover cost of service prudently incurred<br />

plus a reasonable rate of return on rate base. The rate of return pertains to the<br />

percentage which when multiplied by the authorized rate base, provides a return<br />

that will fairly compensate the company for the risk inherent to the investment of<br />

capital. This simply means that a regulated utility is allowed to set rates which will<br />

cover operating costs and provide an opportunity to earn a reasonable rate of<br />

return on the assets utilized in the business.

Page 21 of 35<br />

On the basis of current jurisprudence, the <strong>Commission</strong> has determined that<br />

the 12% rate of return will be maintained in this case but the income tax thereon<br />

will not be allowed as operating expense. Thus, the 12% rate of return is a pretax<br />

rate of return which is equivalent to PhP 3,161,032, computed as follows:<br />

TABLE 20<br />

Adjusted Rate Base PhP 26,341,929<br />

Rate of Return 12%<br />

Return On Rate Base PhP 3,161,032<br />

The <strong>Commission</strong> intends to adopt a new internationally accepted method of<br />

rate regulation known as Performance-Based Regulation. The treatment of<br />

income tax in this new method may be different from the present RORB method.<br />

II.F.<br />

Revenue Requirement Summary<br />

On<br />

the basis of the foregoing discussion, the <strong>Commission</strong> after<br />

considering adjustments of<br />

PhP 10,872,582 approved a total revenue<br />

requirement of PhP 71,946,397 equivalent to OATA of PhP 0.0344 per kWh or<br />

0.66% increase from its existing average rate.<br />

TABLE 21<br />

Per<br />

MANSONS<br />

Adjustments<br />

<strong>ERC</strong><br />

Adjusted<br />

<strong>ERC</strong><br />

Fuel PhP 0 PhP 0 PhP 0<br />

Purchased Power 63,039,806 (8,289,572) 54,750,234<br />

Payroll 4,924,542 0 4,924,542<br />

Operation & Maintenance 6,068,284 (1,315,785) 4,752,499<br />

Depreciation & Amortization 4,358,090 0 4,358,090<br />

Return on Rate Base 4,428,257 (1,267,225) 3,161,032<br />

Total Revenue Requirement PhP 82,8<strong>18</strong>,978 PhP (10,872,582) PhP 71,946,397<br />

Adjusted Revenue (2000) PhP 71,475,841<br />

Increase(Decrease) PhP 470,556<br />

Annualized kWh Sales 13,683,319<br />

Required Increase PhP/kWh 0.0344<br />

The overall average tariff adjustment (OATA) is a measurement tool based<br />

on the formula: (Total Revenue Requirement less Existing Revenue) divided by

Page 22 of 35<br />

kilowatt-hour sales). This measurement is not meant to refer to any specific<br />

customer class. MANSONS proposed an OATA of PhP 0.5823 per kWh.<br />

II.G.<br />

Adjusted Operating Revenue<br />

The<br />

<strong>Commission</strong> adjusted MANSONS actual operating revenue to<br />

PhP 71,475,841, computed as follows:<br />

TABLE 22<br />

MANSONS actual operating revenue PhP 65,326,040<br />

Add/(Deduct):<br />

Franchise Tax (994,324)<br />

Addtl. revenue due to increase in sales 2,789,899<br />

Additl. Revenue due to increase in power cost 4,354,226<br />

Total Adjusted Operating Revenue PhP 71,475,841<br />

II.I.<br />

Billing Determinants and Customer Class Allocation<br />

The <strong>Commission</strong> concurs with MANSONS billing determinants and<br />

allocation factors except for the billing determinant and allocation factor used for<br />

energy related costs.<br />

The <strong>Commission</strong> allocated the computed revenue<br />

requirement using its existing customer class.<br />

The <strong>Commission</strong> believes that any energy related costs should be<br />

allocated based on annualized sales. Annualized sales were derived by<br />

multiplying year-end number of customers with average annual kWh usage for<br />

each customer class. This was performed to project for the future kWh sales for<br />

the development of a more appropriate allocation factors and billing determinants<br />

for each customer class. With the annualized sales per customer class, the<br />

computed adjusted kilowatt-hour sold was 13,683,319.

Page 23 of 35<br />

The <strong>Commission</strong> opines that in theory, the most appropriate way to allocate<br />

costs among customer classes is through the use of the cost causation principles.<br />

Thus, the <strong>Commission</strong> intends, through future proceedings to move even further<br />

towards uniform definitions of customer classes based on cost causation<br />

characteristics. However, the <strong>Commission</strong> believes that such a change would<br />

best be accomplished through the issuance of guidelines of general applicability to<br />

all utilities. Furthermore, R.A. 9136 requires the identification and removal of<br />

interclass cross-subsidies. Substantive change in customer classes at this time<br />

prevents precise calculation of cross-subsidy in existing rates. Therefore, no<br />

changes in customer class allocations are ordered for MANSONS at this time.<br />

II.J.<br />

Design and Calculation of Charges<br />

II.J.1.<br />

Generation Charge<br />

The <strong>Commission</strong> updated the generation cost based on the most recent<br />

approved NPC rate, i.e., <strong>ERC</strong> <strong>Case</strong> <strong>No</strong>. 2003-291, Order dated September 29,<br />

2003. <strong>No</strong>tably, the <strong>Commission</strong> approved the adoption of the ICERA under <strong>ERC</strong><br />

<strong>Case</strong> <strong>No</strong>. 2003-498, Order dated December 4, 2003. The <strong>Commission</strong> directed<br />

NPC and PSALM to refund to its customers the DAA and FOREX Correction for<br />

Luzon amounting to PhP (0.0065) per kWh within a period of six months starting<br />

December 2003 to May 2004.<br />

The NPC’s approved rate will remain fixed until changes are authorized by<br />

the <strong>Commission</strong>.<br />

This eliminates the need for future Purchased Power<br />

Adjustment.

Page 24 of 35<br />

The <strong>Commission</strong> has developed a new recovery mechanism designed to<br />

replace the purchased power adjustment clauses being used by the power<br />

utilities. The <strong>Commission</strong> has promulgated the Implementing Guidelines on the<br />

Generation Rate Adjustment Mechanism (GRAM) effective February 24, 2003. In<br />

view thereof, the <strong>Commission</strong> does not foresee the need for the Purchased Power<br />

Adjustment (PPA) clause. Towards this end, the <strong>Commission</strong> hereby directs<br />

MANSONS to discontinue implementation of its PPA upon effectivity of the herein<br />

approved unbundled rates.<br />

II.J.2.<br />

Transmission Charge<br />

The <strong>Commission</strong>’s decision in <strong>ERC</strong> <strong>Case</strong> <strong>No</strong>. 2001-901 and the<br />

<strong>Commission</strong>’s Order dated September 20, <strong>2002</strong> fixed the transmission charges for<br />

the TRANSCO without any provision for automatic adjustment thereof. Since the<br />

transmission rates to be paid by MANSONS are fixed, it is the decision of the<br />

<strong>Commission</strong> to likewise fix the unbundled transmission rates billed to its end-use<br />

customers.<br />

The transmission charge shall be billed on a fixed rate per kilowatt-hour for<br />

all end-users except for Industrial customers. The transmission charge for<br />

Industrial customers shall be billed using a combination of a fixed rate per kilowatt<br />

(kW) and a rate per kilowatt-hour (kWh).<br />

In consonance with the gradual phase-out of the intra-grid subsidies being<br />

billed by TRANSCO, the <strong>Commission</strong> hereby sets the transmission charges for<br />

the succeeding years, as follows:

Page 25 of 35<br />

TABLE 23<br />

Period Charges Residential Commercial<br />

Street<br />

Lights Industrial Hospital<br />

Govt.<br />

Bldg.<br />

Oct.2003 - Demand (PhP/kW)<br />

138.07<br />

Sept .2004 Transmission (PhP/kWh) 0.9667 0.8934 0.8301 0.4013 0.9036 0.9133<br />

Oct.2004 - Demand (PhP/kW)<br />

157.87<br />

Sept. 2005 Transmission(PhP/kWh) 1.1053 1.0215 0.9491 0.4588 1.0332 1.0442<br />

Oct.2005- Demand (PhP/kW)<br />

177.66<br />

Sept. 2006 Transmission(PhP/kWh) 1.2439 1.1496 1.0681 0.5163 1.1627 1.1751<br />

II.J.3.<br />

System Loss Charge<br />

The <strong>Commission</strong> defines System Loss for utilities to include technical loss<br />

and administrative loss or the utility’s use of power for its own operations.<br />

The <strong>Commission</strong> approves the recovery of allowed system loss through the<br />

establishment of a separate System Loss Charge. The system loss charge shall<br />

vary from one customer class to another depending on their respective<br />

contributions to the system loss. The allowed system loss is equal to the actual<br />

system loss for the test year or the existing system loss cap prescribed in R.A.<br />

7832 whichever is lower.<br />

The <strong>Commission</strong> believes that the present cap on System Loss of 9.5%<br />

should be used in the calculation of revenue requirements at this time. This<br />

would however be subject to change upon the approval of a new policy by the<br />

<strong>Commission</strong>. The actual system loss or cap of 9.5% plus 1% of company use or<br />

actual whichever is lower shall be deducted from total power cost and to be billed<br />

separately as System Loss Charge.<br />

II.J.4.<br />

Distribution Charge<br />

The distribution charge shall be billed on a fixed rate per kilowatt-hour<br />

(kWh) for all end-users except for Industrial customers. The distribution charge

Page 26 of 35<br />

for Industrial customers shall be billed using a combination of a fixed rate per<br />

kilowatt (kW) and a rate per kilowatt-hour (kWh).<br />

Relevant to distribution charge, MANSONS’ proposed distribution wheeling<br />

rates comprised of its proposed distribution and supply charges. The <strong>Commission</strong><br />

believes that wheeling rates are parallel to the cost of service functionalized under<br />

Distribution. Thus, the <strong>Commission</strong> orders that the Distribution Charge provided<br />

in the Rate Schedules be likewise utilized as Distribution Wheeling Charges<br />

available to the future contestable market.<br />

The <strong>Commission</strong>’s decision to allow a distribution utility to avail of the<br />

Distribution Wheeling Charges of another distribution utility is based on the<br />

general intent of R.A. 9136 to promote a competitive generation market.<br />

Distribution utilities that currently or in the near future rely in full or in part on the<br />

distribution facilities of another distribution utility should not be held captive by the<br />

other distribution utility in the purchase of unbundled generation. Distribution<br />

utilities are, therefore, prohibited from bundling or tying the sale of generation or<br />

purchased power with the sale of unbundled distribution wheeling service.<br />

II.J.5.<br />

Metering and Supply Charges<br />

The <strong>Commission</strong> acknowledges that cost-causation rate design principles<br />

suggest the recovery of customer-related costs through fixed monthly charges. In<br />

addition to this cost of service principle, however, the <strong>Commission</strong> must also<br />

consider rate design impacts across the spectrum of customers within each rate<br />

class. Although RA 9136 requires the removal of inter-class cross subsidies, the<br />

law does not require removal of intra-class cross-subsidies. The <strong>Commission</strong> has<br />

the flexibility to consider other factors in determining rate design for a particular

Page 27 of 35<br />

class of customers.<br />

Therefore to mitigate the impact on below-average<br />

consumption of residential end-users, the <strong>Commission</strong> orders MANSONS to use a<br />

combination of peso per customer per month and peso per kilowatt-hour for the<br />

metering function. On the other hand, the <strong>Commission</strong> orders MANSONS to use<br />

peso per kilowatt-hour rate for the supply function. All other end-users except for<br />

Street Lights shall be charged fixed monthly customer charge for both metering<br />

and supply functions. Street Lights will be charged fixed monthly customer charge<br />

for supply function only.<br />

II.J.6.<br />

Franchise Taxes<br />

Franchise taxes shall appear as a separate line item on the customers’<br />

bills. Given this rate design, it is appropriate to remove test year amounts<br />

associated with franchise taxes from the revenue requirement used to calculate<br />

other recurring electricity rates.<br />

Pending issuance of guideline on this issue by the Department of Finance<br />

(DOF), MANSONS is in the meantime directed to use the formula below in<br />

calculating franchise taxes.<br />

Franchise Tax:<br />

Total Power Bill x FTx1,y<br />

Where: FTx = National franchise tax of 2%<br />

Fty = Applicable local franchise tax<br />

II.K. Cross Subsidy Removal<br />

The inter-class cross subsidies in existing rates are as follows:

Page 28 of 35<br />

TABLE 24<br />

Total Residential Commercial Streetlights Industrial Hospital Govt.Bldg.<br />

New Cost-<br />

Based Revenue 71,946,397 54,100,416 7,895,595 1,747,766 7,027,805 486,349 688,466<br />

Existing Rates<br />

Revenue 71,475,841 51,889,384 8,436,324 1,795,401 8,093,882 535,155 725,695<br />

Total Change in<br />

Revenue 470,556 2,211,032 (540,729) (47,635) (1,066,077) (48,806) (37,229)<br />

% Change in<br />

Revenue 0.6583%<br />

<strong>No</strong>rmalized<br />

Revenue 71,946,397 52,230,993 8,491,863 1,807,221 8,147,168 538,678 730,472<br />

Inter-class<br />

Cross Subsidy 0 (1,869,423) 596,268 59,456 1,119,362 52,329 42,008<br />

Class Billing<br />

Determinants 13,683,319 10,000,842 1,578,998 380,481 1,482,377 98,449 142,172<br />

(in kWh)<br />

Inter-class<br />

Cross Subsidy<br />

Rates (PhP/Kwh)<br />

(0.<strong>18</strong>69) 0.3776 0.1563 0.7551 0.5315 0.2955<br />

Section 74 of R.A. 9136 and Rule 16 Section 16, Section 5 of the<br />

Implementing Rules and Regulation thereof provide that <strong>ERC</strong> shall prescribe a<br />

scheme for phasing out all cross subsidies including subsidies within Grids,<br />

between Grids, and between classes of end-users. The phasing out period shall<br />

not exceed three (3) years from the establishment of the Universal Charge, which<br />

may be extendible for a maximum period of one (1) year subject to certain<br />

conditions.<br />

The <strong>Commission</strong> approved the cross subsidy removal scheme for the<br />

TRANSCO in its Decision dated June 26, <strong>2002</strong> in <strong>ERC</strong> <strong>Case</strong> <strong>No</strong>. 2001-901 which<br />

impacts the unbundled transmission rates for MANSONS end users. This impact<br />

is reflected in the three-year schedule for unbundled transmission charges<br />

provided in Section II.J.2 above.<br />

In the instant case, the <strong>Commission</strong> will order the cross subsidy removal<br />

process at a later date following the establishment of the Universal Charge. Until

Page 29 of 35<br />

such time, MANSONS will continue to charge the inter-class cross subsidy rates<br />

set forth above.<br />

II.L.<br />

Lifeline Rate<br />

Section 4 (hh) of R.A. 9136 defines Lifeline Rate as the subsidized rate<br />

given to low-income captive market end-users who cannot afford to pay at full<br />

cost. Pursuant to Section 73 of R.A. 9136, the <strong>Commission</strong> hereby sets the level<br />

of lifeline consumption and rate applicable to MANSONS.<br />

In determining the lifeline level of consumption to be provided to the<br />

marginalized end-users, the <strong>Commission</strong> calculated the probable load<br />

requirement of typical low-income consumers by two (2) lighting facilities at 20<br />

watts each and a 50-watt Radio that are being used at reasonable number of<br />

hours. Thus, the <strong>Commission</strong> sets the lifeline consumption maximum level of 50<br />

kilowatt-hours for MANSONS. The <strong>Commission</strong> considers the impact that the<br />

subsidized Lifeline Rates will have on other end-users who must carry the costs<br />

associated with such subsidy. This fact, combined with the desire to maximize the<br />

benefit to as many marginalized end-users as possible, has led the <strong>Commission</strong><br />

to adopt the following graduated scale for lifeline discount for MANSONS. The<br />

graduated scale is also based on the recognition that individual end-user<br />

consumption may likely vary from month to month.<br />

TABLE 25<br />

KWh Consumption % Lifeline Discount<br />

10 kWh and below 30%<br />

11 – 20 kWh 25%<br />

21 – 30 kWh 20%<br />

31 – 40 kWh 15%<br />

41 – 50 kWh 10%

Page 30 of 35<br />

MANSONS shall apply these discounts to the following residential charges:<br />

Generation, Transmission, Distribution, Supply, Metering and System Loss. In a<br />

given billing period, an end-user at any of the above-consumption levels shall be<br />

given the specified corresponding discount on each of these rate components. An<br />

end-user with a level of consumption exceeding 50 kWh in a particular billing<br />

period shall not be entitled to any discounted lifeline rate for said period.<br />

The cost of subsidy to lifeline end-users shall be passed on to all nonlifeline<br />

end users. For MANSONS, the lifeline discounts result in a Subsidy on<br />

Lifeline by other end-users equal to PhP 0.0849/kWh.<br />

II.M.<br />

Other Charges/<strong>No</strong>n-Recurring Rates<br />

MANSONS existing Other Charges were considered in the determination of<br />

the revenue requirement. The corresponding revenue derived from these charges<br />

were appropriately deducted from the determination of the revenue requirement<br />

allowed to MANSONS.<br />

The Other Charges of MANSONS are hereby pegged at their existing<br />

levels until such time that the <strong>Commission</strong> sets new rates on the same. Further,<br />

MANSONS is ordered to make a compliance filing on its Other Charges a year<br />

from date of this Decision using a format to be prescribed by the <strong>Commission</strong>.<br />

The compliance filing for approval of Other Charges shall include rates that<br />

are cost-based as well as all supporting cost justification for the rates, including<br />

but not limited to the amount of actual time and wages of employees performing<br />

each task encompassed by each type of Other Charges.

Page 31 of 35<br />

II.N.<br />

Estimated Impact on Average Residential Consumer<br />

A comparison of the estimated impact of all adjustments on the revenue<br />

requirement on the monthly bill of a residential end-user consuming 99 kWh a<br />

month using rates based on MANSONS actual existing rates as of December<br />

2003 against the unbundled rates approved by the <strong>Commission</strong> is shown below:<br />

TABLE 26<br />

RESIDENTIAL<br />

Consuming 99 kWh Peso/kWh Amount Peso/kWh Amount<br />

Basic Charge<br />

3.1912 315.92 Generation Charge<br />

Transmission Charge<br />

2.4897<br />

0.9667<br />

System Loss Charge<br />

0.5759<br />

PPA<br />

Power Act Reduction<br />

2.1711<br />

(0.30)<br />

214.94<br />

(29.70)<br />

Distribution Charge<br />

Supply Charge<br />

1.0331<br />

0.1538<br />

Metering Charge:<br />

Retail Customer Charge/Mo.<br />

5.00<br />

Metering System Charge 0.1292<br />

Inter-Class Cross Subsidy Charge (0.<strong>18</strong>69)<br />

Lifeine Rate Subsidy<br />

0.0849<br />

Power Act Reduction<br />

(0.30)<br />

246.48<br />

95.70<br />

57.01<br />

102.27<br />

15.23<br />

5.00<br />

12.79<br />

8.41<br />

(<strong>18</strong>.51)<br />

(29.70)<br />

SUB TOTAL<br />

501.16<br />

SUB TOTAL<br />

494.69<br />

Universal Charge<br />

Missionary Electrification<br />

Environmental Charge<br />

0.0373<br />

0.0025<br />

3.69<br />

0.25<br />

Universal Charge<br />

Miissionary Electrification<br />

Environmental Charge<br />

Franchise Tax 2.5%<br />

0.0373<br />

0.0025<br />

3.69<br />

0.25<br />

12.37<br />

TOTAL BILL<br />

Ave. Rate/kWh<br />

Inc./(Dec.) In Rate<br />

Inc./(Dec.) In Bill<br />

505.10 511.00<br />

5.1020 5.1616<br />

0.0596<br />

5.90<br />

DISPOSITION<br />

follows:<br />

WHEREFORE, the foregoing premises considered, it is hereby decided as<br />

1. To approve the unbundled schedule of rates of MANSONS, to be<br />

effective the first billing cycle thirty (30) days after receipt of this<br />

Decision, to wit;

Page 32 of 35<br />

MANSONS CORPORATION (MANSONS)<br />

<strong>ERC</strong> CASE NO. <strong>2002</strong>-<strong>18</strong> and <strong>2002</strong>-143<br />

RATE SCHEDULE<br />

Residential Commercial Streetlights Industrial Hospital Govt.Bldg.<br />

Generation Charge (PhP/kWh) 2.4897 2.4897 2.4897 2.4897 2.4897 2.4897<br />

Transmission Charge (PhP/kWh) 0.9667 0.8934 0.8301 0.4013 0.9036 0.9133<br />

(PhP/kW)<br />

138.07<br />

Distribution Charge (PhP/kWh) 1.0331 0.8950 0.6975 0.3589 0.9673 0.8284<br />

(PhP/kW)<br />

123.50<br />

Customer Charges<br />

Supply Charge (PhP/Meter/Mo.)<br />

12.57 12.57 12.57 12.57 12.57<br />

(PhP/kWh) 0.1538<br />

Metering Charge (PhP/Cust./Mo.) 5.00 17.28 0 604.95 17.28 17.28<br />

(PhP/kWh) 0.1292<br />

System Loss Charge (PhP/kWh) 0.5759 0.5759 0.5759 0.5759 0.5759 0.5759<br />

Inter-Class Cross<br />

Subsidy (PhP/kWh) (0.<strong>18</strong>69) 0.3776 0.1563 0.7551 0.5315 0.2955<br />

Lifeline Rate Subsidy (PhP/kWh) 0.0849 0.0849 0.0849 0.0849 0.0849 0.0849<br />

Universal Charge (PhP/kWh)<br />

Missionary Electrification<br />

0.0373 0.0373 0.0373<br />

Environmental Charge<br />

0.0025 0.0025 0.0025<br />

<strong>No</strong>te: Plus National and Local Franchise Taxes<br />

0.0373<br />

0.0025<br />

0.0373<br />

0.0025<br />

0.0373<br />

0.0025<br />

2. To approve MANSONS net utility plant in service at sound value as of<br />

September 1, 1998 amounting to PhP 28,355,700.<br />

3. To direct MANSONS to comply with the following:<br />

a) Discontinue charging the PPA upon effectivity of the approved<br />

unbundled rates. MANSONS shall automatically bill its enduser<br />

the new Generation Rate charged by NPC as approved<br />

and authorized by the <strong>Commission</strong>;<br />

b) Make a compliance filing with respect to its Other Charges a<br />

year from date of this Decision;<br />

c) Bill the amount of PhP 0.0373/kWh representing the missionary<br />

electrification portion of the Universal Charge in accordance<br />

with the Decision of the <strong>Commission</strong> in <strong>ERC</strong> <strong>Case</strong> <strong>No</strong>. 2001-<br />

165 (In the Matter of the Petition for the Availments from the

Page 33 of 35<br />

Universal Charge the Share for Missionary Electrification, NPC-<br />

SPUG, Applicant);<br />

d) Bill the amount of PhP 0.0025/kWh representing the<br />

environmental portion of the Universal Charge in accordance<br />

with the <strong>Commission</strong>’s Decision in <strong>ERC</strong> <strong>Case</strong> <strong>No</strong>. <strong>2002</strong>-194 (In<br />

the Matter of the Petition for the Availments from the Universal<br />

Charge the Environmental Share/Charge for the Rehabilitation<br />

and Management of Watershed Areas, NPC, Applicant);<br />

e) To set up a depreciation fund each year corresponding to the<br />

whole amount of depreciation that it has recorded on its books.<br />

The setting up of this fund should be done on a monthly basis<br />

corresponding to the monthly depreciation. MANSONS is<br />

required to strictly account for the expenditures out of this fund<br />

which should be used strictly for investment in electric plant and<br />

all withdrawals from this fund should be reported to the<br />

<strong>Commission</strong> within thirty (30) days from withdrawal;<br />

f) To inform the end-users within its franchise area of the<br />

approved unbundled rates not later than thirty (30) days after<br />

receipt of this Decision;<br />

g) Bill its respective end-users using a billing format which<br />

contains at least the rate elements provided in Annex “A” (Rate<br />

Schedule) of this Decision upon effectivity of the approved<br />

unbundled rates;

Page 34 of 35<br />

h) Bill its respective end-users using a billing format which<br />

contains at least the rate elements provided in Annex “B” of this<br />

Decision upon effectivity of the approved unbundled rates. The<br />

rate elements provided in Annex “B” should appear on the endusers’<br />

bills even if the rate elements currently have a rate of<br />

zero (0) or have not yet been determined by the <strong>Commission</strong>;<br />

and<br />

i) To submit for verification and confirmation purposes on or<br />

before the twentieth (20 th ) day of the month following the<br />

effectivity of the herein approved unbundled rates and every<br />

month thereafter: (a) five (5) sample bills for each customer<br />

class; (b) copy of bills from the generation and transmission<br />

companies; and (c) M-001 and M-002 with all related<br />

schedules;<br />

SO ORDERED.<br />

Pasig City, January 28, 2004.<br />

RODOLFO B. ALBANO<br />

Chairman<br />

OLIVER B. BUTALID<br />

<strong>Commission</strong>er<br />

CARLOS R. ALINDADA<br />

<strong>Commission</strong>er<br />

LETICIA V. IBAY<br />

<strong>Commission</strong>er<br />

JESUS N. ALCORDO<br />

<strong>Commission</strong>er

Page 35 of 35<br />

Copy furnished:<br />

1. Attys. <strong>No</strong>rberto F. Manjares and <strong>No</strong>rberto C. Manjares III<br />

Counsel for Applicant<br />

Law Office of Manjares & Manjares<br />

Suite 211, Jiao Building<br />

2 Timog Avenue, Quezon City 1100<br />

2. Office of the Solicitor General<br />

134 Amorsolo Street, Legaspi Village<br />

City of Makati 1229<br />

3. <strong>Commission</strong> on Audit<br />

Commonwealth Avenue<br />

Quezon City 0880<br />

4. Senate Committee on <strong>Energy</strong><br />

GSIS Building, Roxas Boulevard<br />

Pasay City 1307<br />

5. House Committee on <strong>Energy</strong><br />

Batasan Hills, Quezon City 1126<br />

6. The Municipal Mayor<br />

Floridablanca, Pampanga 2006<br />

7. Mansons Corporation<br />

Floridablanca, Pampanga 2006