INCOME TAXESPetrowest, and its operating entities, are taxable entities under the Income Tax Act <strong>of</strong> Canada and arecurrently taxable only on income that is not distributed or distributable to the unit holders. As the <strong>trust</strong>currently distributes all <strong>of</strong> its taxable income to the unit holders, no provision for income taxes has beenmade in these consolidated financial statements.On October 31, 2006, the Minister <strong>of</strong> Finance (Canada) announced income tax proposals which, ifenacted, would modify the taxation <strong>of</strong> certain flowthrough entities including mutual fund <strong>trust</strong>s and theirunitholders (the "October 31 Proposals"). The October 31 Proposals will apply to a specified investmentflowthrough ("SIFT") <strong>trust</strong> and will apply a tax at the <strong>trust</strong> level on distributions <strong>of</strong> certain income fromsuch SIFT <strong>trust</strong> at a rate <strong>of</strong> tax comparable to the combined federal and provincial corporate tax rate.These distributions will be treated as dividends to the Trust unitholders.On March 19, 2007, the Government <strong>of</strong> Canada tabled in Parliament Bill C-52 draft legislation toimplement the October 31 Proposals discussed above. Bill C-52, which has received first reading,appears to be generally consistent with details included in the October 31 announcement.It is expected that Petrowest will be characterized as a SIFT <strong>trust</strong> and as a result would be subject to theOctober 31 Proposals. The October 31 Proposals are to apply commencing January 1, 2007 for all SIFT<strong>trust</strong>s that begin to be publicly traded after October 31, 2006 and commencing January 1, 2011 for allSIFT <strong>trust</strong>s that were publicly traded on or before October 31, 2006. Subject to the qualification belowregarding the possible loss <strong>of</strong> the four year grandfathering period in the case <strong>of</strong> undue expansion, it isexpected that Petrowest will not be subject to the October 31 Proposals until January 1, 2011.Under the existing provisions <strong>of</strong> the Income Tax Act, Petrowest can generally deduct, in computing itsincome for a taxation year, any amount <strong>of</strong> income that it distributes to unitholders in the year and, on thatbasis, Petrowest is generally not liable for any material amount <strong>of</strong> tax.Pursuant to the October 31 Proposals, commencing January 1, 2011, (subject to the qualification belowregarding the possible loss <strong>of</strong> the four year grandfathering period in the case <strong>of</strong> undue expansion),Petrowest will not be able to deduct certain <strong>of</strong> its distributed income (referred to as specified income).Petrowest will become subject to a distribution tax on this specified income at a special rate estimated tobe 31.5%.Petrowest may lose the benefit <strong>of</strong> the four year grandfathering period if Petrowest exceeds the limits onthe issuance <strong>of</strong> new <strong>trust</strong> units and convertible debt that constitute normal growth during thegrandfathering period (subject to certain exceptions). The normal growth limits are calculated as apercentage <strong>of</strong> Petrowest's market capitalization <strong>of</strong> $248.9 <strong>million</strong> on October 31, 2006 as follows: 40percent for the period November 1, 2006 to December 31, 2007, 20 percent for each <strong>of</strong> 2008, 2009 and2010. Unused portions may be carried forward until December 31, 2010.Pursuant to the October 31, 2007 proposals, the distribution tax will only apply in respect <strong>of</strong> distributions<strong>of</strong> income and will not apply to returns <strong>of</strong> capital.If the October 31 Proposals are implemented, it is expected that the imposition <strong>of</strong> tax at the PetrowestTrust level under the October 31 Proposals will materially reduce the amount <strong>of</strong> cash available fordistributions to unitholders and Petrowest may be required to make income tax provisions in the future.NET INCOMENet loss for the period ended March 31, 2007 was $(2,224,339). This represents a net loss per unit <strong>of</strong>$0.08, basic and fully diluted.- 14 -

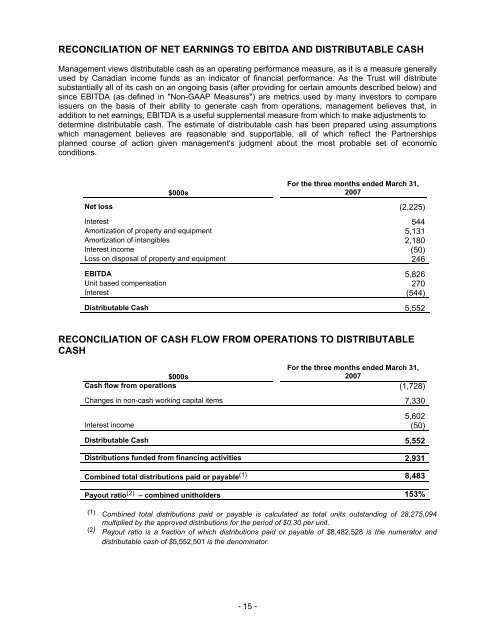

RECONCILIATION OF NET EARNINGS TO EBITDA AND DISTRIBUTABLE CASHManagement views distributable cash as an operating performance measure, as it is a measure generallyused by Canadian income funds as an indicator <strong>of</strong> financial performance. As the Trust will distributesubstantially all <strong>of</strong> its cash on an ongoing basis (after providing for certain amounts described below) andsince EBITDA (as defined in "Non-GAAP Measures") are metrics used by many investors to compareissuers on the basis <strong>of</strong> their ability to generate cash from operations, management believes that, inaddition to net earnings, EBITDA is a useful supplemental measure from which to make adjustments todetermine distributable cash. The estimate <strong>of</strong> distributable cash has been prepared using assumptionswhich management believes are reasonable and supportable, all <strong>of</strong> which reflect the Partnershipsplanned course <strong>of</strong> action given management's judgment about the most probable set <strong>of</strong> economicconditions.$000sFor the three months ended March 31,2007Net loss (2,225)Interest 544Amortization <strong>of</strong> property and equipment 5,131Amortization <strong>of</strong> intangibles 2,180Interest income (50)Loss on disposal <strong>of</strong> property and equipment 246EBITDA 5,826Unit based compensation 270Interest (544)Distributable Cash 5,552RECONCILIATION OF CASH FLOW FROM OPERATIONS TO DISTRIBUTABLECASHFor the three months ended March 31,$000s2007Cash flow from operations (1,728)Changes in non-cash working capital items 7,3305,602Interest income (50)Distributable Cash 5,552Distributions funded from financing activities 2,931Combined total distributions paid or payable (1) 8,483Payout ratio (2) – combined unitholders 153%(1) Combined total distributions paid or payable is calculated as total units outstanding <strong>of</strong> 28,275,094multiplied by the approved distributions for the period <strong>of</strong> $0.30 per unit.(2) Payout ratio is a fraction <strong>of</strong> which distributions paid or payable <strong>of</strong> $8,482,528 is the numerator anddistributable cash <strong>of</strong> $5,552,501 is the denominator.- 15 -