An Introduction to the Ito Calculus and Stochastic Differential ...

An Introduction to the Ito Calculus and Stochastic Differential ...

An Introduction to the Ito Calculus and Stochastic Differential ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

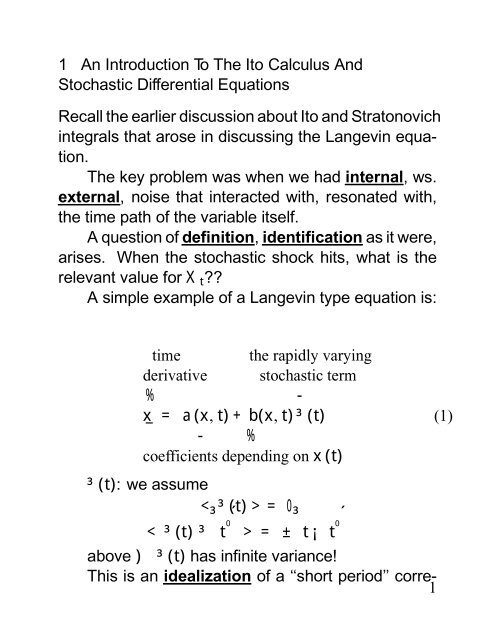

lated process.Example: =°2 e¡° jt¡t 0 j<strong>the</strong> correlation function for <strong>the</strong> Ornstein-Uhlenbeck process.This is correlated, not a white noise process. But, <strong>the</strong>limit of this as°!1 is a Divac delta function <strong>and</strong> is,in <strong>the</strong> limit, a white noise process.Thus:1R¡1°2 e¡° jt¡t 0 j definition of adt= 1 »Gausse Distributionlim°!1°2 e¡° jt¡t 0 j =0 8¯¯¯t¡t0¯¯¯6=0So a ‘white noise process ’can be regarded as <strong>the</strong>limit of an Ornstein-Uhlenbeck process, with very fastinteraction, ra<strong>the</strong>r with very short correlation times.It seems reasonable in order <strong>to</strong> make equation (1)useful as a model <strong>to</strong> require:U(t)=Z t0³³t 0´dt 0exists <strong>and</strong> is continuousU(t) is <strong>the</strong>n Markov:U(t), ¡ U ¡ t 0 ¢ ¡U(t)¢ , t0>tare independent.IfU(t) is continuous, it will have a Fokker-Planckrepresentation.2

We see in this case that:A(U 0 ,t)=0B(U 0 ,t)= 4t4t =1This is just <strong>the</strong> Wiener processZ t³³t 0´dt 0 = U(t) = W(t),in <strong>the</strong> old notation.0<strong>An</strong> alternative way of writing equation (1) is:x(t)¡x(0) =Z t0a[x(s),s]dstR h i+ b x(s)|{z} ,s ³(s)ds0%The key elementThis is an equation for <strong>the</strong> solution ofx(s) whichdepends on coefficients that in turn depend onX(s).Fur<strong>the</strong>r, we have <strong>to</strong> worry about what X(s) in b[²] isused <strong>to</strong> multiply <strong>the</strong> effect of³(s) onX(s)!Traditionally, using <strong>the</strong> Wiener process interpretation:4

Z tb[x(s),s]³(s)ds )Z tb[x(s),s]dW(s)0This last equation poses <strong>the</strong> problem:We have <strong>to</strong> define what we mean by:tR h ib x(s)|{z} ,s dW(s)|{z }0. &s<strong>to</strong>chastic process Wiener processdepending on aWiener process0(2)We will see that evenZ t0b(s)dW(s)needs interpretation forW(s), Wiener.The Gaussianity involved withdW(s) follows from<strong>the</strong> assumed continuity of U(t), coupled with <strong>the</strong>Fokker-Planck expansion.1.1 Definition Of A S<strong>to</strong>chastic IntegralLetG(t)be an arbitrary continuous function. W(t)is aWiener process- independent Gaussian increments of 5

a continuous s<strong>to</strong>chastic process, stationary with zeromean.Let us begin with a Rieman-Stieltjes integral interpretationof G(s)dW(s).tRt 0DiagramDefine¿ i 3t i¡1·¿ i·t i forft i g any partition of[t 0 ,t].We define <strong>the</strong> partial sum:S n =X ni=1G(¿ i )[W(t i )¡W(t i¡1 )]In <strong>the</strong> usual definition of <strong>the</strong> Rieman-Stieltjes integralnotinvolving a Wiener process- <strong>the</strong> partial sum limitdoes not depend on how <strong>the</strong> ¿ i are chosen inside[t i¡1 ,t i ].Here, it does.6

LetG(t)=W(t).We consider: =[min(¿ i ,t i )¡min(¿ i ,t i¡1 )]" "use of expectation + independent increments» CorrelationW(¿ i )W(t i )Therefore,=X ni=1(¿ i ¡t i¡1 ).Let¿ i = at i +(1¡a)t i¡1 , 0·a·1Therefore,< S n >=X ni=1(t i ¡t i¡1 )a= (t¡t 0 )a can be anything from0 <strong>to</strong>(t¡t 0 )!The I<strong>to</strong> solution is <strong>to</strong> choosea=0; i.e. ¿ i = t i¡1 ,so that <strong>the</strong> functionG(t)is treated as non-anticipatingfor[W(t i )¡W(t i¡1 )].7(3)

We define <strong>the</strong> I<strong>to</strong> S<strong>to</strong>chastic Integral:Z tGt 0³t 0´dW³t 0´´Recall:ms¡lim f P G(t i¡1 )[W(t i )¡W(t i¡1 )]gn! 1(4)ms¡lim X n =Xn! 1if <strong>and</strong> only iflim =0n! 1i.e. if <strong>and</strong> only ifZlimn! 1dwp(!)[X n (!)¡X(!)] 2 =01.1.1 A Key ExampleLetZ tt 0W(s)dW(s)W i =W(t i ), i=1,... n.8

S n =X nW i¡1 4W iW i¡1 (W i ¡W i¡1 ) = Xi=1 iWe solve this with a ‘trick ’re-exp.- Let ‘W i¡1 4W i ’ be <strong>the</strong> ‘cross-product ’termin a quadratic expansion.S n = 1 X n h(W i¡1 +4W i ) 2 :::2i=1i¡ (W i¡1 )| {z } 2 ¡(4W | {z i)}2. &Therefore, S n = 1 hW(t) 2 ¡W(t 0 ) 2i ¡ 1 2 2We now average:< X (4W i ) 2 >= X i=X ni=1(t i ¡t i¡1 ) =(t¡t 0 )This gives us <strong>the</strong> mean of P (4W i ) 2 ; we nowneed <strong>to</strong> see that its variance)0.Consider:X ni=1(4W i ) 29

=< X (W i ¡W i¡1 ) 4 +2 X i>j(W i ¡W i¡1 ) 2 (W j ¡W j¡1 ) 2¡2(t¡t 0 ) X (W i ¡W i¡1 ) 2 +(t¡t 0 ) 2 >W i ¡W i¡1 is Gaussian <strong>and</strong> is ind. of W j ¡W j¡1forjj(t i ¡t i¡1 )(t j ¡t j¡1 )¡2(t¡t 0 ) 2 + (t¡t 0 ) 2) 2 X (t i ¡t i¡1 ) 2 + X iX(t i ¡t i¡1 )(t j ¡t j¡1 )j:::) ¡(t¡t 0 ) 2 10

) X iXj[(t i ¡t i¡1 )¡(t¡t 0 )][(t j ¡t j¡1 )¡(t¡t 0 )]= 0by suming over one index first <strong>and</strong> recognizing thatX(ti ¡t i¡1 ) = (t¡t 0 ).The variance of P (4W i ) 2 is:2 X (t i ¡t i¡1 ) 2 · 2(t¡t 0 )" n ,since" n !0.Asn! 1, above)0 <strong>the</strong> limit.» <strong>the</strong> sum is on <strong>the</strong> µ order of122¢n¢ = 2 n n ! 0asn! 1.We conclude:a)ms¡lim P (4W i ) 2 =(t¡t 0 )n! 1b)Z tt 0W³t 0´dW³t 0´11

=<strong>the</strong> st<strong>and</strong>ard resultz }| {1hiW(t) 2 ¡W(t 0 ) 2 ¡(t¡t 0 )2| {z }enters because < P (4W i ) 2 > is ofsame order as rest of statement= < 1 2hi¡¡(t¡t 0 )>easy <strong>to</strong> see from= 0,S n = X W i 4W i<strong>and</strong>= 0as4W i ind. ofW i .A key problem is that dW(s), or ³(s) is of unboundedvariation.Let¡ be a partition of[t 0 ,t]Let12

S ¡ =nPi=1j4W i j#note jj.The variation of4W i over[t 0 ,t] is:V (4!, (t 0 ,t))= Sup¡ fS ¡ gIf V < 1, function is of bounded variation. Inour case with4W, it is not- recall ³(s) has ‘infinitevariance ’.Reconsider <strong>the</strong> integralZ tt 0G(s)dW(s),but now letG(s) be a function of<strong>to</strong>nly, that is not afunction ofW(s), or ofdW(s).Z tG(s)dW(s) = G(s)W(s) ¯¯tt 0t 0Z¡ W(s) G(s)ds _| {z }this is now an ordinaryRieman-Stieltjes integral!13

1.1.2 Some Important Properties Of <strong>the</strong> I<strong>to</strong> Integrala)Z tt 0(aG 1 +bG 2 )dW = ab)Z tZ tt 0G 1 dW +bZ t< GdW >= 0t 0c)Z t 2Z t= ds¯ ¯t 0 t 0or more generally:=Z tt 0G 2 dWt 0dsAll <strong>the</strong> results we have depend on <strong>the</strong> relationshipbetweenG(t)<strong>and</strong>W(t), or4W(t)being a non-anticipatingone.A functionG(t) is said <strong>to</strong> be non-anticipating, if8t

X(t)¡X(0) =Z tt 0a[X(s),s]dtZ t+ b[X(s),s]dW(s);t 0X(t) only involvesW(s) fors=forG(s), itselftRnon-anticipatingdW(s)G(s) >;t 015

1.2 <strong>An</strong> Important ResultForG(t) non-anticipating:Z t[dW(s)] 2+N G(s) ´ ms¡lim P G i¡1 (4W i ) 2+Nn! 1 it 0=Z tt 0G(s)ds forN =0´ 0 forN ¸11.3 Some Properties <strong>An</strong>d Important Formulae ForThe I<strong>to</strong> S<strong>to</strong>chastic IntegraltRa) Existence: G(s)dW(s) exists whenevert 0G(²) is continuous <strong>and</strong> non-anticipating on[t 0 ,t].b)d(W(t)) n = nW(s) n¡1 dW(s) (4)+ n(n¡1) W(s) n¡2 dt| 2 {z }note <strong>the</strong> added term16

This is a special case of a general result:Letf(W(s),s)be a continuous differentiable functiondf[W(t),t] = f t dt+ 1 2 f tt(dt) 2 +f w dW+ 1 2 f ww[dW] 2 + 1 2 f twdtdW +:::1.3.1 Derivation of <strong>the</strong>d(W(t)) n Resultd(W(t)) n = (W(t)+dW(t)) n| {z } ¡(W(t))n=X nk=0+µ nW(t)kn¡k dW(t) k ¡W(t) n= W(t) n ¡W(t) n +nW(t) n¡1 dW(t)n(n¡1)+ W(t) n¡2 dW(t) 2| 2 {z }#n(n¡1)2W(t) n¡2 dtHigher powers of dW(t) all have zero expectation.Therefore,17

d(W(t)) n = nW(t) n¡1 dW(t)| {z }usual result18

+ n(n¡1) W(t) n¡2 dt| 2 {z }due <strong>to</strong> non-vanishing of2nd order effects8 Fordtsmall:< (dt) 2 !0* [dW(t)] 2 !dt, by previous arguments:=0, dtnon-anticip. =0.* within integrals: note integral definition in a mean sq.lim. sense.<strong>and</strong> we have concluded that higher powers vanish.This produces:df[W(t),t] $Ã!f t + 1 2 f ww dt (5)|{z}note <strong>the</strong> extra term+f w dW(t)Example:hd e W(t)i = e W(t)+4W ¡e W(t)= e W(t)£ e 4W ¡1 ¤ 19

= e W(t)·1+4W + 4W22Example:$ e W(t)·dW + 1 2 dţZ t¸+ ... ¡1W(s) n dW(s)t 0integrate by parts <strong>and</strong> use equation (4).2 3Z tt ZW(s) n dW(s) = W(s)n+1t¡ 6n+1 ¯ 4 W(s)dW(s) n75t 0t 0 t| 0{z }.Z t ·W(s) nW(s) n¡1 dW(s)+ n(n¡1) ¸W(s) n¡2 dt2t 0Therefore,Z t(n+1)t 0W(s) n dW(s) = W(s) n+1 j t t 0¡ n(n¡1)2Z tt 0W(s)W(s) n¡2 d20

)Z tt 0W(s) n dW(s) =1n+1¡ n(n¡1)2(n+1)hw(t) n+1 ¡W(t 0 ) n+1iZ tt 0W(s) n¡1 dt21

$1hW(t) n+1 ¡W(t 0 ) n+1i| n+1 {z }‘regular ’solutionZ t¡ n W(s) n¡1 dt (6)2t| 0{z }‘correction ’term added due <strong>to</strong> internal noiseZ t< G(s)dW(s)>=0 (7)t 0in terms of <strong>the</strong> partial sums< X G i¡1 4W i > = X i= 0IfG(²),H(²) are arbitrary non-anticip. functions: (8)= dtt 0Use <strong>the</strong> partial sums <strong>to</strong> show <strong>the</strong> result as in <strong>the</strong>previous case.22

1.3.2 Important Convention Using±(²)Z t 2t 1f(t)±(t¡t 1 )dt = f(t 1 )Z t 2t 1f(t)±(t¡t 2 )dt = 0<strong>to</strong> maintain ‘non-anticipation ’.(9)1.4 Initial <strong>Introduction</strong> To S<strong>to</strong>chastic <strong>Differential</strong>Equations Using I<strong>to</strong> <strong>Calculus</strong>We can begin with a simple equation:_x = a(x,t)+b(x,t)³(t)corresponds <strong>to</strong> a s<strong>to</strong>chastic equation integralx(t)¡x(0) =Z ta(x(s),s)ds+0Z tb(x(s),s)dW(s)(10)023

These equations are I<strong>to</strong> S<strong>to</strong>chastic <strong>Differential</strong> Equationsif <strong>the</strong>y obey <strong>the</strong> I<strong>to</strong> calculus.Consider a discretization of <strong>the</strong> differential equation,lettingX ti =X iX i+1 = X i +a(X i ,t i )4t i (11)+b(X i ,t i )4W i4t i =t i ¡t i¡1 4W i =W(t i )¡W(t i¡1 )DiagramThis approximate solution method is called is called<strong>the</strong> Cauchy-Euler method- is very useful for simulationsin simple cases.Existence Condition For A Solution:Lipschitz: 9K 1 3ja(x,t)¡a(y,t)j+jb(x,t)¡b(y,t)j·K 1 jx¡yj24

Growth Condition (For Uniqueness <strong>An</strong>d BoundedPaths):9K 2 3ja(x,t)j 2 +jb(x,t)j 2·K 2³1+jxj 2´2are true8fx,yg.The solution pathx(t) is Markov.1.5 Change Of Variable- I<strong>to</strong>’s FormulaIfdX(t) = a(x,t)dt+b(x,t)dW(t)<strong>and</strong>f(²) is a continuous differential function- what is<strong>the</strong> differential equation fordf(X(t))?df[X(t)] = f[X(t)+dX(t)]| {z } ¡f[X(t)]exp<strong>and</strong> aboutX(t)= f 0 [X(t)]dX(t)+ 1 2 f0 [X(t)]dX(t) 2 + ...$ f 0 [X(t)][adt+bdW t ]+ 1 [X(t)][adt+bdW2 f0 t ]| {z }2#£ a 2 dt 2 +2abdtdW t +b 2 dWt¤225

(= f 0 [X(t)]a(x,t)+ 1 [X(t)]b 2 (x,t)| 2 f0 {z }* I<strong>to</strong> addition+f 0 [X(t)]b(x,t)dW twhere we recognize that:h(dW(t)) 2i !0(dt) 2 !0dtdW(t) !0)dtdW tdtdW t dtdt 00 0We can generalize fur<strong>the</strong>r,LetY t =u(t,X t )dX t =a(X t ,t)dt+b(X t ,t)dW(t)dY t ="u t (t,X t )+u X (²)a(²)+ 1 2 u XX(²)b(²) 2| {z }<strong>the</strong> I<strong>to</strong> extra term¤dt+u X b(²)dW(t)#26

1.6 Link Between <strong>the</strong> S<strong>to</strong>chastic <strong>Differential</strong>Equation <strong>An</strong>d <strong>the</strong> Fokker-Planck EquationConsider first <strong>the</strong> time development of an arbitraryf(x(t)), differentiable.< d f(x(t)) >= ddt dt by exchanging order ofd(²)+ R (²)= ,term involvingdW(t))0 on taking expectation.X(t)has a conditional prob. densityp(x,tjx 0 ,t 0 )with respect <strong>to</strong> which <strong>the</strong> expectation is <strong>to</strong> be taken.We reconsider ddt paying attention <strong>to</strong><strong>the</strong> density function.Zddt = dxf(x)@ t p(x,tjx 0 ,t 0 )Z= dx·f x a(x,t)+ 1 2 b(x,t)2 f xx¸p(x,tjx 0 ,t 0 )| {z }process of taking <strong>the</strong> expectationusing <strong>the</strong> previous statement.But when we solved <strong>the</strong> differential form of <strong>the</strong>Chapman-Kolmogorov equation we solved <strong>the</strong> equation,<strong>the</strong> simple univariate form of which is *- i.e. wehave:27¤

Z Zdxf(x)p t (²) = dxf(x)f¡@ x [a(x,t)p]+ 1 h i ¾2 @2 x b(x,t) 2 pwhich is obtained from * by integrating by parts <strong>and</strong>discarding ‘surface terms ’, that is:f(x)pj 1 ¡1Butf(x) is an arbitrary function; i.e. <strong>the</strong> above istrue8f(x) diff.<strong>the</strong>refore@ t p(x,tjx 0 ,t 0 )= ¡@ x [a(x,t)p(x,tjx 0 ,t 0 )]+ 1 h i2 @2 x b(x,t) 2 p(x,tjx 0 ,t 0 )If <strong>the</strong> time derivative of <strong>the</strong> mean of f(x) can beexpressed as <strong>the</strong> mean of a s<strong>to</strong>chastic differential equationwith parameters a(x,t), b(x,t); <strong>the</strong>n <strong>the</strong> transitionprobability density obeys a Fokker-Plank equationwith <strong>the</strong> same parameters.1.7 Some Simple ExamplesA) Coefficients not involvingx(t).<strong>the</strong>reforedx=a(t)dt+b(t)dW(t)28

Rx(t) = |{z}x 0 + ta wtd. sum of Gaussian-Ra(s)ds+ tt 0t 0b(s)dW(s)&may, may not be r<strong>and</strong>om, but is usuallyassumed <strong>to</strong> be ind. ofdW(s),)x(t) is non-anticipating.Z t=+ a(s)dst 0The covariance function is given by:- ignoring, we have[b(u)] 2 duTo get this result we have used:Z tt 0Z tG(s)dW(s) H(s)dW(s)t 0 t 029

where here:Z t= dst 0G(v)=b(v), v

<strong>and</strong>dW(s) 2 )dtThis equation is directly integrable as well.y(t) = y 0 +c[W(t)¡W(t 0 )]¡ 1 2 c2 (t¡t 0 )<strong>and</strong> as½ x=e yx(t)=x 0 Exp c[W(t)¡W(t 0 )]¡ 1 ¾2 c2 (t¡t 0 )Since==0forx(t) non-anticipating<strong>the</strong>refore,= *<strong>and</strong>ddt =0,follows from *.=¤=exp £ c 2 min(t¡t 0 ,s¡t 0 ) ¤is obtained by recalling that for z Gaussian with zeromean31

½ ¾ = e2- cf. mean <strong>and</strong> variance of a log normal distribution.1.7.1 The Ornstein-Uhlenbeck ProcessWe recall <strong>the</strong> Fokker-Planck equation was:p t =@ x (kxp)+ 1 2 Dp xxFur<strong>the</strong>r, we showed above <strong>the</strong> link between Fokker-Planck <strong>and</strong> I<strong>to</strong> S<strong>to</strong>chastic <strong>Differential</strong> Equations.Ifp t =¡@ x [a(x,t)p]+ 1 h i2 @2 x b(x,t) 2 p<strong>the</strong>n< df(x)dt > , usingdx=a(x,t)dt+b(x,t)dW(t)Here,<strong>the</strong>refore= .a(x,t)=¡kxb(x,t)= p Ddx=¡kxdt+ p DdW(t)We solve this by a transformation of variables as 32

well.Let<strong>the</strong>reforey=xe ktdy = dxe kt +xd ¡ e kt¢ +(dx)de kt| {z }remember, need2nd. order terms.<strong>the</strong>refore,dy =(dx)d ¡ ez }| kt¢{ke kth ¡kxdt+ p iDdW(t) dt+dxez }| kth{¡kxdt+ p iDdW(t) e kt +vanishes becausedt 2 !0,dtdW t !0- cancell<strong>the</strong>refore,dy= p De kt dW(t)<strong>the</strong>refore<strong>the</strong>reforey(t) = y(0) p DZ tt 0e kt dW(t)xd ¡ e kt¢z }| {kxe kt dt33

x(t) = x(0)e ¡kt|{z} +p D t Rfort 0 =0.& .de-transformation0e ¡k(t¡s) dW(s)Maintaining <strong>the</strong> usual assumptions:=e ¡kt<strong>the</strong>reforevarfx(t)g =< © [x(0)¡]e ¡kt9+ p Z t 2=D e ¡k(t¡s) dW(s) >;0varfx(t)g = varfx(0)ge ¡2kt+DZ te ¡2k(t¡s) dsby once again usingZ t0Z t< G(s)dW(s) H(u)dW(u)>t 0 t 0Z t= dtt 034

<strong>the</strong>reforevarfx(t)g =·varfx(0)g¡ D ¸e ¡2k t+ D 2k 2kOne last example:C) A time-dependent Ornstein-Uhlenbeck process.Let:dx(t) = ¡ A |{z} (t)x(t)dt+ B(t)dW(t).replaces <strong>the</strong> ‘k ’ used beforeWe can solve this equation by solving first <strong>the</strong> homogeneousequation <strong>and</strong> <strong>the</strong>n adding a particular solution.dx(t)=¡A(t)x(t)dt<strong>the</strong>refore 2 3x(t)=x(0)exp4¡Z tThe inhomogeneous solution is:2x(t) = x(0)exp4¡0Z tA(s)ds53A(s)ds5+Z texp24¡Z t03A(u)du5B(s)dW(s)0sWe discuss <strong>the</strong> general (single variable) linear sys-35

tem. We distinguish between <strong>the</strong> homogeneous casedxx =A(t)<strong>and</strong> <strong>the</strong> inhomogeneous case where this is not true.Homogeneous Equation:dx=[b(t)dt+g(t)dW(t)]x(t)A natural transformation of variables <strong>to</strong> solve is:y=logx<strong>the</strong>reforedx 2x 2dy = dx x ¡1 2.added since we suspect2nd.order conditions are important.Substituting <strong>the</strong> definition ofdx, we get:usingdy = [b(t)dt+g(t)dW(t)]¡ 1 2 g(t)2 dt=·b(t)¡ 1 g(t)2¸dt+ g(t)dW(t),2<strong>the</strong>reforedt 2 !0E © dW 2ª !dtEfdWdtg! 0,36

<strong>the</strong>reforey(t) = y(t 0 )++Z tZ t ·b(s)¡ 1 2 g(s)2¸dst 0t 0g(s)dW(s)2Z t " # 3x(t) = x(0)Exp4b(s)¡ g(s) 2 Z tds+ g(s)dW(s) 520t| {z 0}defines'(t)is <strong>the</strong> homogeneous solution.Letx(t)=x(0)'(t)<strong>and</strong> so define'(t)- see above.Inhomogeneous case,dx=[a(t)+b(t)x]dt+[f(t)+g(t)x]dW(t)Solution involves a ‘trick ’:LetZ(t)=x(t)' ¡1 (t)<strong>the</strong>reforedZ =dx' ¡1 +xd' ¡1 +dxd' ¡1By using rules fromdW n , we get:37

d' ¡1 = ¡ d' + (d')2' 2 ' 3Using I<strong>to</strong> rules <strong>and</strong> substituting, we get:dz = f[a(t)¡f(t)g(t)]dt+f(t)dW(t)g'(t) ¡1<strong>and</strong> this is directly integrable.The solution by resubstituting is:x(t) = '(t)fx(0)| {z }homogeneous solution+Z t9>='(s) ¡1 f[a(s)¡f(s)g(s)]ds+f(s)dW(s)g>;0| {z }inhomogeneous component1.8 Rule For Integration By Parts For I<strong>to</strong> <strong>Calculus</strong>Letdx 1 (t) = f 1 (t)dt+G 1 (t)dW(t)dx 2 (t) = f 2 (t)dt+G 2 (t)dW(t)Considerd(X 1 (t)X 2 (t)) <strong>and</strong> use above ‘rules ’:d(X 1 (t)X 2 (t)) = X 1 (t)dX 2 (t)+X 2 (t)dX 1 (t) 38

+G 1 (t)G 2 (t)dt (A)= ¡ X 1 f 2 +X 2 f 1 +G 1 G 2¢dt+(X1 G 2 +X 2 G 1 )dW(t)Note <strong>the</strong> extra terms.<strong>and</strong>Recall:if<strong>the</strong>reforedY =dX t =f t dt+GdWY t =u(x,t)µu t (t,x t )+u x (²)f t + 1 2 u xx(²)G 2 dt+u x GGdW tSo we get: (integrating(A))X 1 (t)X 2 (t) = X 1 (t 0 )X 2 (t 0 )+Z t 1t 0X 1 dX 2+Z t 1t 0X 2 dX 1 +Z t 1t 0G 1 G 2 ds| {z }extra term.1.9 Some Special Casesu(t,W t ) : X t´W t39

du(t,W t )=µu t (²)+ 1 2 u xx(²) dt+u x (²)dW(t)<strong>and</strong> whenu(²) is ind. oft:du(W t ) = u 0 (W)dW + 1 2 u0 (W)d<strong>to</strong>ru(W t ) = u(0)+Z t0u 0 (W)dW + 1 2Z t0u 0 (W)dsLastly, consider <strong>the</strong> General Linear (Scalar) Equation.mXdX(t) = (A(t)X t +a(t))dt+ (¯i(t)X t ¡b i (t))dWtii=1- note aspects of linearity- is also linear indW i t.©Witªis anm -dimensional Wiener process.X t0 =X(t 0 )Solution <strong>to</strong> <strong>the</strong> above equation is:2Z t à !mXX t = ' t4X t0 + a(s)¡ ¯i(s)b i (s)' ¡1st 01ds40

where+' t = ExpmX1Z t' ¡1s b i (s)dWsit 02Z t ÃmX4 A(s)¡t10B i (s) 22!dsZ tmX+ B i (s)dWsi1t 0is itself <strong>the</strong> solution <strong>to</strong> <strong>the</strong> homogeneous equation:mX_' t = A(t)' t dt+ B i (t)' t dWti1' t0´1.The form of this equation is <strong>the</strong> usual:f ¡ X,X _¢ =g t , g t a forcing term<strong>and</strong> if:' t =Xtis a solution <strong>to</strong> <strong>the</strong> homogeneous equation,ZtX t = ' t X t0 +' t ' ¡1s g s dst 0is <strong>the</strong> <strong>to</strong>tal solution.41

(Saved under v: IntroI<strong>to</strong>)42